VA Loans in Hauppauge: Exclusive Programs for Military Families in Suffolk County For veterans, active-duty…

Self-Employed? How a Mortgage Broker in Hauppauge, NY Can Secure Your Loan

Self-Employed? How a Mortgage Broker in Hauppauge, NY Can Secure Your Loan

If you are one of the millions of Americans who have embraced the freedom of self-employment, you know the perks: being your own boss, setting your own hours, and the ability to write off significant business expenses to lower your tax bill. However, when it comes time to buy a home in Hauppauge, NY, or anywhere across Long Island, that last perk—tax write-offs—can suddenly feel like a penalty.

Many business owners, freelancers, and 1099 contractors face a harsh reality when they walk into a traditional big-box bank: denial. The bank looks at the “net income” on your tax returns, which you’ve legally minimized to save on taxes, and claims you can’t afford the mortgage.

Here is the good news: You do not have to choose between saving on taxes and buying your dream home.

As a specialized mortgage broker in Hauppauge, NY, RCG Mortgage understands that your tax returns do not always reflect your true cash flow or ability to repay a loan. Led by Andrew Russell, a recognized leader in the mortgage industry, our team helps self-employed borrowers navigate the complex lending landscape using innovative loan programs designed specifically for entrepreneurs.

The “Write-Off Paradox”: Why Banks Say No to Business Owners

To understand why working with a local broker is essential, you first need to understand why traditional lenders struggle with self-employed applicants. When you apply for a conventional mortgage (like those backed by Fannie Mae or Freddie Mac), the underwriter focuses heavily on your Debt-to-Income (DTI) ratio.

For a W-2 employee, income is simple: it’s the gross number on their paycheck. For a self-employed individual, traditional lenders look at the net income (the bottom line) on your tax returns. If you made $150,000 in revenue but wrote off $100,000 in expenses (mileage, home office, equipment, advertising), the bank views your income as only $50,000.

This creates a disconnect. You have the cash flow to pay the mortgage, but on paper, you don’t “qualify.” This is where RCG Mortgage steps in. We don’t just look at tax returns; we look at the full financial picture.

The Broker Advantage: “Nordstrom Experience, Ford Assembly Line”

At RCG Mortgage, our philosophy is unique. Andrew Russell founded the company to provide a “Nordstrom” level of customer service coupled with a “Ford” assembly line efficiency. This means you get a high-touch, personalized experience where we listen to your story, backed by a streamlined process that gets you to the closing table faster.

Unlike a retail bank officer who is restricted to a handful of rigid loan products, a mortgage broker acts as a liaison between you and dozens of wholesale lenders. We shop the market on your behalf to find lenders who specialize in working with business owners.

Why Choose a Local Hauppauge Broker?

- Local Market Knowledge: We understand the Hauppauge and Suffolk County real estate market. We know the local appraisers, real estate agents, and attorneys, which helps smooth out bumps in the road.

- Access to Non-QM Loans: We have access to “Non-Qualified Mortgage” (Non-QM) products that big banks simply do not offer.

- Speed and Efficiency: We know that in a competitive market, time is money. Our “assembly line” process ensures your file doesn’t sit on a desk gathering dust.

The Solution: Bank Statement Loans & Non-QM Options

If tax returns are the problem, what is the solution? For many of our self-employed clients in Hauppauge, the answer lies in Bank Statement Loans.

What is a Bank Statement Loan?

A Bank Statement Loan is a type of Non-QM loan that allows you to qualify using your bank deposits rather than your tax returns. Lenders will look at 12 to 24 months of your personal or business bank statements to determine your average monthly income.

How it works:

- Personal Bank Statements: Lenders typically count 100% of the deposits as income.

- Business Bank Statements: Lenders will usually count 50% to 90% of the deposits as income (factoring in a standard expense ratio) without needing to see your expense receipts.

This approach gives a much more accurate representation of your cash flow and purchasing power. It allows you to qualify for a loan amount that reflects your actual success, not just your taxable income.

Other Options for Self-Employed Borrowers

Beyond bank statement loans, RCG Mortgage offers other creative financing solutions:

- 1099 Only Loans: Ideal for independent contractors where we use your 1099 forms to verify income.

- Asset Depletion Loans: If you have significant liquid assets but low monthly income, we can use your assets to calculate a “monthly income” for qualification.

- DSCR Loans (for Investors): If you are buying an investment property, we can qualify you based on the property’s potential rental income (Debt Service Coverage Ratio) rather than your personal income.

Comparing Traditional Banks vs. RCG Mortgage

It can be helpful to visualize the difference between walking into a standard bank branch in Hauppauge versus scheduling a consultation with RCG Mortgage. See the comparison below:

| Feature | Traditional Retail Bank | RCG Mortgage (Broker) |

|---|---|---|

| Income Verification | Strictly Tax Returns (Net Income) | Tax Returns, Bank Statements, 1099s, or Assets |

| Loan Variety | Limited (Conventional, FHA, VA) | Extensive (Non-QM, Jumbo, Bank Statement, FHA, VA, Conventional) |

| Self-Employed Friendliness | Low (Penalizes tax write-offs) | High (Understands business cash flow) |

| Processing Speed | Slower (Bureaucratic red tape) | Fast (“Ford Assembly Line” efficiency) |

| Client Experience | Transactional | Relationship-based (“Nordstrom Experience”) |

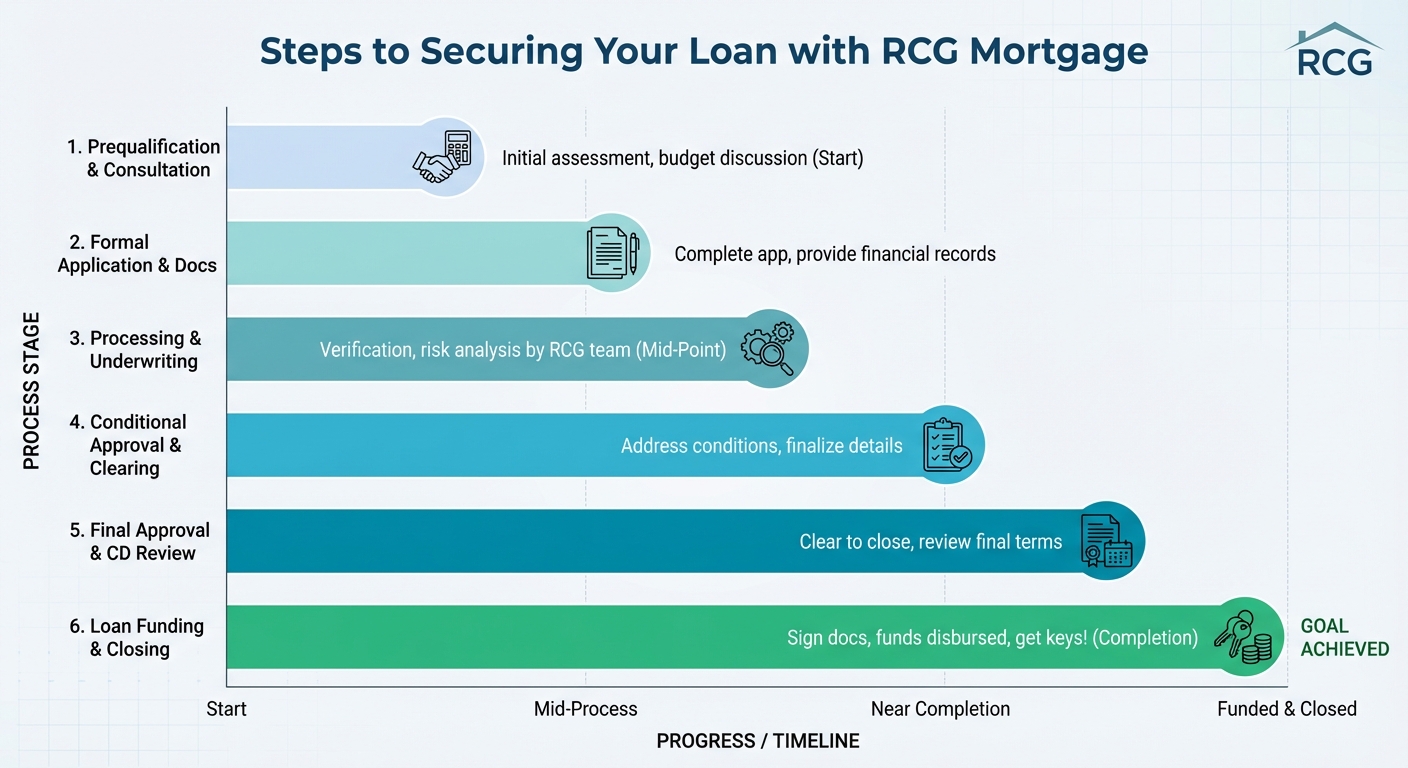

Steps to Securing Your Loan with RCG Mortgage

1. The Discovery Call

We start by listening. We discuss your business structure (Sole Proprietorship, LLC, S-Corp), your income streams, and your homeownership goals. This helps us identify whether a traditional loan or a Non-QM product is the best fit.

2. Gathering Documentation

- 12-24 months of business or personal bank statements.

- Current Profit & Loss (P&L) statement (sometimes required).

- Business license or proof of business existence for at least 2 years.

3. Pre-Approval

We issue a solid pre-approval letter. In the competitive Long Island market, a pre-approval from a reputable local broker like RCG carries weight with listing agents.

4. Shopping and Closing

Why Hauppauge Residents Trust Andrew Russell

RCG Mortgage isn’t just a faceless online entity; we are your neighbors. Located on Wheeler Road in Hauppauge, we have helped hundreds of local business owners achieve the American Dream.

Andrew Russell has been recognized as a top mortgage broker nationally, including features in the Scotsman Guide and Inc. 5000. But more importantly, our clients appreciate the honesty. We believe in educating you, not just selling to you. If now isn’t the right time to buy, we will tell you what you need to do to be ready in six months.

Frequently Asked Questions (FAQs)

1. Do Bank Statement loans have higher interest rates?

Generally, yes, the interest rates for Bank Statement loans are slightly higher than standard Conventional loans. This is because the lender is taking on a bit more risk by not using tax returns. However, the rate difference is often marginal compared to the benefit of actually securing the home. Additionally, you can often refinance into a conventional loan later if your tax profile changes.

2. How many years do I need to be self-employed to qualify?

Most lenders require you to be self-employed for at least two years. However, there are some programs available for borrowers who have been self-employed for at least one year, provided they have a strong history in the same line of work prior to starting their business.

3. Can I use a Bank Statement loan for an investment property?

Absolutely. In fact, self-employed investors often use these loans or DSCR (Debt Service Coverage Ratio) loans to expand their real estate portfolios without dealing with the complexity of personal tax returns for every purchase.

4. Is RCG Mortgage licensed to lend outside of Hauppauge, NY?

Yes! While our headquarters is in Hauppauge, NY, RCG Mortgage is licensed in multiple states including Florida, New Jersey, Connecticut, Pennsylvania, and many others. Whether you are buying a primary residence on Long Island or a vacation home in Florida, we can help.

5. Does a Bank Statement loan require a larger down payment?

Typically, yes. While conventional loans allow for as little as 3% or 5% down, Non-QM bank statement loans usually require a minimum down payment of 10% to 20%, depending on your credit score and the loan amount.

Take the Next Step Toward Homeownership

Being self-employed should be a badge of honor, not a barrier to buying a home. Don’t let a big bank’s rejection discourage you. At RCG Mortgage, we specialize in finding the “Yes” for business owners in Hauppauge and across New York.

Whether you are looking to buy a new home, refinance your current mortgage, or invest in real estate, Andrew Russell and his team are ready to provide you with a world-class experience.

Ready to explore your options?

Contact RCG Mortgage today for a no-obligation consultation.

- Phone: (516) 246-6353

- Email: andrew@rcgmortgage.com

- Visit Us: 490 Wheeler Rd Suite 252, Hauppauge, NY 11788

- Website: www.rcgmortgage.com