Understanding First-Time Buyer Loans and Exploring Your Options Stepping into the real estate market is…

The Ultimate Guide to a HELOC Home Equity Line of Credit in Hauppauge, NY

Understanding How a Home Equity Line of Credit Works

If you are a homeowner in Hauppauge, NY, looking to tap into your home’s value, a heloc home equity line of credit might be the perfect financial tool for you. A HELOC allows you to borrow against the equity you have built in your property, functioning much like a credit card where you can draw funds as needed. At RCG Mortgage, our award-winning team led by Andrew Russell is dedicated to helping Long Island residents navigate their home financing options.

Many homeowners use a home equity line of credit for major expenses like home renovations, debt consolidation, or unexpected emergencies. However, choosing the right structure is crucial. We are experts at providing second opinions on HELOCs to ensure you are getting the best possible terms for your unique financial situation.

- Flexible borrowing limits based on your home equity

- Only pay interest on the amount you actually draw

- Potential tax benefits for home improvements (consult a tax advisor)

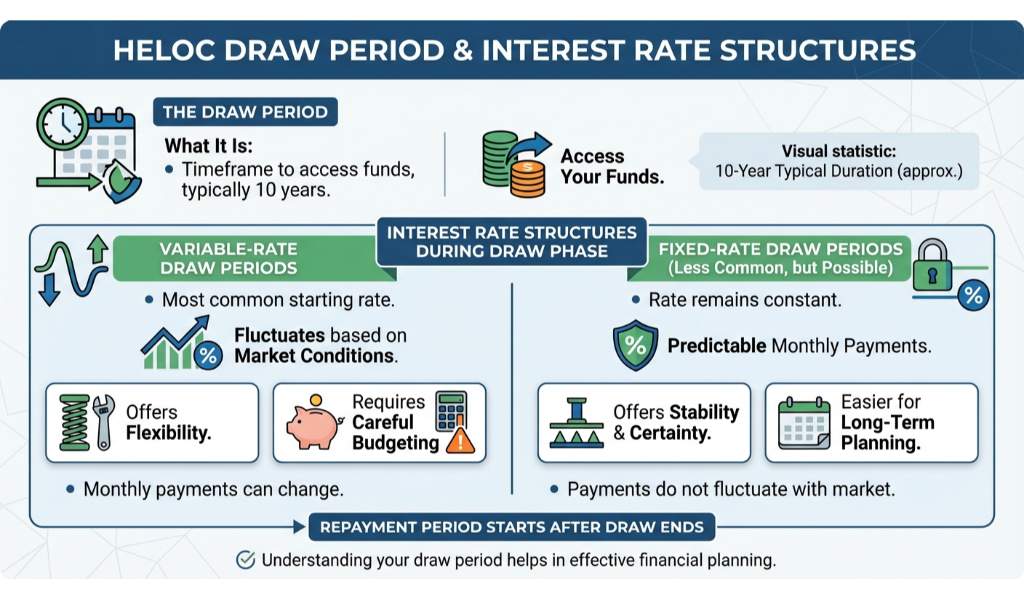

Variable-Rate vs. Fixed-Rate Draw Periods

When setting up your heloc home equity line of credit, understanding the draw period is essential. This is the timeframe, typically 10 years, during which you can access your funds. You will generally encounter two main types of interest rate structures during this phase:

Variable-Rate Draw Periods: Most HELOCs start with a variable interest rate. This means your monthly payments can fluctuate based on market conditions. It offers flexibility, but it requires careful budgeting since your minimum payment could increase.

Fixed-Rate Draw Periods: Some lenders offer the option to lock in a portion of your balance at a fixed interest rate. This provides predictable monthly payments, shielding you from rising interest rates. If you prefer absolute stability, you might also consider comparing a HELOC against a home equity loan second mortgage or a cash-out refinance to see which product best aligns with your goals.

Not sure which option is right for you? Our Hauppauge mortgage brokers are always available to offer a complimentary second opinion on your current HELOC offer.

| Financing Option | Interest Rate Type | Access to Funds | Best For |

|---|---|---|---|

| Variable-Rate HELOC | Fluctuating | Revolving line of credit | Ongoing projects with uncertain costs |

| Fixed-Rate HELOC Option | Fixed on drawn amount | Revolving line of credit | Borrowers wanting predictable payments |

| Home Equity Loan | Fixed | Lump sum | Large, one-time expenses |

| Cash-Out Refinance | Fixed or Variable | Lump sum (replaces primary mortgage) | Accessing large equity while securing a new rate |

Why Choose RCG Mortgage for Your HELOC Needs?

As the top Mortgage Broker in Long Island and New York, RCG Mortgage prides itself on operating with integrity and excellence. Securing a heloc home equity line of credit is a significant financial decision, and having a trusted local expert by your side makes all the difference. Andrew Russell and our dedicated team in Hauppauge, NY, take the time to analyze your financial goals, ensuring your HELOC structure maximizes your benefits.

Remember, we are experts at providing second opinions on HELOCs. If you already have an offer from another institution, let us review it. We often find better terms, lower fees, or more favorable draw period conditions for our clients.

Compliance Note: All loans are subject to credit approval, income verification, and property appraisal. Rates and terms are subject to change without notice. RCG Mortgage is an Equal Housing Lender.

Q1: What exactly is a HELOC home equity line of credit?

A HELOC is a revolving line of credit secured by your home’s equity. You can draw funds as needed up to a certain limit, making it ideal for ongoing expenses like renovations.

Q2: How does the draw period work on a HELOC?

The draw period is the initial phase of the loan, usually lasting 10 years. During this time, you can access funds and typically only need to make interest payments on the amount you have borrowed.

Q3: Can I switch from a variable rate to a fixed rate?

Many modern HELOCs offer a fixed rate option, allowing you to lock in a specific interest rate on a portion of your outstanding balance to protect against market fluctuations.

Q4: How does a HELOC differ from a cash out refinance?

A cash out refinance replaces your primary mortgage with a new, larger loan, giving you the difference in cash. A HELOC is a separate, second mortgage that does not alter your primary mortgage terms.

Q5: Why should I get a second opinion on my HELOC offer?

Lenders offer vastly different terms, rates, and fees. Getting a second opinion from our Hauppauge mortgage experts ensures you are not overpaying and that the loan structure fits your long term goals.

Related Posts