Why Choose a 30-Year Fixed-Rate Mortgage? When it comes to financing your dream home in…

The Complete Guide to Assumable Mortgages in Hauppauge, NY

What is an Assumable Mortgage?

In today’s dynamic real estate market, securing a low interest rate can feel like a daunting task. This is where an assumable mortgage (also known as a mortgage assumption) becomes an incredibly valuable tool. An assumable mortgage allows a homebuyer to take over the seller’s existing home loan, keeping the exact same interest rate, repayment period, and current principal balance.

For homebuyers in Hauppauge, NY, and across Long Island, this strategy can translate to massive long-term savings if the seller locked in a historically low rate years ago. However, it is important to note that not all loans are eligible for assumption. Typically, conventional loans cannot be assumed because they contain a due-on-sale clause. Instead, government-backed loans are the primary vehicles for a mortgage assumption.

At RCG Mortgage, we are experts at providing second opinions on assumable mortgages. Whether you are considering an assumption, exploring a FHA purchase loan, or weighing other financing avenues, our award-winning team is here to help you navigate the complex fine print.

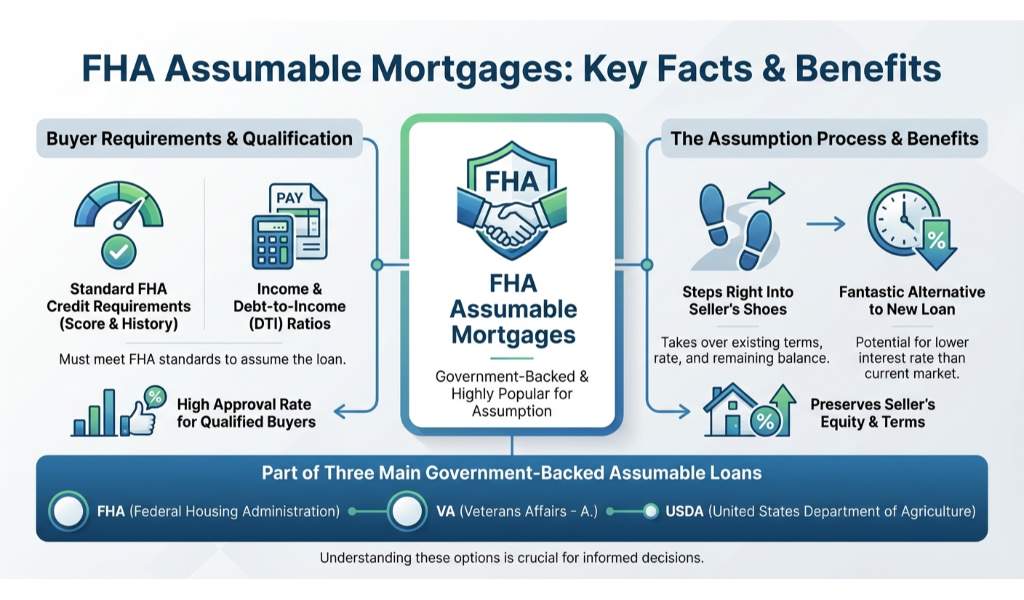

Types of Assumable Mortgages: FHA, VA, and USDA

When looking into an assumable mortgage, it is crucial to understand the three main types of government-backed loans that allow for mortgage assumption:

- FHA Assumable Mortgages: Backed by the Federal Housing Administration, these loans are highly popular for assumption. The buyer must meet standard FHA credit and income requirements. If approved, the buyer steps right into the seller’s shoes, making an FHA assumable loan a fantastic alternative to originating a brand new FHA purchase loan.

- VA Assumable Mortgages: Department of Veterans Affairs loans offer incredible benefits. Interestingly, you do not always need to be a military veteran to assume a VA loan. However, if a non-veteran assumes the loan, the original veteran seller’s VA entitlement remains tied to the property until the loan is paid off. If you are a veteran, you might also consider a standard VA purchase loan to utilize your own entitlement fully.

- USDA Assumable Mortgages: Designed for rural and suburban homebuyers, USDA loans also feature assumability. The new buyer must meet the USDA’s strict income limits and location requirements to qualify for this type of mortgage assumption.

Keep in mind that assuming a mortgage often requires paying the seller the difference between the home’s purchase price and the remaining loan balance. If you do not have the cash on hand to cover this equity gap, you might need a second mortgage, or you could explore a rate and term refinance down the road to consolidate your financing.

| Loan Type | Assumable? | Special Requirements for Assumption |

|---|---|---|

| FHA Loan | Yes | Buyer must meet standard FHA credit, debt-to-income, and income guidelines. |

| VA Loan | Yes | Buyer must meet VA standards. The seller’s VA entitlement remains tied up unless the buyer is an eligible veteran who substitutes their own entitlement. |

| USDA Loan | Yes | Buyer must meet strict USDA income limits and property location rules. |

| Conventional Loan | Rarely | Typically contains a due-on-sale clause preventing assumption. |

Why Get a Second Opinion on Your Mortgage Assumption?

Navigating an assumable mortgage can be incredibly complex. The original lender must approve the assumption, the timeline can be longer than a traditional closing, and the paperwork can be daunting. Because these transactions are highly unique, many buyers and sellers receive conflicting information from real estate agents or standard retail lenders.

That is exactly why you need a trusted Long Island mortgage broker in your corner. At RCG Mortgage in Hauppauge, NY, we are experts at providing second opinions on assumable mortgages. Led by Andrew Russell, our team has been recognized as the NAMB Mortgage Broker of the Year from 2022 to 2025. We thoroughly review your financial scenario, calculate the equity gap, and ensure the mortgage assumption is truly in your best financial interest.

Q1: What is an assumable mortgage?

An assumable mortgage allows a homebuyer to take over the seller’s existing loan terms, including their exact interest rate, remaining loan balance, and repayment schedule.

Q2: Are conventional loans assumable?

No, conventional loans generally have a due-on-sale clause that requires the loan to be paid in full when the property is sold, making them ineligible for assumption.

Q3: Do I need to be a veteran to assume a VA loan?

No, non-veterans can assume a VA loan. However, the original seller’s VA entitlement will remain tied to the home until the loan is fully paid off, which may affect their ability to secure another VA loan.

Q4: How do I cover the equity gap in a mortgage assumption?

If the home’s purchase price is higher than the remaining loan balance, the buyer must cover the difference in cash or secure secondary financing to make up the gap.

Q5: Why should I get a second opinion on an assumable mortgage?

Assumption processes are complicated and not always the best financial move depending on the equity gap and lender fees. Getting a second opinion from the experts at RCG Mortgage ensures you are making a sound, fully informed decision.

Related Posts