VA Loans in Hauppauge: Exclusive Programs for Military Families in Suffolk County For veterans, active-duty…

Preparing Your Credit Score for a Mortgage in 2026: A New Year’s Financial Resolution

Preparing Your Credit Score for a Mortgage in 2026: A New Year’s Financial Resolution

As the calendar turns and we embrace the fresh start of a New Year, many residents in Hauppauge and across Long Island are setting their sights on a major milestone: homeownership. If your goal is to buy a home in 2026, the work begins now. While saving for a down payment is often the first thing that comes to mind, your credit score is the silent gatekeeper that determines not only if you get approved, but how much that home will actually cost you over the life of the loan.

At RCG Mortgage, we believe that an educated borrower is a successful borrower. Led by Andrew Russell and our team of expert mortgage brokers in Hauppauge, NY, we specialize in guiding clients through the complexities of home financing with a “Nordstrom” level of service and a “Ford” assembly line efficiency. Whether you are a first-time homebuyer or looking to upgrade, treating your credit profile as a priority financial resolution this year is the smartest move you can make.

Why Your Credit Score is the Key to 2026 Homeownership

Your credit score is essentially a numerical representation of your financial reliability. In the mortgage world, it influences two critical factors: your eligibility for specific loan programs and the interest rate lenders are willing to offer you.

Even a fraction of a percentage point difference in your interest rate can translate to tens of thousands of dollars in savings (or costs) over a 30-year mortgage term. By starting your preparation in early 2025 for a 2026 purchase, you give yourself the runway needed to correct errors, pay down debt, and optimize your score to qualify for the best possible rates.

The “Tiered” Reality of Mortgage Rates

Lenders generally use price adjustments based on credit tiers. For example, a borrower with a 760 FICO score often unlocks the premier rates, whereas a borrower with a 660 score might pay a higher rate or require private mortgage insurance (PMI) for a longer period. Preparing now ensures you land in the highest tier possible.

Credit Score Requirements by Loan Type

One of the advantages of working with a broker like RCG Mortgage, rather than a big-box bank, is our access to a wide variety of lenders and loan products. Different loan types have different credit thresholds. Below is a general guide to what you should aim for as you prepare for 2026.

| Loan Program | Typical Minimum Score | Ideal Score for Best Terms | Who Is It For? |

|---|---|---|---|

| Conventional Loan | 620 | 760+ | Borrowers with stable income and average to excellent credit. |

| FHA Loan | 580 (3.5% down) 500 (10% down) |

640+ | First-time buyers or those with lower credit scores/higher debt ratios. |

| VA Loan | No official min (Lenders often look for 580-620) | 640+ | Veterans, active military, and eligible spouses (0% down payment). |

| Jumbo Loan | 700 | 740+ | Buyers purchasing high-value properties in Long Island exceeding conforming limits. |

| Non-QM Loans | Flexible (varies) | Varies | Self-employed borrowers, gig workers, or those with unique financial situations. |

Note: These figures are general industry standards. RCG Mortgage works with lenders who may offer exceptions or specific programs for unique situations.

5 Actionable Steps to Boost Your Score for 2026

Improving your credit score isn’t an overnight process; it is a marathon. Here are five strategic moves you can make this year to ensure you are mortgage-ready by 2026.

1. Check Your Report for Errors

According to the FTC, a significant number of consumers have errors on their credit reports that could affect their scores. Request your free credit reports from the major bureaus (Equifax, Experian, and TransUnion). Look for accounts you don’t recognize, late payments that were actually paid on time, or old debts that should have dropped off. Disputing these errors can result in a quick score boost.

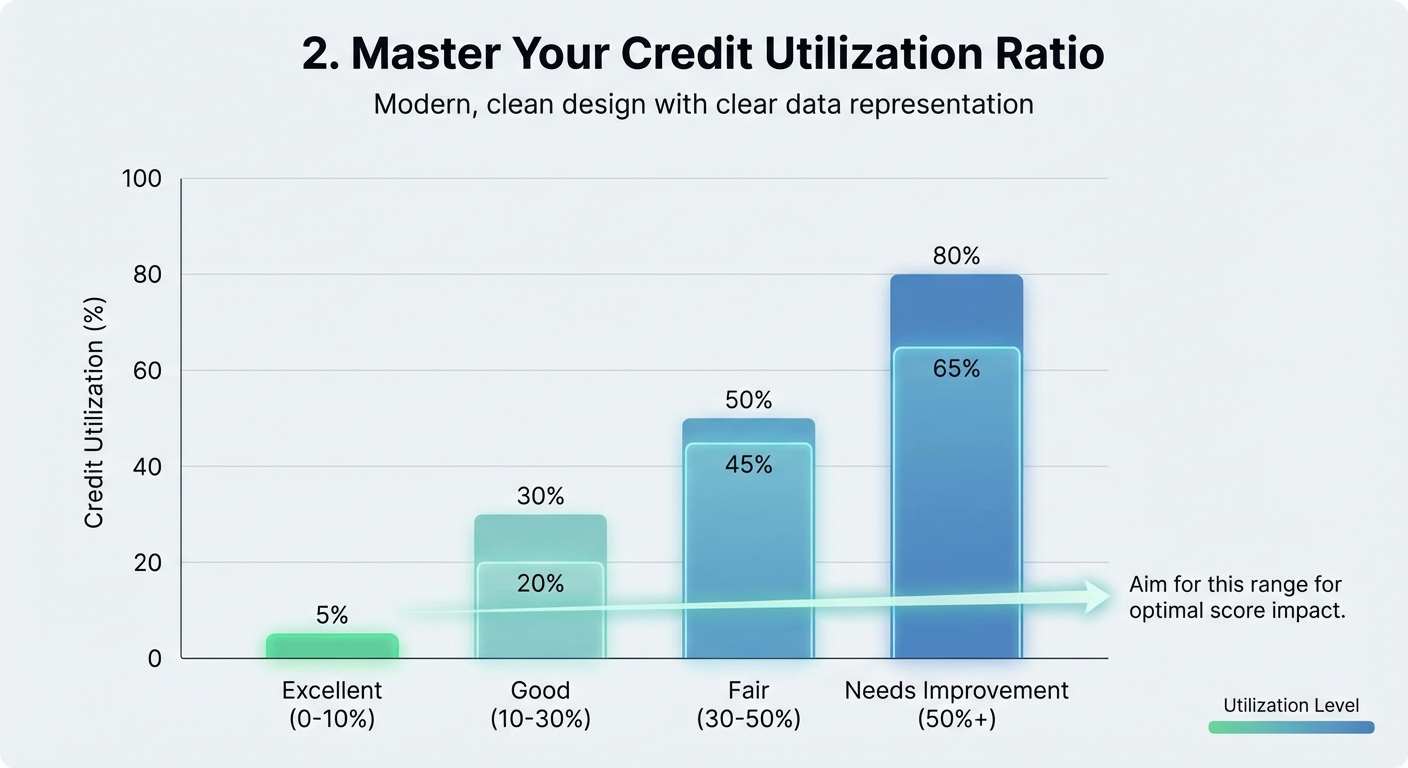

2. Master Your Credit Utilization Ratio

The Goal: Aim to keep your utilization below 30% on each card, and ideally below 10% for the highest score impact. If you have the cash flow, paying down revolving debt is the fastest way to increase your score.

The Goal: Aim to keep your utilization below 30% on each card, and ideally below 10% for the highest score impact. If you have the cash flow, paying down revolving debt is the fastest way to increase your score.

3. Don’t Close Old Credit Cards

When you pay off a credit card, your instinct might be to close the account. Don’t do it. The length of your credit history accounts for 15% of your FICO score. Closing an old account shortens your average credit age and reduces your total available credit limit, which can spike your utilization ratio. Keep the account open and use it for a small recurring subscription to keep it active.

4. Become an Authorized User

5. Avoid “Credit Shopping” Before the Mortgage

Every time you apply for a new credit card or auto loan, it triggers a “hard inquiry,” which can temporarily ding your score. In the 6 to 12 months leading up to your home purchase in 2026, avoid opening new lines of credit unless absolutely necessary. We want your credit profile to look stable and seasoned.

Why Choose a Local Hauppauge Mortgage Broker?

In the age of online clicking and automated approvals, you might wonder why you should partner with a local broker. The answer lies in customization and advocacy.

Big banks often have rigid “overlays”—stricter rules than what the loan guidelines actually require. If your credit score is on the borderline, a big bank might simply say “no.” As a specialized mortgage broker in Hauppauge, NY, RCG Mortgage operates differently:

- We Shop for You: We aren’t tied to one bank’s products. We scan dozens of lenders to find one that fits your specific credit profile.

- Local Expertise: We understand the Long Island market, from property taxes to condo requirements, ensuring no surprises derail your financing.

- Personalized Strategy: Andrew Russell and the team review your full financial picture. If you aren’t ready today, we help you map out exactly what you need to do to be ready in 2026.

Your 2025-2026 Credit Fitness Timeline

To help you stay on track with your New Year’s Resolution, follow this simple timeline:

- Q1 2025 (Jan-Mar): Pull credit reports, dispute errors, and set a budget to pay down high-interest credit card debt.

- Q2 2025 (Apr-Jun): Automate your bill payments to ensure zero late payments. Late payments are the biggest score killer.

- Q3 2025 (Jul-Sep): Check your progress. If your score has improved, consider asking for credit limit increases (without hard inquiries if possible) to further lower utilization.

- Q4 2025 (Oct-Dec): Avoid any new debt. Start gathering income documents (W2s, tax returns).

- Q1 2026 (The Home Stretch): Contact RCG Mortgage for a pre-approval. We will pull a mortgage credit report (which is different from consumer reports) and verify your buying power.

Frequently Asked Questions (FAQs)

1. What is the minimum credit score needed to buy a house in New York in 2026?

While requirements can vary by lender, generally, you need a minimum score of 580 for an FHA loan (requires 3.5% down) and 620 for a Conventional loan. However, to secure the most competitive interest rates, a score of 740 or higher is recommended.

2. Will checking my own credit score hurt it?

No. When you check your own credit (soft inquiry), it does not affect your score. Only “hard inquiries” initiated by a lender when you apply for credit will temporarily lower your score.

3. Can RCG Mortgage help if I have a low credit score?

Absolutely. Unlike big banks that may automatically decline applicants below a certain threshold, we have access to FHA, VA, and Non-QM loan products designed for borrowers with less-than-perfect credit. We can also advise you on how to improve your score to qualify.

4. How long does it take to improve my credit score?

It depends on the negative factors. Paying down high credit card balances can improve your score in as little as 30-45 days (after the issuer reports the new balance). However, recovering from missed payments or bankruptcies can take significantly longer. Starting your preparation a year in advance is the best strategy.

5. Should I pay off all my debts before applying for a mortgage?

Not necessarily. While less debt improves your Debt-to-Income (DTI) ratio, you also need cash reserves for your down payment and closing costs. It is often better to have a strategic balance between debt reduction and savings. Consult with a mortgage professional at RCG Mortgage to find the right balance for your situation.

Start Your Journey with RCG Mortgage Today

Buying a home is one of the biggest financial commitments you will make, but you don’t have to navigate the path alone. By making credit health your New Year’s resolution, you are investing in your future home and your financial well-being.

At RCG Mortgage, we are more than just loan originators; we are your partners in the American Dream. Whether you are in Hauppauge, elsewhere on Long Island, or anywhere in New York, we are ready to help you strategize for a successful purchase in 2026.

Ready to see where you stand? Don’t wait until 2026 to ask the questions. Let’s build your roadmap today.

Request a No-Obligation Quote

Or call us directly at (516) 246-6353