What is an Assumable Mortgage? In today's dynamic real estate market, securing a low interest…

Your Complete Guide to a Conventional Fixed-Rate Mortgage in Hauppauge, NY

Understanding the Basics of a Conventional Mortgage

When you are ready to buy a home in Hauppauge, NY, choosing the right financing is one of the most critical steps. A conventional mortgage is a home loan that is not backed by a government agency. Instead, it is offered by private lenders like RCG Mortgage. For many homebuyers, a conventional fixed-rate mortgage provides the perfect blend of predictable monthly payments and competitive interest rates.

We specialize in helping Long Island residents secure the best possible terms for their home purchase. In fact, we are experts at providing second opinions on conventional mortgages. If you already have a quote, let our award-winning team review it to ensure you are getting the most value.

Conventional loans generally fall into two main categories:

- Conforming Loans: These loans meet the funding criteria set by Fannie Mae and Freddie Mac, including specific loan limits.

- Non-Conforming Loans: These loans exceed the standard limits or have unique requirements, often referred to as jumbo loans.

Choosing a 30-year fixed-rate mortgage under the conventional umbrella means your interest rate will remain exactly the same for the entire life of the loan, offering incredible stability for your family budget.

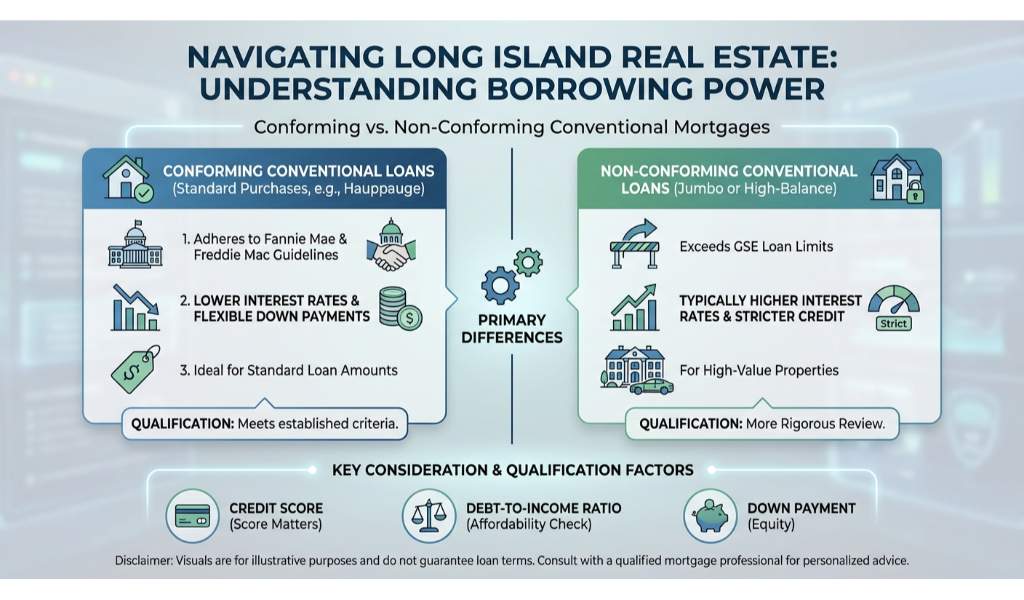

Conforming vs. Non-Conforming: Which is Right for You?

Navigating the Long Island real estate market requires a clear understanding of your borrowing power. The primary difference between conforming and non-conforming conventional mortgages lies in the loan amount and the strictness of the credit requirements.

Conforming conventional loans are ideal for standard home purchases in Hauppauge. Because they adhere to guidelines set by Fannie Mae and Freddie Mac, they typically offer lower interest rates and more flexible down payment options. To qualify, borrowers generally need a solid credit score and a manageable debt-to-income ratio.

On the other hand, if you are looking at luxury properties or homes in high-cost areas of New York, you might exceed the federal loan limits. This is where a non-conforming loan, specifically a jumbo mortgage, comes into play. Jumbo loans require stricter underwriting standards, including higher credit scores and larger down payments, because the lender is taking on more risk without government or Fannie Mae backing.

Not sure which category your dream home falls into? RCG Mortgage is here to help. We are experts at providing second opinions on conventional mortgages, ensuring you are matched with the exact product that fits your financial profile.

| Loan Type | 2024 Loan Limit (Most Areas) | Minimum Down Payment | Typical Minimum Credit Score |

|---|---|---|---|

| Conforming Conventional | $766,550 | 3% to 5% | 620 |

| High-Cost Area Conforming (NY) | Up to $1,149,825 | 5% | 620 |

| Non-Conforming (Jumbo) | Exceeds $1,149,825 | 10% to 20% | 700+ |

Why Choose RCG Mortgage for Your Home Financing?

At RCG Mortgage, we pride ourselves on being a top-rated Long Island mortgage broker. Recognized as the Mortgage Broker of the Year from 2022 to 2025 by NAMB, our team, led by Andrew Russell, operates with integrity and excellence. Whether you are exploring a conventional mortgage or considering government-backed options like an FHA purchase loan, we provide tailored solutions for your unique needs.

Getting a second opinion on your mortgage quote can save you thousands of dollars over the life of your loan. We invite you to bring us your current pre-approvals. Our team will meticulously review the interest rate, monthly payment, and term options to guarantee you are receiving the best possible deal.

Compliance Notice: All loans are subject to credit and property approval. Rates, program terms, and conditions are subject to change without notice. RCG Mortgage is an Equal Housing Lender. By providing your contact information, you agree to our Terms of Service and Privacy Policy, and consent to receive communications regarding your mortgage inquiry.

Q1: What is a conventional fixed-rate mortgage?

A conventional fixed-rate mortgage is a home loan not insured by the federal government that features an interest rate that remains exactly the same for the entire duration of the loan.

Q2: How much of a down payment do I need for a conventional mortgage?

First-time homebuyers can often secure a conventional mortgage with as little as 3% down, though a 20% down payment will help you avoid paying private mortgage insurance (PMI).

Q3: What is the difference between a conforming and non-conforming loan?

A conforming loan meets the maximum loan limits and guidelines set by Fannie Mae and Freddie Mac. A non-conforming loan exceeds these limits or has different qualifying criteria, often referred to as a jumbo loan.

Q4: Can I get a second opinion on my conventional mortgage quote?

Absolutely. At RCG Mortgage, we are experts at providing second opinions on conventional mortgages to ensure you are getting the most competitive rate and terms available in Hauppauge, NY.

Q5: Is a conventional loan better than an FHA loan?

It depends on your financial situation. Conventional loans are typically better for borrowers with strong credit scores and larger down payments, while FHA loans offer more flexibility for those with lower credit scores.

Related Posts