Understanding How a Home Equity Line of Credit Works If you are a homeowner in…

The Impact of Inflation on Mortgage Affordability in Long Island: A 2026 Forecast

For potential homebuyers in Hauppauge and across Long Island, the economic headlines of the past few years have been dominated by one scary word: Inflation. It affects the price of gas, groceries, and, most significantly, the cost of housing. As we look toward 2026, understanding the intricate dance between inflation, Federal Reserve policies, and mortgage rates is crucial for anyone looking to buy a home or refinance in Nassau or Suffolk County.

At RCG Mortgage, we believe that an educated borrower is a successful borrower. Whether you are a first-time homebuyer trying to break into the market or a seasoned investor, navigating the currents of the Long Island real estate market requires local expertise and a forward-looking strategy. Here is our comprehensive forecast on how inflation will impact mortgage affordability in 2026 and what you can do to prepare.

The Inflation-Interest Rate Connection

To understand where mortgage rates are going in 2026, we first have to understand the relationship between inflation and interest rates. Simply put, inflation is the enemy of long-term bonds, including mortgage-backed securities. When inflation rises, the purchasing power of the interest payments investors receive diminishes. To compensate for this risk, lenders demand higher interest rates.

Furthermore, the Federal Reserve combats high inflation by raising the Federal Funds Rate. While the Fed doesn’t set mortgage rates directly, their moves influence the bond market, which in turn drives mortgage rates up or down. As we move through 2025 and into 2026, the key indicator to watch is the Consumer Price Index (CPI). If inflation data shows a consistent cooling trend, we can expect mortgage rates to stabilize or potentially decrease, improving affordability for Long Island buyers.

Long Island Real Estate Market: A 2026 Forecast

Long Island is a unique market. Unlike other parts of the country where land is abundant, Nassau and Suffolk Counties have limited inventory and high demand. This creates a “floor” for home prices, even when rates are high. Here is what we forecast for the local market in Hauppauge and beyond for 2026:

- Inventory Constraints Will Persist: The “lock-in effect”—where homeowners with 3% mortgage rates refuse to sell—will likely begin to ease by 2026, but inventory will remain tight compared to historical averages.

- Price Appreciation: While we may not see the explosive double-digit growth of the pandemic years, home prices in desirable school districts like Hauppauge are expected to see moderate, steady appreciation. Inflation drives up the cost of construction materials and labor, making new builds more expensive and driving up the value of existing homes.

- The Return of Competition: If rates dip in 2026 as inflation stabilizes, a wave of sidelined buyers will re-enter the market. This could reignite bidding wars, meaning affordability isn’t just about the rate—it’s about the purchase price.

How Inflation Affects Your Borrowing Power in Hauppauge

Inflation doesn’t just impact the rate; it impacts your monthly budget and your debt-to-income (DTI) ratio. As the cost of living rises, lenders scrutinize your disposable income more heavily. However, the most direct impact is on “Purchasing Power.”

Consider this scenario: A 1% increase in mortgage rates can reduce your purchasing power by approximately 10-11%. This means that if inflation remains stubborn and rates stay elevated, the home you could afford in 2024 might be out of reach in 2026 unless your income has increased proportionately.

The “Cost of Waiting” Analysis

Many clients ask Andrew Russell and the team at RCG Mortgage, “Should I wait for rates to drop?” It is a valid question, but in an inflationary environment, waiting can be costly. If home prices in Long Island appreciate by 4% annually, a $600,000 home today will cost roughly $649,000 in two years. Even if rates drop by 1%, the higher loan amount might negate the savings, and you would have missed out on two years of equity building.

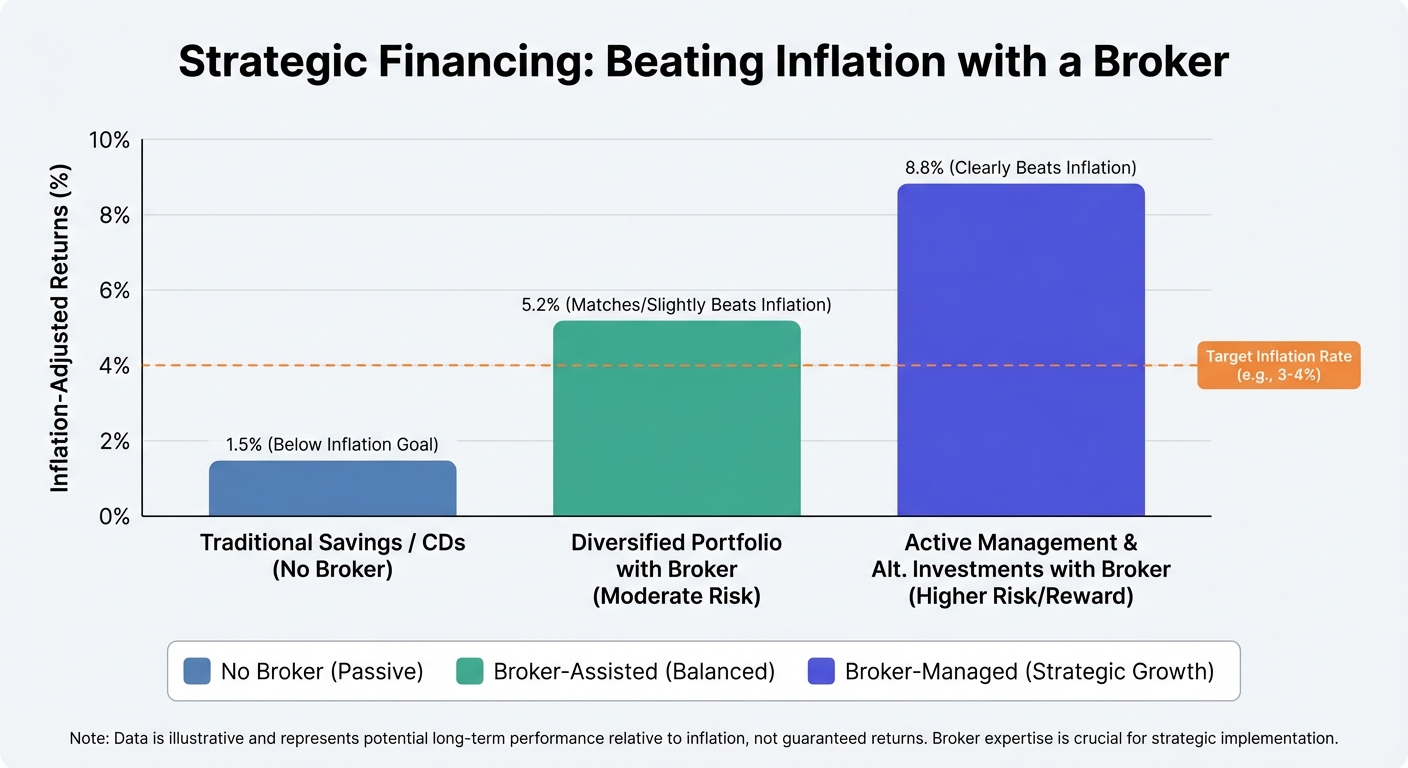

Strategic Financing: Beating Inflation with a Broker

This is where the “Big-Bank Fatigue” sets in. Big banks often have rigid underwriting guidelines and a limited menu of products. In a volatile, inflationary market, you need flexibility. As a premier Mortgage Broker in Hauppauge, NY, RCG Mortgage offers strategies that big banks simply cannot match.

1. Adjustable-Rate Mortgages (ARMs)

If the forecast predicts rates will drop in 2026 or 2027, locking in a 30-year fixed rate at a peak might not be the best move. An ARM often offers a lower initial interest rate for 5, 7, or 10 years. This can make monthly payments more affordable now, with the plan to refinance when inflation cools and rates drop.

2. Temporary Buydowns (2-1 Buydown)

3. Non-QM and Bank Statement Loans

Inflation hits self-employed business owners differently. If your tax returns show high write-offs to combat inflation costs, a traditional bank might deny you. RCG Mortgage has access to Non-QM loans that use bank statements to qualify income, ensuring you don’t miss out on homeownership due to tax strategy.

Renting vs. Buying in an Inflationary Economy

Below is a projection of the cost difference over 5 years based on current Long Island trends:

| Factor | Buying (Fixed Rate Mortgage) | Renting |

|---|---|---|

| Monthly Payment Stability | Principal & Interest are locked. Payment is stable. | Rent increases annually (typically 3-5% or matching inflation). |

| Asset Value | Home value appreciates with inflation. | No asset accumulation. You pay the landlord’s mortgage. |

| Tax Benefits | Potential deductions for mortgage interest and property taxes. | No tax benefits. |

| Inflation Impact | Positive: You pay back debt with “cheaper” future dollars. | Negative: Your housing cost rises as the dollar weakens. |

Why Choose RCG Mortgage? The Nordstrom Experience

In a challenging market, who you work with matters. At RCG Mortgage, our philosophy is simple: we provide a “Nordstrom” experience coupled with a “Ford” assembly line efficiency. We don’t just process loans; we engineer mortgage solutions tailored to your life goals.

Founder Andrew Russell has built a team that understands the nuances of the Hauppauge and greater Long Island market. Being a broker means we shop dozens of lenders to find the specific program that fits your needs—whether that is FHA, VA, Conventional, or Jumbo financing. We operate with transparency and accountability, ensuring you aren’t just a number in a queue.

“Brokers Do it Better… RCG Does it Best.” This isn’t just a slogan; it’s a promise backed by our recognition as a top Mortgage Brokerage locally and nationally.

Frequently Asked Questions (FAQs)

1. Will mortgage rates go down in 2026?

While no one has a crystal ball, most economic forecasts suggest that as the Federal Reserve achieves its target inflation rate, mortgage rates should stabilize and potentially trend downward in 2026. However, they are unlikely to return to the historic lows of 2020-2021.

2. Is it better to buy now or wait until 2026?

Waiting carries the risk of higher home prices. If you can afford the monthly payment now, buying allows you to start building equity immediately. You can always refinance the rate later if they drop (“Date the rate, marry the house”), but you cannot renegotiate the purchase price once the market goes up.

3. How does a mortgage broker differ from a bank regarding inflation?

Banks usually have one set of rates and products. If their rates are high due to inflation, you are stuck. A mortgage broker like RCG Mortgage has access to wholesale rates from multiple lenders, allowing us to shop for the most competitive pricing and find niche products (like ARMs) that help mitigate high-interest environments.

4. What is the loan limit for Long Island in 2026?

Conforming loan limits typically increase annually to account for home price appreciation (inflation). While 2026 limits haven’t been released yet, the trend suggests they will be higher than 2025 limits, allowing borrowers in high-cost areas like Suffolk County to avoid Jumbo loan rates for higher purchase prices.

5. Can I buy a home in Hauppauge with a low down payment?

Absolutely. Despite inflation, programs like FHA loans (3.5% down) and conventional loans for first-time buyers (3% down) are still available. RCG Mortgage specializes in helping first-time buyers navigate these options to minimize upfront costs.

Secure Your Financial Future Today

Inflation is a reality, but it doesn’t have to be a roadblock to your dream home. By understanding the market forecast and utilizing the right mortgage products, you can turn a challenging economic environment into an opportunity for wealth building.

Don’t let the headlines paralyze you. Partner with a team that has the local expertise and the “Nordstrom” level of service you deserve. Contact Andrew Russell and the RCG Mortgage team today to discuss your 2026 homeownership strategy.

Ready to get started?

Request a No-Obligation Quote or call us directly at (516) 246-6353.

Related Posts