Rent vs. Buy in Hauppauge: A 2026 Financial Breakdown The age-old debate of renting versus…

VA Loans in Hauppauge: Exclusive Programs for Military Families in Suffolk County

VA Loans in Hauppauge: Exclusive Programs for Military Families in Suffolk County

For veterans, active-duty service members, and surviving spouses living in or moving to Long Island, the journey to homeownership is paved with one of the most powerful financial tools available: the VA Loan. At RCG Mortgage, located right here in Hauppauge, NY, we believe that those who served our country deserve the highest level of service when securing their piece of the American Dream.

Navigating the real estate market in Suffolk County can be complex. With fluctuating interest rates and competitive housing prices, having a dedicated local mortgage broker by your side makes all the difference. Led by Andrew Russell, a multi-year award-winning Mortgage Broker of the Year, the team at RCG Mortgage is committed to providing a “Nordstrom” customer service experience coupled with “Ford” assembly line efficiency. This guide will explore everything you need to know about VA loans in Hauppauge and how our team can help you maximize your military benefits.

What is a VA Loan?

A VA loan is a mortgage loan issued by private lenders—like RCG Mortgage—and backed by the U.S. Department of Veterans Affairs (VA). Created in 1944 as part of the GI Bill, this program was designed to help returning service members purchase homes without needing a down payment or excellent credit.

While the government guarantees a portion of the loan, they do not originate it. This is where working with a specialized Hauppauge mortgage broker becomes crucial. We shop multiple lenders to find you the most competitive rates and terms that fit your specific financial situation.

Why Choose a VA Loan in Suffolk County?

Long Island, specifically Suffolk County, is known for its beautiful neighborhoods, top-rated school districts, and proximity to New York City. However, it is also known for higher-than-average property values. This is where the specific benefits of a VA loan shine for local buyers.

1. 0% Down Payment

The most significant barrier to entry for many homebuyers in Hauppauge, NY (11788) is the down payment. On a median-priced home in Suffolk County, a traditional 20% down payment can be upwards of $100,000. With a VA loan, qualified borrowers can purchase a home with $0 down. This allows you to keep your savings for renovations, furnishing your new home, or emergency funds.

2. No Private Mortgage Insurance (PMI)

With Conventional and FHA loans, if you put down less than 20%, you are typically required to pay Private Mortgage Insurance (PMI). This insurance protects the lender, not you, and can add hundreds of dollars to your monthly mortgage payment. VA loans do not require PMI, regardless of your down payment amount. This monthly saving significantly increases your purchasing power in the Long Island market.

3. Competitive Interest Rates

Because the federal government backs these loans, lenders assume less risk. Consequently, VA loans often come with lower interest rates compared to conventional loans. At RCG Mortgage, we leverage our network of lenders to ensure you are getting the absolute best rate available.

4. Flexible Credit Requirements

Life in the military can sometimes make maintaining a perfect credit score difficult due to frequent moves and deployments. The VA loan program is more forgiving regarding credit scores than conventional financing. While many big banks have strict cut-offs, as a flexible mortgage broker, RCG Mortgage can often work with borrowers who have lower credit scores or previous financial hurdles.

The “Broker vs. Bank” Advantage for Veterans

When shopping for a VA loan, you have two main options: a direct lender (like a big bank) or a mortgage broker. Here is why choosing a local broker like RCG Mortgage in Hauppauge offers a distinct advantage:

- More Options: A bank can only offer their specific products. If you don’t fit their box, you are denied. RCG Mortgage works with dozens of wholesale lenders. We shop the market for you to find the lender that views your application most favorably.

- Local Expertise: We understand the nuances of Suffolk County real estate, from property taxes to condo approvals. A call center representative in another state likely won’t understand the specifics of buying a home in Hauppauge or Smithtown.

- Speed and Efficiency: In a competitive market, closing speed matters. Our “Ford assembly line” process ensures your loan moves through underwriting quickly, helping you compete with cash buyers.

- Personalized Service: You aren’t just a loan number to us. You can visit our office at 490 Wheeler Rd, Suite 252, Hauppauge, NY, or call Andrew Russell directly. We are accountable to you.

VA Loan Eligibility Requirements

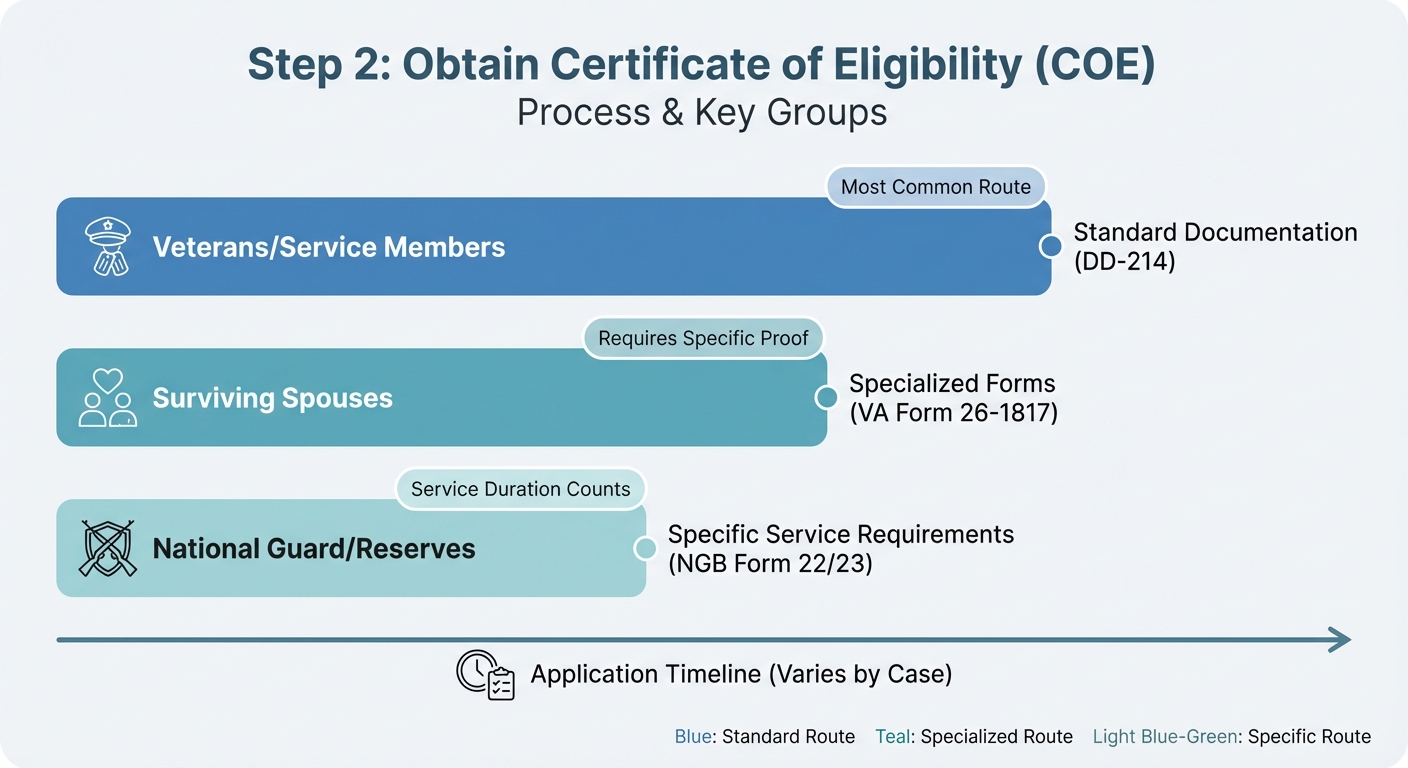

While the VA loan is one of the most accessible loan programs, there are specific service requirements to obtain a Certificate of Eligibility (COE). Generally, you may be eligible if you meet one of the following criteria:

- You have served 90 consecutive days of active service during wartime.

- You have served 181 days of active service during peacetime.

- You have more than 6 years of service in the National Guard or Reserves.

- You are the spouse of a service member who died in the line of duty or as a result of a service-related disability.

Note: Even if you have a discharge other than honorable, you may still qualify. Contact RCG Mortgage, and we can help you pull your COE to verify your status.

Comparing Mortgage Options: VA vs. FHA vs. Conventional

To help you understand the value of a VA loan, look at this comparison of standard loan programs available in New York:

| Feature | VA Loan | FHA Loan | Conventional Loan |

|---|---|---|---|

| Down Payment | 0% | 3.5% | 3% – 20% |

| Mortgage Insurance (PMI) | None | Required (Upfront + Monthly) | Required if under 20% down |

| Credit Score | Flexible (often 580+) | Flexible (580+) | Stricter (Typically 620+) |

| Closing Costs | Limited by VA rules | Standard | Standard |

| Occupancy | Primary Residence Only | Primary Residence Only | Primary, Second Home, or Investment |

The VA Loan Process with RCG Mortgage

We strive to make the mortgage process simple and transparent. Here is what the path to homeownership looks like for military families in Hauppauge:

Step 1: Prequalification

Before you start looking at homes, you need to know your budget. Contact us to get pre-qualified. We will review your income, credit, and military service history to determine how much you can afford. This generates a Prequalification Letter, which proves to sellers that you are a serious buyer.

Step 2: Obtain Certificate of Eligibility (COE)

Step 3: House Hunting

Armed with your pre-approval, you can shop for homes in Hauppauge, Smithtown, Brentwood, or anywhere in Suffolk County. We recommend working with a real estate agent who understands VA financing.

Step 4: VA Appraisal

Step 5: Underwriting and Closing

Our team works diligently to clear any conditions from the underwriter. Once approved, you’ll sign the final paperwork, and you’ll be handed the keys to your new home.

Exclusive Benefits: The VA Funding Fee Exemption

Most VA borrowers pay a one-time funding fee that helps sustain the program. This fee can be rolled into the loan amount. However, veterans with a service-connected disability rating of 10% or higher are exempt from paying this fee.

This is a massive saving—often amounting to thousands of dollars. If you have a disability rating, please let the team at RCG Mortgage know immediately so we can structure your loan correctly to save you money.

Frequently Asked Questions (FAQs)

1. Can I use a VA loan more than once?

Yes! The VA loan benefit is not a one-time use program. Once you sell your home and pay off the original VA loan, your full entitlement is restored. In some cases, you can even have two VA loans active simultaneously (bonus entitlement) if you are relocating for orders. Contact us to calculate your remaining entitlement.

2. Are there limits on how much I can borrow in Suffolk County?

Thanks to the Blue Water Navy Vietnam Veterans Act of 2019, loan limits have been eliminated for borrowers with full entitlement. This means you can buy a home in Hauppauge at a higher price point with zero down, provided you qualify based on income and credit.

3. Can I use a VA loan to buy an investment property?

VA loans are designed strictly for primary residences. You must intend to live in the home. However, you can purchase a multi-unit property (up to 4 units) as long as you occupy one of the units as your primary home. This is a great strategy for veterans to build wealth through rental income.

4. What are the closing costs for a VA loan?

While there is no down payment, there are still closing costs (title fees, recording fees, taxes, etc.). The VA limits what fees veterans can be charged. Additionally, sellers are allowed to pay up to 4% of the purchase price in concessions to cover your closing costs, potentially allowing you to close with very little money out of pocket.

5. How long does the process take?

There is a myth that VA loans take forever to close. This is simply not true when working with an experienced broker. At RCG Mortgage, we pride ourselves on speed. We can often close VA loans in 30 days or less, comparable to conventional loans.

Ready to Use Your Military Benefits?

At RCG Mortgage, we are honored to serve those who have served us. Whether you are a first-time homebuyer in Hauppauge or looking to refinance an existing loan, Andrew Russell and his team are ready to guide you with transparency and expertise.

Don’t navigate the mortgage maze alone. Work with a local expert who is invested in your success.

Ready for a no-obligation quote?

Get Started with RCG Mortgage Today

Or call us directly at (516) 246-6353