VA Loans in Hauppauge: Exclusive Programs for Military Families in Suffolk County For veterans, active-duty…

Saving for a Down Payment in the New Year: Strategies for Hauppauge Residents

Saving for a Down Payment in the New Year: Strategies for Hauppauge Residents

As the calendar turns to a new year, resolutions are set in motion. For many residents in Hauppauge, NY, and across Long Island, the top goal for 2025 is clear: achieving the American Dream of homeownership. However, in the current economic climate, the biggest hurdle often isn’t the monthly mortgage payment—it’s the down payment.

If you are tired of renting or looking to upgrade from your current living situation, you might feel overwhelmed by the perception that you need a massive pile of cash to get started. At RCG Mortgage, we believe that transparency and education are the keys to unlocking your future home. Whether you are eyeing a single-family home near the hidden gems of Hauppauge or a condo closer to the LIE for an easier commute, saving for a down payment requires a mix of discipline, strategy, and knowing your financing options.

In this comprehensive guide, we will break down actionable strategies for saving, debunk common myths about how much you actually need, and explain why partnering with a local Hauppauge mortgage broker like Andrew Russell can save you money before you even reach the closing table.

Understanding the Hauppauge Real Estate Market

Before you set a savings goal, you need to understand the playing field. Hauppauge is a unique market within Suffolk County. It offers a blend of suburban tranquility, excellent industrial hubs, and highly rated schools. Because of its desirability, home prices here can be competitive.

However, “competitive” does not mean “impossible.” The first step in your savings journey is not cutting out coffee—it is defining your target. Are you looking for a starter home or a forever home? Understanding the price range of properties in the 11788 zip code helps you calculate exactly what your down payment percentage looks like in real dollars.

Debunking the 20% Down Myth

One of the most persistent myths in real estate is that you must save 20% of the home’s purchase price before you can buy. While putting 20% down eliminates Private Mortgage Insurance (PMI), it is not a requirement for most buyers. Believing this myth can delay your home purchase by years, during which home prices may rise further.

At RCG Mortgage, we specialize in a variety of loan programs that offer low down payment options tailored to your financial profile:

- FHA Loans: Ideal for first-time buyers, requiring as little as 3.5% down. This is a government-insured loan that offers flexibility with credit scores.

- Conventional Loans: Qualified buyers can purchase a home with as little as 3% down.

- VA Loans: For our brave veterans and active military in Hauppauge, VA loans often require 0% down.

- USDA Loans: Available in select rural and suburban areas, also offering 0% down payment options.

Comparison of Down Payment Requirements

Here is a breakdown of what a down payment might look like on a $500,000 home in the Hauppauge area based on different loan types:

| Loan Type | Minimum Down Payment % | Estimated Down Payment Amount ($500k Home) | Ideal Borrower Profile |

|---|---|---|---|

| Conventional 97 | 3% | $15,000 | Strong credit score, first-time homebuyers. |

| FHA Loan | 3.5% | $17,500 | Lower credit scores, higher debt-to-income ratios. |

| Conventional Standard | 5% | $25,000 | Buyers looking to lower monthly payments slightly. |

| VA Loan | 0% | $0 | Veterans, active-duty military, and eligible spouses. |

| Traditional | 20% | $100,000 | Investors or buyers wanting to avoid PMI immediately. |

Note: These figures are estimates for educational purposes. Contact RCG Mortgage for a precise quote based on your specific financial situation.

Strategic Budgeting: The “Ford Assembly Line” Approach

Andrew Russell, the founder of RCG Mortgage, often describes our service as providing a “Nordstrom experience coupled with a Ford assembly line.” We can apply this same “assembly line” efficiency to your personal budgeting.

1. Audit Your Local Expenses

Living on Long Island comes with specific costs—high utilities, commuting costs, and property taxes. To save effectively, you need to audit where your money is going. Print out your last three months of bank statements. Highlight every non-essential expense. You might find that you are spending hundreds a month on subscriptions you don’t use or dining out frequently.

2. The “Automate and Forget” Method

Willpower is a finite resource. The best way to save for a home in Hauppauge is to automate the process. Open a high-yield savings account specifically for your “House Fund.” Set up an automatic transfer from your checking account on payday. If you don’t see the money, you won’t spend it.

3. Reduce High-Interest Debt

Your ability to qualify for a mortgage is heavily influenced by your Debt-to-Income (DTI) ratio. While saving for a down payment is crucial, paying down high-interest credit cards can be equally important. It increases your borrowing power and frees up monthly cash flow that can then be diverted into your house fund.

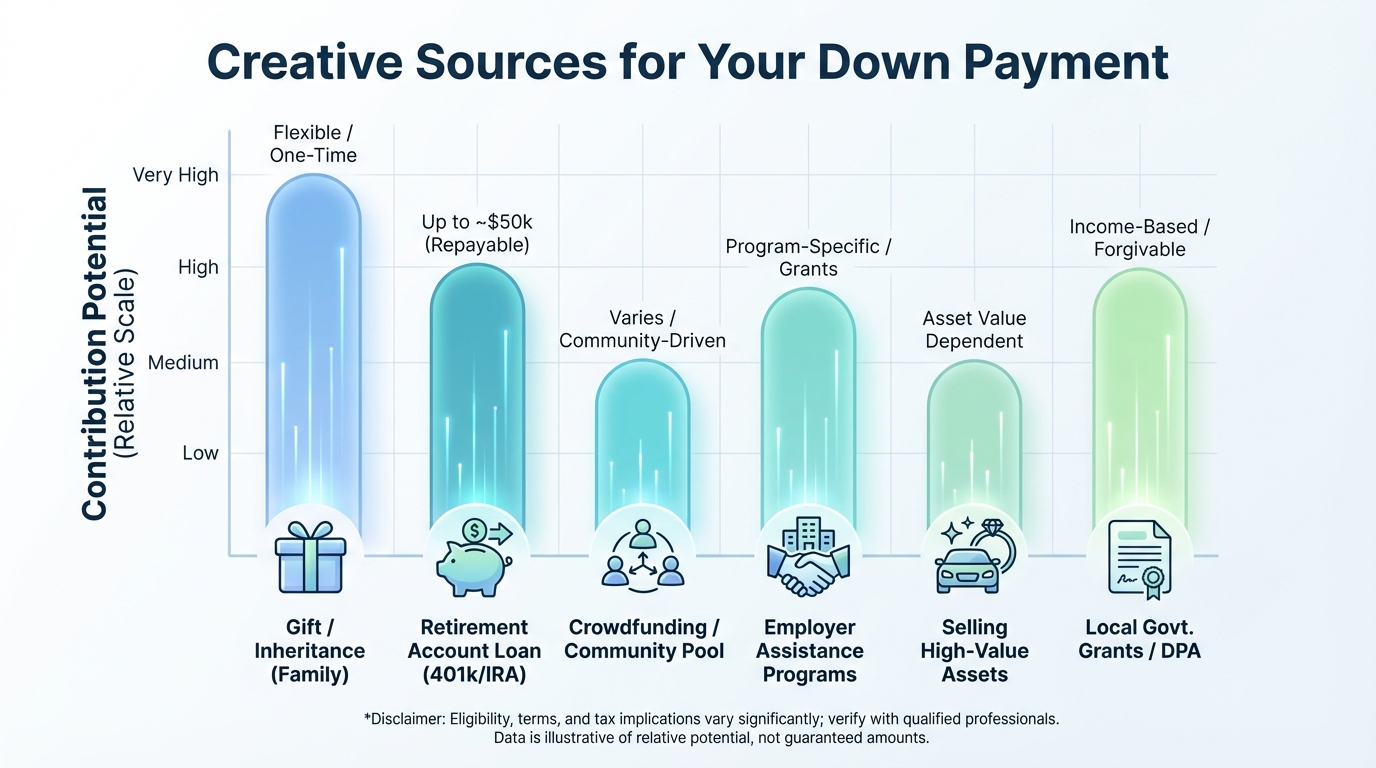

Creative Sources for Your Down Payment

Leveraging Gift Funds

Did you know that for many loan programs, including FHA and Conventional loans, your down payment can come entirely from gift funds? Family members often want to help with this major life milestone. If you have parents or relatives willing to contribute, this can bridge the gap immediately. RCG Mortgage can guide you on the proper documentation (gift letters) required to ensure these funds are accepted by underwriters.

Retirement Accounts (401k)

Tax Refunds and Bonuses

We are approaching tax season. Instead of viewing your tax refund as “fun money,” view it as a stepping stone to your new front door. Committing 100% of your tax refund and any year-end work bonuses directly to your house fund can accelerate your timeline by months.

Why “Shopping Local” for Your Mortgage Saves You Money

When saving for a home, every dollar counts. This brings us to a critical point: Big-Bank Fatigue. Many homebuyers in Hauppauge default to walking into a large retail bank because it feels familiar. However, this can be a costly mistake.

Brokers Do it Better… RCG Does it Best.

As an independent mortgage broker, RCG Mortgage works with multiple lenders. We aren’t tied to one bank’s products or rates. This allows us to shop on your behalf to find the best interest rate and the lowest closing costs. By securing a lower interest rate or a lender credit, we can potentially lower the amount of cash you need to bring to the closing table.

Big banks often have high overhead costs that are passed down to you in the form of junk fees or higher rates. Working with a local expert like Andrew Russell means you get:

- Access to Wholesale Rates: Often lower than retail bank rates.

- Speed and Efficiency: We simplify the underwriting process, helping you close faster.

- Tailored Solutions: We look at your whole picture, not just a credit score number.

Your 2025 Action Plan: A Month-by-Month Guide

To make this goal a reality, let’s break it down into a timeline:

- January: Pull your credit report and check for errors. Contact RCG Mortgage for a “Pre-Qualification” to understand your baseline.

- February: Execute your budget audit. Cancel unused subscriptions and set up your auto-draft savings.

- March: Use your tax refund to boost your savings account.

- April: Re-evaluate your savings progress. If you are close to your goal, begin casually looking at neighborhoods in Hauppauge.

- May: Get “Pre-Approved” (a more formal step than pre-qualification). This makes you a competitive buyer when the spring market heats up.

Frequently Asked Questions (FAQs)

1. Is it better to wait until I have 20% down to buy in Hauppauge?

Not necessarily. While 20% down avoids Private Mortgage Insurance (PMI), home prices in Long Island have historically appreciated. Waiting years to save 20% might mean the house that costs $500,000 today costs $550,000 by the time you are ready. It is often better to buy sooner with a lower down payment and start building equity.

2. Can I use a personal loan for my down payment?

Generally, no. Lenders want to see that the down payment comes from your own funds or an approved gift. Borrowing money for a down payment increases your debt load and is typically not allowed for the down payment portion of the transaction.

3. What are “closing costs,” and do I need to save for them too?

Yes. In addition to the down payment, you will have closing costs (taxes, title insurance, appraisal fees, etc.). In New York, these can range from 3% to 6% of the loan amount. However, RCG Mortgage can sometimes negotiate “seller concessions” where the seller pays a portion of your closing costs, reducing the cash you need upfront.

4. How does my credit score affect my down payment?

Your credit score affects your loan eligibility and interest rate more than the down payment percentage. However, for FHA loans, a score of 580+ usually qualifies you for the 3.5% down option. If your score is lower, you might be required to put down 10%. RCG Mortgage can help you understand where you stand.

5. Why should I choose RCG Mortgage over an online lender?

Real estate is local. Online lenders often lack the specific knowledge of New York property taxes and Hauppauge-specific regulations. Furthermore, in a competitive market, a pre-approval letter from a respected local broker like Andrew Russell carries more weight with listing agents than a generic letter from an internet bank. We provide accountability and a personal touch that algorithms cannot match.

Start Your Journey with RCG Mortgage Today

Saving for a down payment is the first step toward building generational wealth and securing your own piece of Hauppauge. You don’t have to navigate this financial journey alone. The team at RCG Mortgage is dedicated to transparency, accountability, and helping you find the loan that fits your lifestyle.

Don’t let another year pass you by. Let’s look at your numbers, explore your options, and get you on the path to homeownership in 2025.

Ready to see how much home you can afford?

Request a No-Obligation Quote Today

Contact Andrew Russell and the RCG Team:

Phone: (516) 246-6353

Email: teamrcg@rcgmortgage.com

Address: 490 Wheeler Rd Suite 252, Hauppauge, NY 11788