What is a Doctor Mortgage Loan? Medical and legal professionals face unique financial challenges. From…

Cash-Out Refinance vs. HELOC: The Ultimate Guide to Funding Home Improvements in Hauppauge, NY

Cash-Out Refinance vs. HELOC: The Ultimate Guide to Funding Home Improvements in Hauppauge, NY

If you are a homeowner in Hauppauge, New York, you have likely watched your property value climb over the last few years. Whether you own a classic colonial near Blydenburgh Park or a ranch closer to the Northern State Parkway, your home is more than just a place to live—it is likely your most valuable financial asset.

With housing inventory tight across Long Island, many Hauppauge residents are choosing to renovate rather than relocate. Whether you are dreaming of a chef’s kitchen, a finished basement for the kids, or an outdoor oasis to enjoy the New York summers, the biggest question isn’t usually “what to build,” but rather “how to pay for it.”

Two of the most popular methods for leveraging your home’s equity are the Cash-Out Refinance and the Home Equity Line of Credit (HELOC). Both have distinct advantages, but the right choice depends entirely on your financial goals, your current mortgage rate, and the scope of your renovation project.

At RCG Mortgage, led by Andrew Russell, we believe in providing the “Nordstrom” experience with “Ford” assembly line efficiency. We are here to help you navigate these options with transparency and local expertise right here in Hauppauge.

The Hauppauge Housing Landscape: Why Renovate Now?

Hauppauge is a unique market within Suffolk County. With excellent schools and proximity to major business hubs, holding onto real estate here is a smart long-term play. However, many homes in the area built in the 1970s and 80s are ready for modernization.

By reinvesting in your property, you aren’t just improving your quality of life; you are potentially increasing the resale value of your home. However, funding these improvements with high-interest credit cards or personal loans can be financial suicide. Utilizing your home’s equity is generally the most cost-effective strategy.

Option 1: The Cash-Out Refinance

What is a Cash-Out Refinance?

A cash-out refinance involves replacing your current mortgage with a new, larger loan. You pay off your existing mortgage balance and take the difference between the two loans in tax-free cash. This gives you a lump sum of money that you can use for home improvements, debt consolidation, or other financial needs.

How It Works

Let’s say your home in Hauppauge is valued at $700,000, and you owe $400,000 on your current mortgage. You have $300,000 in equity. If you want $50,000 for a kitchen renovation, you would refinance your home for $450,000. This pays off the original $400,000 and puts $50,000 in your pocket (minus closing costs).

The Pros of a Cash-Out Refinance

- Fixed Interest Rates: Unlike HELOCs, which often have variable rates, a cash-out refinance typically locks you into a fixed rate for 15 or 30 years. This provides stability and predictable monthly payments.

- Lower Interest Rates: First mortgages generally carry lower interest rates compared to second mortgages (like HELOCs) or personal loans.

- Longer Repayment Terms: You can spread the cost of your renovation over up to 30 years, keeping your monthly obligation lower.

- Debt Consolidation: In addition to renovations, you can use the extra cash to pay off high-interest credit card debt, effectively rolling it into a tax-deductible mortgage payment (consult your tax advisor).

The Cons of a Cash-Out Refinance

- Closing Costs: Since this is a new mortgage, you will have to pay closing costs, which can range from 2% to 5% of the loan amount.

- Resetting the Clock: If you have been paying your mortgage for 10 years and refinance into a new 30-year term, you are extending the time it takes to become debt-free.

- Rate Sensitivity: If your current mortgage rate is historically low (e.g., from 2020 or 2021), refinancing into today’s market rates might increase your interest expense significantly on the entire balance, not just the cash-out portion.

Option 2: The Home Equity Line of Credit (HELOC)

What is a HELOC?

A HELOC is a revolving line of credit secured by your home. It functions similarly to a credit card. You are approved for a specific limit based on your equity, and you can draw from it, pay it back, and draw again during the “draw period” (usually 10 years).

How It Works

Using the same example: Your home is worth $700,000, and you owe $400,000. A lender might approve you for a $50,000 HELOC. You keep your original mortgage exactly as it is. You now have a “second mortgage” available to use. If you only use $10,000 for a bathroom update, you only pay interest on that $10,000.

The Pros of a HELOC

- Keep Your First Rate: The biggest advantage is that you do not touch your primary mortgage. If you have a 3% rate on your main loan, you keep it.

- Flexibility: You only pay interest on the money you actually use. This is perfect for ongoing projects where costs might fluctuate.

- Lower Closing Costs: HELOCs often come with very low or zero closing costs compared to a full refinance.

- Interest-Only Options: Many HELOCs allow for interest-only payments during the draw period, keeping initial costs low while construction is happening.

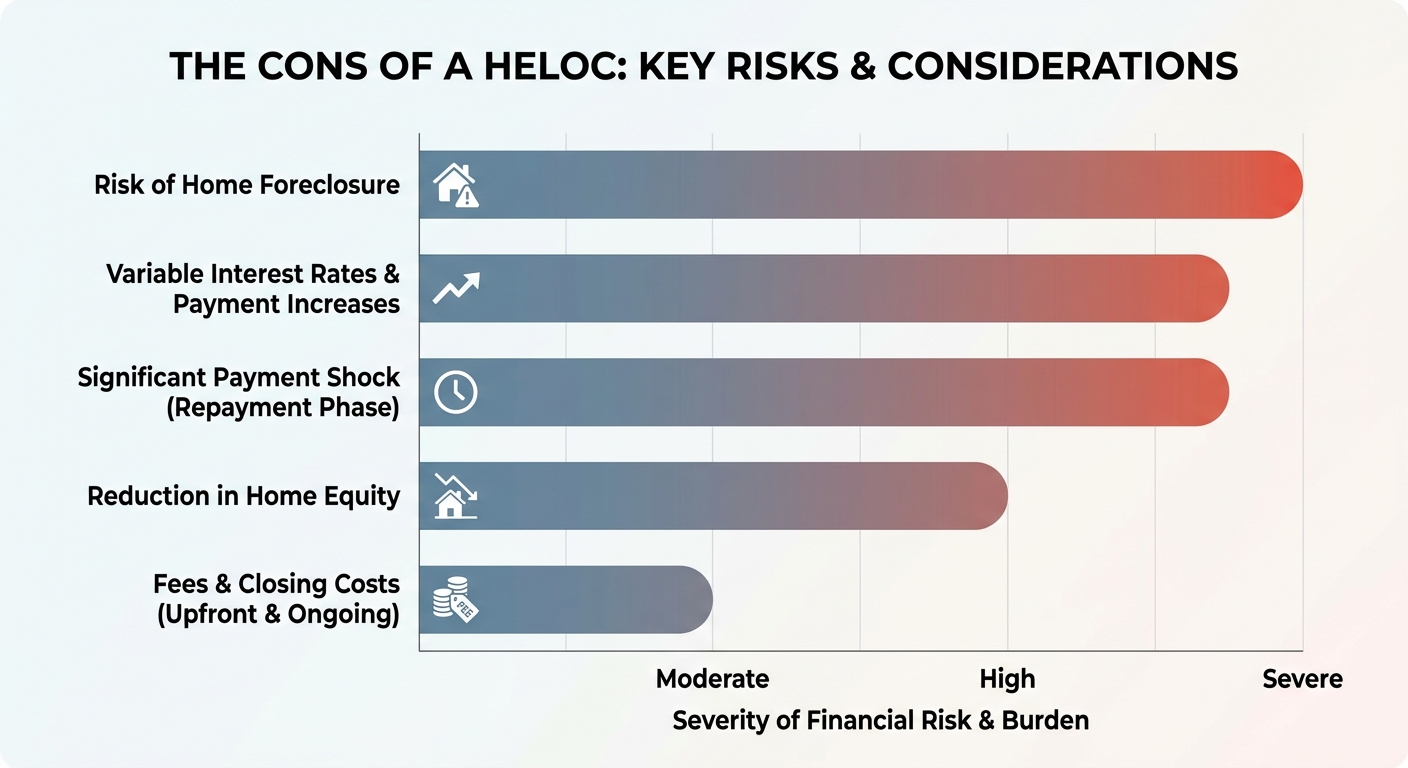

The Cons of a HELOC

- Variable Interest Rates: Most HELOCs have variable rates tied to the Prime Rate. If the Federal Reserve raises rates, your HELOC payment goes up immediately.

- Payment Shock: Once the draw period ends (usually after 10 years), the loan converts to a repayment period where you must pay principal and interest. This can lead to a significant jump in monthly payments.

- Harder to Qualify: In uncertain economic times, banks may tighten guidelines for second mortgages more aggressively than for primary mortgages.

Side-by-Side Comparison: Cash-Out Refi vs. HELOC

| Feature | Cash-Out Refinance | HELOC |

|---|---|---|

| Loan Type | Replaces your existing mortgage | Second mortgage (adds to existing) |

| Interest Rate | Typically Fixed Rate | Typically Variable Rate |

| Disbursement | Lump Sum at closing | Draw as needed (Revolving) |

| Closing Costs | Higher (Standard mortgage costs) | Lower (often minimal fees) |

| Monthly Payment | Stable (Principal + Interest) | Fluctuates (Interest-only options available) |

| Best For | Large, one-time projects & debt consolidation | Ongoing projects or emergency access |

Which Option is Right for Your Project?

Scenario A: The Major Overhaul

The Project: You are adding a second story or doing a complete gut-renovation of your kitchen and bathrooms. The cost is fixed at roughly $100,000, and you want to get it done in one shot.

The Verdict: A Cash-Out Refinance is often the winner here. You get the full amount upfront to pay contractors. Because the balance is high, locking in a fixed rate provides protection against future rate hikes, ensuring your budget stays predictable.

Scenario B: The Staggered Upgrade

The Project: You want to finish the basement this spring, maybe do the roof next year, and handle the landscaping whenever you have time.

The Verdict: A HELOC is likely the better fit. You don’t want to pay interest on $50,000 if you are only spending $15,000 right now. The flexibility allows you to borrow, pay back, and borrow again as your home evolves.

The RCG Mortgage Advantage: Why Work with a Local Broker?

When you are looking for mortgage solutions in Hauppauge, you might be tempted to walk into a big bank branch. However, big banks often have limited product lines and stricter underwriting “boxes” that you must fit into.

At RCG Mortgage, located right here at 490 Wheeler Rd in Hauppauge, we operate differently. As a mortgage broker, we have access to multiple lenders, allowing us to shop for the loan that fits your lifestyle, not the bank’s quota.

Why choose RCG Mortgage?

- We Are Local Experts: We understand the Long Island market, from property tax nuances to local appraisal trends.

- Award-Winning Service: Andrew Russell has been recognized as the NAMB Mortgage Broker of the Year (2022-2025) and is ranked as the #1 Loan Originator in Long Island and New York by Scotsman Guide (2024).

- Speed and Efficiency: We pride ourselves on simplifying the underwriting process. We handle the heavy lifting so you can focus on choosing paint colors and tile samples.

- Tailored Solutions: Whether it’s a standard Conventional loan, FHA, VA, or a Non-QM loan for self-employed borrowers, we find the path that works for you.

We believe that transparency and accountability are the cornerstones of our business. We will sit down with you, look at your current interest rate, analyze your equity position, and give you an honest recommendation on whether a Cash-Out Refinance or a HELOC makes the most financial sense for you.

Frequently Asked Questions (FAQs)

1. Can I deduct the interest on a Cash-Out Refinance or HELOC?

Generally, yes, if the funds are used to “buy, build, or substantially improve” your home. The Tax Cuts and Jobs Act of 2017 placed some limits on this deduction, particularly for HELOCs used for non-housing expenses (like paying off credit cards). We always recommend consulting with a qualified tax professional to understand your specific situation.

2. How much equity do I need to qualify for a cash-out refinance in Hauppauge?

Most lenders require you to maintain at least 20% equity in your home after the refinance. This means the maximum Loan-to-Value (LTV) ratio is usually 80%. For example, if your home is worth $500,000, your new loan amount typically cannot exceed $400,000. However, VA loans may allow for up to 100% cash-out for eligible veterans.

3. Does RCG Mortgage handle renovation loans?

Yes! In addition to cash-out refinances, we offer Rehab loans that allow you to roll the costs of renovation directly into your mortgage. This can be a great option if you are buying a “fixer-upper” in Hauppauge and need funds immediately to make it livable.

4. Will a Cash-Out Refinance affect my credit score?

Initially, you may see a small dip in your credit score due to the hard inquiry and the new loan appearing on your report. However, if you use the funds to pay off high-utilization credit cards, your score often rebounds quickly and may even increase significantly due to the improved credit utilization ratio.

5. How long does the process take with RCG Mortgage?

While timelines can vary based on the complexity of the loan, working with a broker like RCG Mortgage is often faster than working with a traditional bank. We streamline the document collection and underwriting process. Typically, a refinance can close in 30 to 45 days.

Ready to Transform Your Home?

Your dream home doesn’t have to be a new address—it can be the one you are living in right now. Whether you decide on a Cash-Out Refinance or a HELOC, leveraging your equity is a powerful financial tool when done correctly.

Don’t navigate the complex mortgage landscape alone. Partner with a trusted Long Island mortgage broker who puts your interests first.

Contact Andrew Russell and the RCG Mortgage team today for a no-obligation quote and let’s build your future together.

Or call us directly at (516) 246-6353 to speak with a loan expert.

Related Posts