Understanding How a Home Equity Line of Credit Works If you are a homeowner in…

The Complete Guide to Mortgage Closing Day: What to Expect from Your Broker and Attorney

You have made it. After months of house hunting in Hauppauge, NY, submitting financial documents, and waiting on underwriting, you have finally reached the finish line: Closing Day. For many first-time homebuyers and even seasoned investors, this day is a mix of excitement and anxiety. It is the moment keys change hands, and you officially become a homeowner.

At RCG Mortgage, we believe the closing process shouldn’t be a mystery. As Andrew Russell, our founder, often says, we aim to provide a “Nordstrom” customer service experience coupled with a “Ford” assembly line efficiency. This means high-touch service with a streamlined, predictable process.

However, in New York, closing day involves a specific cast of characters—specifically your mortgage broker and your real estate attorney. Understanding who handles what is the key to a stress-free experience. This guide will walk you through exactly what to expect when closing on a home in Long Island and how we ensure your transaction crosses the finish line smoothly.

The “Clear to Close”: The Green Light

Before we talk about the closing table, we need to talk about the most important three words in the mortgage industry: Clear to Close (CTC). This is the milestone we work toward from day one.

A “Clear to Close” means the underwriter has reviewed and approved all your documentation, the appraisal is solid, and the lender is ready to fund your loan. Once RCG Mortgage secures this for you, the clock starts ticking toward your closing appointment.

The Closing Disclosure (CD)

By law, you must receive your Closing Disclosure (CD) at least three business days before you sign your loan documents. This document is the final version of the Loan Estimate you received at the beginning of the process. It outlines:

- Your final interest rate.

- Your monthly payments.

- Your total closing costs.

- The exact amount of “Cash to Close” you need to bring to the table.

Pro Tip: Compare your CD against your Loan Estimate. If there are significant discrepancies, contact your RCG Mortgage broker immediately. Transparency is one of our core values, and we ensure you understand every penny involved.

New York: An Attorney Closing State

If you are buying a home in Hauppauge or anywhere else in New York, it is important to understand that New York is an “attorney state.” In many other parts of the country, title companies handle the closing. Here, real estate attorneys drive the legal side of the transaction.

This creates a partnership between your mortgage broker (who secures the money) and your attorney (who secures the property title). Here is how the responsibilities are divided:

The Role of Your Real Estate Attorney

Your attorney represents your legal interests. On closing day, they are the ones sitting next to you at the table. Their responsibilities include:

- Reviewing the contract of sale.

- Examining the title report to ensure there are no liens against the property.

- Calculating tax adjustments (property taxes paid upfront by the seller).

- Explaining the legal documents you are signing (the Deed, the Note, the Mortgage).

- Disbursing the funds to the seller.

The Role of Your Mortgage Broker (RCG Mortgage)

While the attorney handles the paperwork, RCG Mortgage handles the financing. Our job is to make sure the money is there when you need it. Our role leading up to and on closing day includes:

- Finalizing the loan package with the lender.

- Coordinating with the attorney to balance the final numbers.

- Ensuring the lender wires the funds to the closing table.

- Resolving any last-minute conditions required by the bank.

We operate with transparency and accountability. Even though we might not physically sit at the table (as that is the attorney’s domain in NY), we are virtually there, monitoring the funding status to ensure no delays occur.

Visualizing the Responsibilities: Broker vs. Attorney

To help you understand who to turn to for what, we have broken down the responsibilities in the table below.

| Task/Responsibility | Mortgage Broker (RCG) | Real Estate Attorney |

|---|---|---|

| Securing the Interest Rate | ✔ | |

| Title Search & Insurance | ✔ | |

| Underwriting Approval | ✔ | |

| Reviewing Legal Contracts | ✔ | |

| Coordinating Bank Wire/Funding | ✔ | (Receives Funds) |

| Explaining Loan Terms | ✔ | |

| Explaining Deed & Title Docs | ✔ |

The Final Walkthrough

Usually, 24 hours before closing (or sometimes on the morning of), you will do a final walkthrough of the property with your real estate agent. This is not a home inspection; it is a verification visit.

You are checking to ensure:

- The seller has moved out and removed all debris.

- No new damage has occurred since the inspection.

- All appliances and fixtures included in the sale are present and working.

- The home is “broom clean.”

If you find issues (e.g., a hole in the wall from movers or a missing chandelier), do not panic. Call your attorney immediately. They can often hold back funds in escrow at the closing table to cover repairs, allowing the closing to proceed.

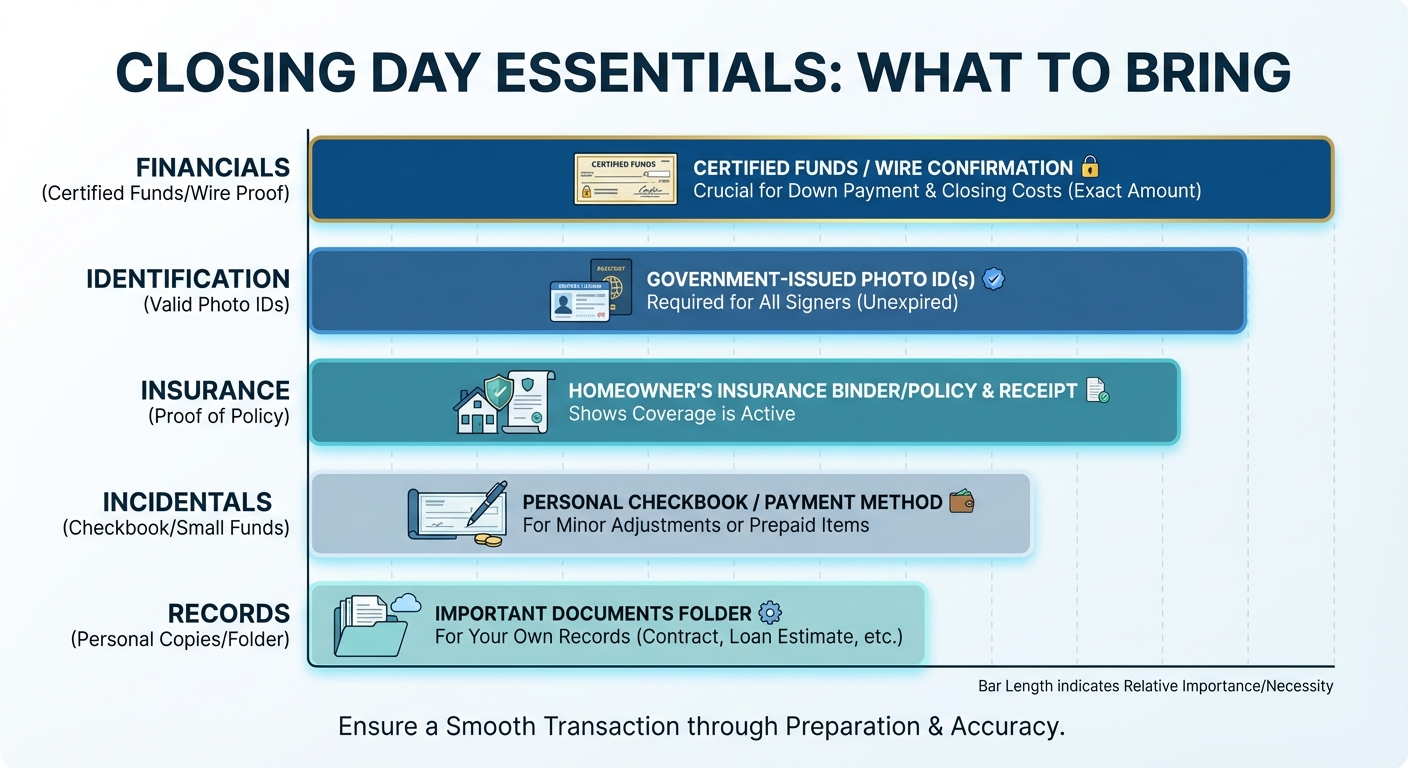

What to Bring to Closing Day

- Government-Issued Photo ID: A driver’s license or passport. All borrowers must be present and identifiable.

- Certified Funds: Personal checks are generally not accepted for the down payment and closing costs. You will need a cashier’s check or proof of a wire transfer. Note: Always verify wire instructions with your attorney over the phone to prevent fraud.

- Proof of Homeowners Insurance: A binder or receipt showing the first year’s premium is paid.

- Your Spouse: If you are married, your spouse may need to sign documents even if they are not on the loan (due to spousal rights in New York). Check with your attorney beforehand.

- Patience: Closings can take anywhere from one to three hours.

Common Closing Day Hiccups (And How We Avoid Them)

At RCG Mortgage, we pride ourselves on efficiency. We work hard to prevent the common issues that delay closings. However, being aware of them helps you stay prepared.

1. Funding Delays

2. Unexpected Changes in Credit

Lenders often do a final “soft pull” of your credit right before closing. Do not buy a new car, furniture on credit, or open new credit cards during the mortgage process. This can change your debt-to-income ratio and kill the deal at the last minute.

3. Name Misspellings

Why Choose a Local Hauppauge Broker?

You might wonder, “Why not just use a big online bank?” The answer lies in local expertise and accountability. As a Hauppauge-based mortgage broker, RCG Mortgage understands the nuances of the Long Island market.

We know the local attorneys, we know the tax structures in Suffolk County, and we are accessible. You aren’t calling a 1-800 number; you are calling Andrew Russell and a team that treats your mortgage with the seriousness it deserves. We offer the variety of loan options that brokers are known for, with the personalized service of a boutique firm.

Frequently Asked Questions (FAQs)

1. How long does the actual closing appointment take?

In New York, a typical closing takes about 1 to 2 hours. This includes reviewing and signing a significant stack of legal documents. If there are disputes over the final walkthrough or delays in wiring funds, it can take longer.

2. Can I sign my closing documents digitally?

While much of the mortgage application process with RCG Mortgage is digital and efficient, the final closing in New York usually requires “wet signatures” (ink on paper) for documents that need to be recorded with the county clerk, such as the Deed and Mortgage. Your attorney will guide you on this.

3. What is “Cash to Close”?

“Cash to Close” is the total amount of money you need to provide on closing day. This includes your down payment plus closing costs (attorney fees, title insurance, taxes, pre-paid items), minus any earnest money deposit you already made.

4. What happens if the wire transfer doesn’t arrive on time?

If the bank’s wire misses the federal cutoff time, the closing is “dry,” meaning you sign the papers, but the keys aren’t released until the money hits the account the next morning. RCG Mortgage coordinates closely with lenders to avoid this scenario.

5. Should I bring my checkbook to closing?

Yes! While the bulk of the money must be a cashier’s check or wire, there are often small adjustments (e.g., $50 for fuel oil left in the tank or a minor tax calculation adjustment). A personal check can usually cover these small differences.

Ready to Start Your Journey to Homeownership?

Closing day should be a celebration, not a headache. The difference between a stressful transaction and a smooth one often comes down to the team you build. By choosing RCG Mortgage, you are choosing a broker dedicated to transparency, speed, and a world-class experience.

Whether you are a first-time homebuyer in Hauppauge or looking to refinance on Long Island, we are here to guide you from application to the closing table.

Contact RCG Mortgage today for a no-obligation quote.

Phone: (516) 246-6353

Email: andrew@rcgmortgage.com

Office: 490 Wheeler Rd Suite 252, Hauppauge, NY 11788

Get Started with RCG Mortgage Now

Related Posts