What is a Doctor Mortgage Loan? Medical and legal professionals face unique financial challenges. From…

Is 2026 the Right Time to Refinance Your Hauppauge Home? A Rate Analysis

Is 2026 the Right Time to Refinance Your Hauppauge Home? A Rate Analysis

For homeowners in Hauppauge, NY, the real estate market has been a whirlwind of fluctuating values and shifting interest rates over the last few years. As we look ahead, many Long Islanders are asking the same critical question: Is 2026 finally the year to refinance?

Whether you purchased your home during the peak rate environment or you are sitting on significant equity due to rising property values in Suffolk County, understanding the mortgage landscape is essential. At RCG Mortgage, we believe in empowering our neighbors with data-driven insights rather than sales pitches. Led by Andrew Russell, a recognized industry leader and multi-year NAMB Mortgage Broker of the Year, our team is here to break down the rate analysis for 2026 and help you determine if a refinance strategy aligns with your financial goals.

The Mortgage Landscape: What to Expect in 2026

Predicting mortgage rates is never an exact science, but analyzing economic trends provides a roadmap for smart financial planning. After a period of aggressive rate hikes aimed at curbing inflation, the market has shown signs of stabilization. For Hauppauge homeowners, 2026 is shaping up to be a pivotal year for potential relief and opportunity.

If you secured a mortgage between 2023 and 2025, you might be holding a loan with an interest rate higher than the historical average. Market analysts suggest that as inflation targets normalize, lenders may adjust rates downward to stimulate activity. This potential “softening” of rates makes 2026 a prime target for a Rate-and-Term Refinance.

Why Local Market Knowledge Matters

National headlines often miss the nuances of the Long Island real estate market. Hauppauge is unique. Property values here have remained resilient, meaning many homeowners have gained substantial equity even if they haven’t owned their home for long. This equity is the key to unlocking better financial terms.

Top Reasons to Refinance Your Hauppauge Home in 2026

Refinancing isn’t just about chasing a lower number; it is about restructuring your debt to fit your life. Here are the primary drivers we are seeing for local clients:

- lowering Monthly Payments: The most common motivation. Even a rate reduction of 0.75% to 1% can result in hundreds of dollars in monthly savings, freeing up cash flow for other household expenses.

- Cash-Out Refinancing for Renovations: Many Hauppauge homes were built decades ago and are ready for updates. Instead of using high-interest credit cards or personal loans, a cash-out refinance allows you to leverage your home’s equity to fund kitchens, bathrooms, or extensions at a much lower interest rate.

- Debt Consolidation: With consumer debt interest rates at all-time highs, rolling high-interest credit card debt into a tax-deductible mortgage payment can save thousands annually and improve your credit score.

- Removing Mortgage Insurance (PMI): If your home value has appreciated, you may now have enough equity (20% or more) to refinance into a conventional loan and eliminate costly Private Mortgage Insurance.

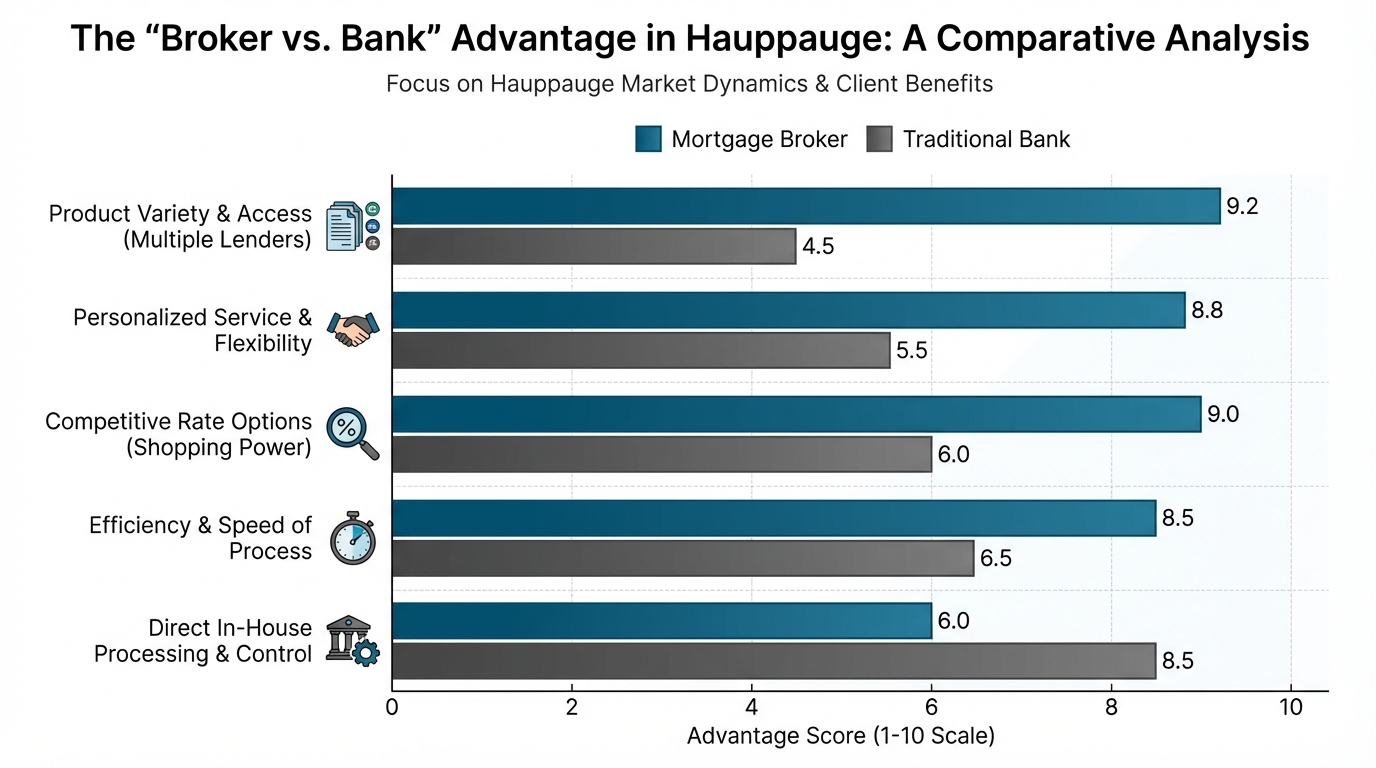

The “Broker vs. Bank” Advantage in Hauppauge

When considering a refinance, you generally have two options: walk into a big retail bank or partner with a local mortgage broker. In a complex rate environment like the one projected for 2026, the difference between these two paths can be substantial.

At RCG Mortgage, we often talk about “Big-Bank Fatigue.” This occurs when borrowers get stuck in a rigid system with limited options, slow turn times, and impersonal service. As a broker, Andrew Russell and the RCG team operate differently:

At RCG Mortgage, we often talk about “Big-Bank Fatigue.” This occurs when borrowers get stuck in a rigid system with limited options, slow turn times, and impersonal service. As a broker, Andrew Russell and the RCG team operate differently:

- Wholesale Rates: Brokers have access to wholesale interest rates that retail banks often cannot match. We shop dozens of lenders to find the specific product that fits your profile.

- Speed and Efficiency: We pride ourselves on providing a “Nordstrom experience coupled with a Ford assembly line.” This means high-touch customer service backed by an efficient process that closes loans faster.

- Tailored Solutions: Whether it is a standard Conventional loan, FHA Streamline, VA IRRRL, or a Non-QM loan for self-employed borrowers, we have access to the entire market inventory.

Rate Analysis Scenario: The Cost of Waiting vs. Acting

To illustrate the potential impact of a refinance in 2026, let’s look at a hypothetical scenario for a single-family home in Hauppauge. Please note that these figures are for educational purposes only and do not constitute a specific lending offer.

Scenario: A homeowner with a $500,000 mortgage balance taken out during a high-rate period.

| Loan Details | Current Loan (Hypothetical) | Potential 2026 Refinance |

|---|---|---|

| Interest Rate | 7.25% | 5.75% |

| Loan Term | 30-Year Fixed | 30-Year Fixed |

| Monthly Principal & Interest | $3,411 | $2,918 |

| Monthly Savings | — | $493 |

| Annual Savings | — | $5,916 |

*Disclaimer: Rates are subject to change based on market conditions, credit score, and loan-to-value ratio. This table is an example of mathematical savings based on interest rate reduction.

As you can see, a 1.5% reduction in rate significantly impacts the monthly budget. Over the life of the loan, the interest savings are massive. However, it is vital to calculate the “break-even point”—the time it takes for your monthly savings to cover the closing costs of the refinance. RCG Mortgage provides a detailed Total Cost Analysis to ensure the math makes sense for you.

Is Your Home Ready for an Appraisal?

For a successful refinance in Hauppauge, your home’s value is critical. The Loan-to-Value (LTV) ratio determines your eligibility and interest rate. Fortunately, Suffolk County real estate has maintained strong value. Before applying, we recommend:

- Checking Comparable Sales: Look at what homes similar to yours in Hauppauge have sold for recently.

- Completing Minor Repairs: Fix any obvious deferred maintenance that might negatively impact an appraisal.

- Reviewing Your Credit: A higher credit score can unlock significantly lower rates. RCG Mortgage can advise on rapid rescoring strategies if your score needs a slight boost.

The RCG Mortgage Process: Simple, Transparent, Local

Refinancing shouldn’t be a headache. Since 2017, RCG Mortgage has refined the process to respect your time and intelligence. We are located right here on Wheeler Road in Hauppauge, making us truly local experts.

When you contact us, here is what happens:

1. Discovery Call: We discuss your goals. Are you looking for cash out? Lower payments? Shorter term?

2. Soft Credit Pull: We can often review options without a hard hit to your credit initially.

3. Custom Options: We present multiple scenarios from different lenders.

4. Efficient Closing: Our team manages the paperwork, underwriting, and appraisal coordination to get you to the closing table smoothly.

Frequently Asked Questions (FAQs)

1. How do I know if 2026 is the right time to refinance?

2. What are the closing costs for a refinance in New York?

Closing costs in New York typically range between 2% and 4% of the loan amount. This includes bank fees, title insurance, and recording fees. However, RCG Mortgage often has options to structure “no-closing-cost” refinances where these costs are covered by a lender credit in exchange for a slightly different rate.

3. Can I refinance if I have bad credit?

Yes, options exist. While the lowest advertised rates require excellent credit (740+), FHA loans and Non-QM loans offer flexible refinancing solutions for borrowers with lower scores. As a broker, we have access to lenders who specialize in helping borrowers with less-than-perfect credit histories.

4. What is an FHA Streamline Refinance?

If you currently have an FHA loan, an FHA Streamline Refinance allows you to lower your rate with reduced documentation. Often, no appraisal is required, and income verification is minimal. It is designed to be fast and easy for homeowners who are current on their mortgage payments.

5. Why should I choose a Hauppauge Mortgage Broker over a big online lender?

Local accountability and expertise. An online call center doesn’t know the Hauppauge market, and you are often just a file number. At RCG Mortgage, we are your neighbors. We are accountable to our community, we know local appraisers, and we understand New York specific laws. Plus, our wholesale rates often beat the big box retail lenders.

Take the Next Step Toward Financial Freedom

Don’t leave your mortgage strategy to chance. If you are considering refinancing in 2026, get a head start by speaking with the team that has been voted Mortgage Broker of the Year four years running.

Andrew Russell and the RCG Mortgage team are ready to provide you with a transparent, honest assessment of your options. Let us help you lower your monthly payments and maximize your home investment.

Ready to see how much you can save?

Request Your No-Obligation Quote Today

Or call us directly at: (516) 246-6353

Brokers Do it Better… RCG Does it Best.

Related Posts