What is a Doctor Mortgage Loan? Medical and legal professionals face unique financial challenges. From…

Stop Throwing Money Away: Understanding Private Mortgage Insurance (PMI) and How to Get Rid of It

Stop Throwing Money Away: Understanding Private Mortgage Insurance (PMI) and How to Get Rid of It

Buying a home on Long Island is a significant achievement. Whether you are eyeing a colonial in Hauppauge or a condo in Smithtown, the journey to homeownership often comes with a vocabulary list that can feel overwhelming. One acronym that frequently causes confusion—and frustration—is PMI, or Private Mortgage Insurance.

At RCG Mortgage, we believe in transparency. We know that nobody likes seeing an extra fee on their monthly mortgage statement. However, for many first-time homebuyers in New York, PMI is the tool that makes buying a home possible sooner rather than later. The key is understanding what it is, why you have it, and most importantly, how to get rid of it once you have built enough equity.

If you are tired of “big bank fatigue” and want straight answers from a local expert, you are in the right place. Let’s break down everything you need to know about PMI and how to eventually eliminate it from your monthly budget.

What is Private Mortgage Insurance (PMI)?

Private Mortgage Insurance (PMI) is a type of insurance policy that protects the lender—not you—in case you stop making payments on your loan. It is typically required on conventional loans when you make a down payment of less than 20% of the home’s purchase price.

It is important to distinguish PMI from homeowners insurance. Homeowners insurance protects your physical property from damage (like fire or theft), whereas PMI protects the financial institution financing your home.

Why Do Lenders Require It?

From a lender’s perspective, a loan with a low down payment is riskier. If a borrower defaults and the home goes into foreclosure, the lender might not recoup the full loan amount if the market value has dipped. PMI mitigates this risk. Because of PMI, lenders are willing to offer mortgages to buyers with down payments as low as 3% or 5%, opening the door to homeownership for thousands of families in Hauppauge and across Long Island who haven’t saved a full 20%.

The Cost of PMI: What to Expect

One of the most common questions we get at RCG Mortgage is, “How much will PMI cost me?” There is no single answer, as PMI rates vary based on several factors:

- Your Credit Score: Borrowers with higher credit scores generally pay lower PMI rates.

- Loan-to-Value (LTV) Ratio: The lower your down payment, the higher your risk profile, and typically, the higher the premium.

- Loan Type: Fixed-rate mortgages often have slightly different PMI calculations than adjustable-rate mortgages (ARMs).

Typically, PMI costs between 0.5% and 1.5% of the original loan amount per year. This amount is broken down and added to your monthly mortgage payment.

PMI Cost Comparison Example

To give you a clearer picture, let’s look at a hypothetical scenario for a home purchase in Hauppauge, NY.

| Home Price | Down Payment (5%) | Loan Amount | Credit Score | Estimated Annual PMI | Estimated Monthly Cost |

|---|---|---|---|---|---|

| $600,000 | $30,000 | $570,000 | 760+ (Excellent) | $2,850 (0.5%) | $237.50 |

| $600,000 | $30,000 | $570,000 | 640-660 (Fair) | $8,550 (1.5%) | $712.50 |

Note: These figures are estimates for educational purposes. Actual PMI rates will vary based on current market conditions and specific insurer guidelines.

As you can see, your credit score plays a massive role in the cost of this insurance. This is why working with a broker like Andrew Russell and the team at RCG Mortgage is vital. We help you understand your credit profile and shop multiple lenders to find the most favorable terms.

PMI vs. MIP: Knowing the Difference

It is crucial not to confuse Private Mortgage Insurance (PMI) with Mortgage Insurance Premiums (MIP). While they serve a similar purpose, they apply to different loan types.

- PMI: Applies to Conventional Loans. It is provided by private insurance companies and can be removed once you reach a certain equity threshold.

- MIP: Applies to FHA Loans (Federal Housing Administration). FHA loans require both an upfront insurance premium and an annual premium paid monthly.

The Critical Distinction: With modern FHA loans, if you put down less than 10%, the MIP usually remains for the life of the loan. You cannot simply request to have it removed when you hit 20% equity. To get rid of FHA MIP, you typically have to refinance into a conventional loan once you have sufficient equity. This is a common strategy we use at RCG Mortgage to help clients lower their monthly payments.

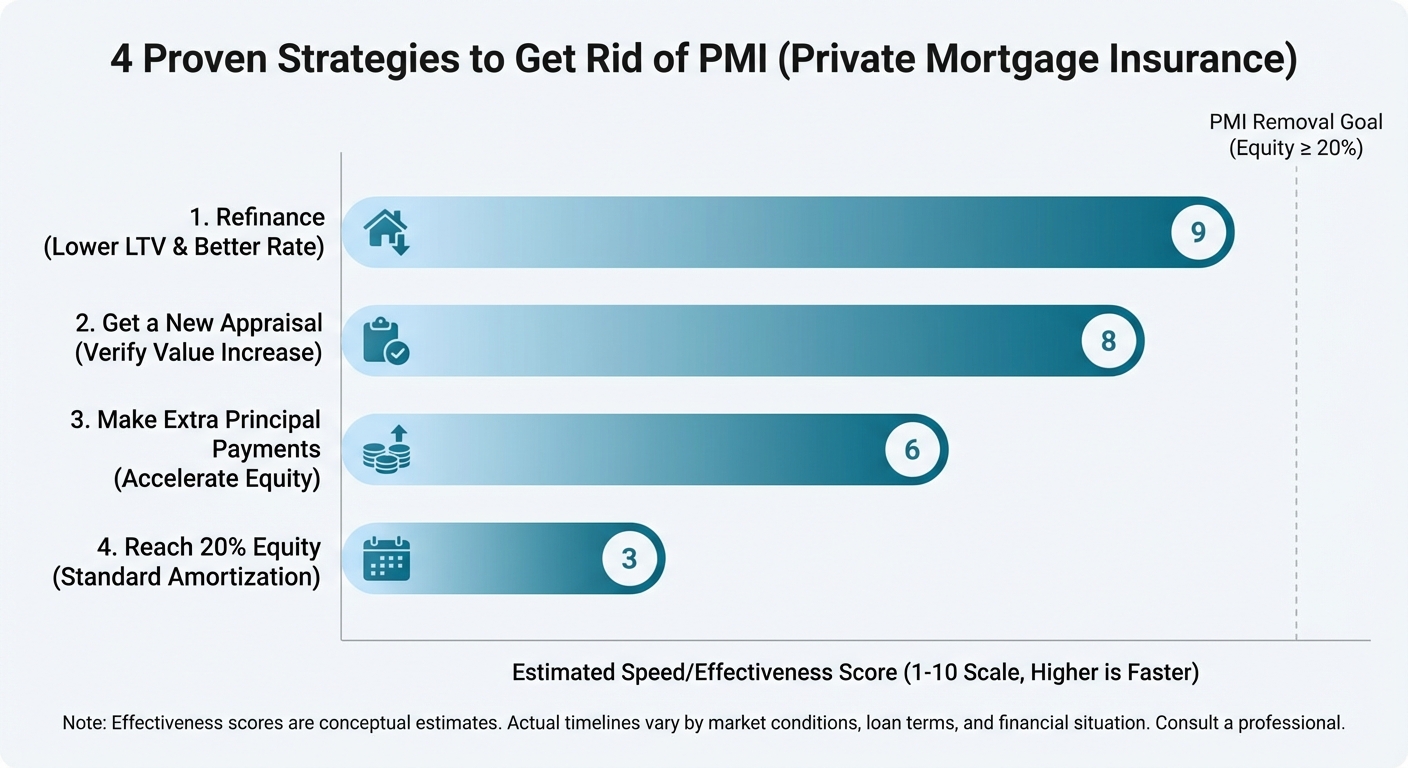

4 Proven Strategies to Get Rid of PMI

1. The Automatic Termination (The “Wait and See” Method)

Under the federal Homeowners Protection Act, your lender is required to automatically terminate your PMI once your loan balance reaches 78% of the original value of your home. This is based on your scheduled amortization payment plan.

While this requires zero effort on your part, it is often the slowest method. You simply continue making regular payments until the math works out in your favor.

2. Request Cancellation at 80% LTV

You do not have to wait for the automatic 78% drop-off. Once your mortgage balance drops to 80% of the home’s original appraised value, you have the right to request PMI cancellation in writing.

Requirements for this method:

- You must have a good payment history (no late payments in the last 12 months).

- You must be current on your payments.

- There generally cannot be any second mortgages or liens on the home.

- You may need to pay for an appraisal to prove the home’s value hasn’t declined.

3. Refinance Your Mortgage

This is where a local expert like RCG Mortgage shines. If interest rates have dropped since you bought your home, or if your home’s value has increased significantly, refinancing can be a game-changer.

By refinancing into a new conventional loan, the new lender will appraise your home at its current market value. If your new loan amount is 80% or less of this new value, you will not have to pay PMI on the new loan. This strategy can eliminate PMI and potentially lower your interest rate simultaneously.

4. Reappraisal Based on Market Appreciation or Renovations

You can contact your lender and ask if you can pay for a new appraisal to prove the higher value. If the new appraisal confirms you have 20% equity, they may agree to cancel the PMI early. Note: Lenders often require you to hold the loan for at least two years before using this method, though exceptions exist for substantial improvements.

Why Working with a Local Hauppauge Broker Matters

Navigating mortgage insurance, equity calculations, and refinancing options can be complex. While big banks treat you like a number, RCG Mortgage treats you like a neighbor. We are based right here at 490 Wheeler Rd, Hauppauge, NY.

We pride ourselves on offering a “Nordstrom” experience coupled with a “Ford” assembly line. This means you get high-end, personalized customer service combined with an efficient, streamlined process that gets you to the closing table faster.

When you work with Andrew Russell and the RCG team, we monitor your loan even after closing. We can help you identify exactly when you are eligible to drop your PMI or when a refinance makes financial sense. We understand the nuances of the Long Island market that national call centers simply miss.

Frequently Asked Questions (FAQs)

1. Is PMI tax-deductible?

In the past, PMI premiums were tax-deductible for certain income brackets. However, tax laws change frequently. As of the most recent updates, the deductibility of PMI has expired for many tax years, but it is sometimes retroactively reinstated by Congress. It is always best to consult with a certified tax professional regarding your specific situation.

2. Can I avoid PMI even with a low down payment?

Yes, there are a few ways. You might consider “Lender-Paid Mortgage Insurance” (LPMI), where the lender pays the insurance in exchange for a slightly higher interest rate. Alternatively, you can use a “piggyback loan” (an 80/10/10 structure), where you take a first mortgage for 80%, a second mortgage for 10%, and put 10% down. An RCG Mortgage broker can help you run the numbers to see if these options save you money.

3. What happens to my PMI if I refinance?

When you refinance, your old loan is paid off, and a new loan is created. If your new loan amount is 80% or less of your home’s current appraised value, your new mortgage will not include PMI. This is one of the most effective ways to remove mortgage insurance if your home value has increased.

4. Does PMI protect me if I lose my job?

No. This is a common misconception. PMI protects the lender against financial loss if you stop paying. It does not pay your mortgage for you if you lose your income. For that type of protection, you would need to look into mortgage protection insurance or life/disability insurance policies.

5. How do I start the process of removing PMI?

Start by checking your current loan balance against your home’s estimated value. If you think you are close to 20% equity, call your loan servicer (the company you send payments to) and ask for their specific requirements for PMI removal. Alternatively, contact RCG Mortgage for a consultation to see if refinancing is a better route to eliminate the cost and improve your loan terms.

Ready to Lower Your Monthly Payments?

Whether you are looking to buy your first home in Hauppauge without a massive down payment, or you are a current homeowner looking to ditch your PMI, RCG Mortgage is here to guide you. We offer tailored mortgage solutions to fit your unique needs.

Don’t let unnecessary fees drain your wallet. Let us review your current mortgage or help you structure a new purchase loan that fits your budget.

Request a No-Obligation Quote Today or give us a call at (516) 246-6353. Let’s make your homeownership journey smarter and more affordable.

Disclaimer: RCG Mortgage is a licensed mortgage broker. This content is for educational purposes only and does not constitute financial or legal advice. Loan programs, interest rates, and PMI guidelines are subject to change without notice. This site is not authorized by the New York State Department of Financial Services. No mortgage loan applications for properties located in the state of New York will be accepted through this site.

Related Posts