Understanding Teacher and Public Servant Loans in Hauppauge, NY If you dedicate your life to…

Master Your Finances with a Debt Consolidation Mortgage in Hauppauge, NY

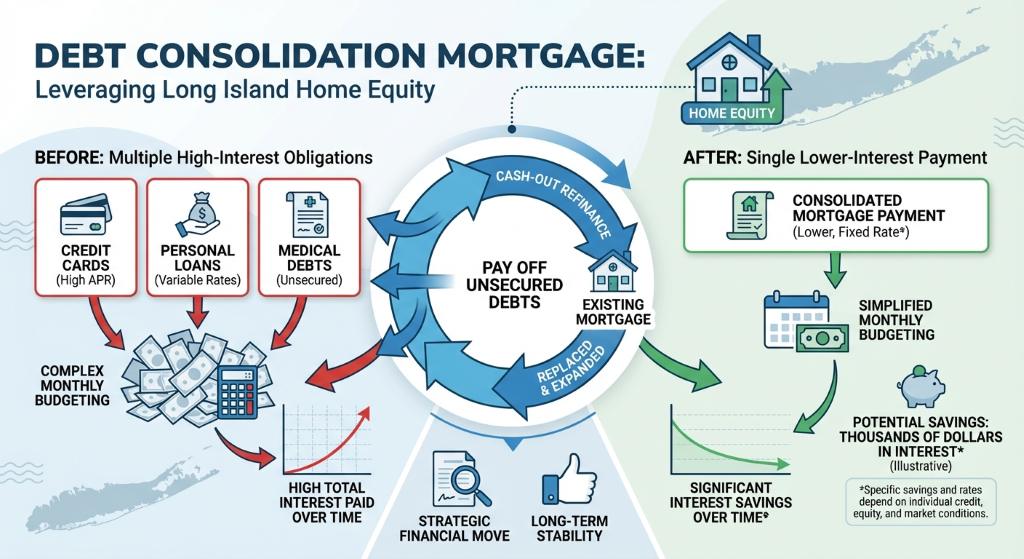

Understanding Your Debt Consolidation Options

Are high-interest credit cards and personal loans keeping you from achieving your financial goals? For many homeowners in Hauppauge and across Long Island, a debt consolidation mortgage offers a strategic path to financial freedom. By rolling high-interest debts into a single, lower-interest home loan, you can significantly reduce your monthly payments and simplify your financial life.

- Lower Interest Rates: Mortgage rates are typically much lower than credit card rates.

- Single Monthly Payment: A Debt Consolidation Loan streamlines your bills into one predictable payment.

- Improved Cash Flow: Free up your monthly budget for savings or investments.

At RCG Mortgage, we specialize in helping Long Island homeowners navigate their debt consolidation options. Whether you are considering a cash-out refinance or exploring a home equity loan or second mortgage, our team is here to guide you. We are also experts at providing second opinions on debt consolidation mortgages to ensure you are getting the absolute best terms for your unique situation.

How a Debt Consolidation Mortgage Works

A debt consolidation mortgage allows you to leverage the equity you have built in your Long Island home to pay off unsecured debts. When you choose this financial strategy, you are essentially replacing multiple high-interest obligations with a single mortgage payment. This process not only simplifies your monthly budgeting but can also save you thousands of dollars in interest over time.

There are two primary ways to achieve this:

- Cash-Out Refinance: This involves replacing your existing mortgage with a new loan for a larger amount than you currently owe. You receive the difference in cash, which you then use to pay off your outstanding debts.

- Home Equity Loan or Line of Credit: If you already have a fantastic rate on your primary mortgage, taking out a second mortgage might be the smarter move. This leaves your original mortgage untouched while giving you the funds needed for debt consolidation.

Because the real estate market in Hauppauge, NY has seen steady appreciation, many homeowners have more equity than they realize. Andrew Russell and the award-winning team at RCG Mortgage can help you determine exactly how much equity you have available to put toward a Debt Consolidation Loan.

| Debt Type | Average Interest Rate | Typical Term | Monthly Payment Impact |

|---|---|---|---|

| Credit Cards | 18% to 25% | Revolving | High |

| Personal Loans | 10% to 30% | 2 to 5 Years | Medium to High |

| Debt Consolidation Mortgage | 6% to 8% | 15 to 30 Years | Low (Consolidated) |

Why Choose RCG Mortgage for Your Debt Consolidation Journey

Finding the right mortgage broker is crucial when restructuring your finances. As a multi-year recipient of the NAMB Mortgage Broker of the Year award, RCG Mortgage prides itself on delivering transparent, tailored mortgage solutions. We do not just process loans; we analyze your complete financial picture to ensure a debt consolidation mortgage truly benefits you.

If you have already received a quote from another lender, do not hesitate to reach out to us. We are experts at providing second opinions on debt consolidation mortgages. Often, homeowners find that our local expertise and extensive network of lenders allow us to offer better rates or lower fees than their initial offers.

Taking control of your debt is a major step. Let our trusted Long Island mortgage brokers provide the clarity and confidence you need to secure a brighter financial future.

Q1: What is a debt consolidation mortgage?

It is a home loan that allows you to use your home equity to pay off high-interest debts, combining them into one lower-interest monthly payment.

Q2: Does a debt consolidation loan hurt my credit score?

Initially, applying for a new loan may cause a slight dip in your credit score. However, paying off maxed-out credit cards can significantly lower your credit utilization ratio, which often improves your score over time.

Q3: Is a cash-out refinance better than a second mortgage for debt consolidation?

The best choice depends on your current mortgage rate. If your current rate is very low, a second mortgage might be better. If current rates are lower than your existing mortgage, a cash-out refinance could be ideal.

Q4: How much equity do I need to consolidate debt?

Most lenders require you to retain at least 15 to 20 percent equity in your home after the new loan is finalized. Our team in Hauppauge can help calculate your available equity.

Q5: Can RCG Mortgage review an offer I received from another lender?

Absolutely. We are experts at providing second opinions on debt consolidation mortgages and can help you determine if you are getting the best possible terms.

Related Posts