Understanding How a Home Equity Line of Credit Works If you are a homeowner in…

The Essential Guide to Hauppauge, NY Property Taxes and How They Affect Your Mortgage Payment

Buying a home on Long Island is a dream for many, and Hauppauge, NY, offers a fantastic blend of suburban charm, excellent schools, and community amenities. However, anyone who has browsed real estate listings in Suffolk County knows that the sticker price of the home is only half the story. The other half? Property taxes.

For first-time homebuyers and seasoned investors alike, understanding how local taxes influence your buying power is critical. At RCG Mortgage, we believe in transparency and education. We want you to walk into your closing with your eyes wide open, confident that your monthly budget is secure.

Below is your essential guide to navigating property taxes in Hauppauge and understanding exactly how they impact your bottom line.

The Reality of Long Island Property Taxes

It is no secret that Long Island has some of the highest property taxes in the nation. In Hauppauge, these taxes fund top-tier school districts, police, fire departments, and public works. While these services keep property values high and neighborhoods desirable, they also mean that two homes with the exact same listing price can have vastly different monthly payments based solely on their tax bills.

When you apply for a loan, your debt-to-income (DTI) ratio is calculated using your total monthly housing obligation, not just the loan repayment. If taxes are higher than expected, it reduces the loan amount you qualify for.

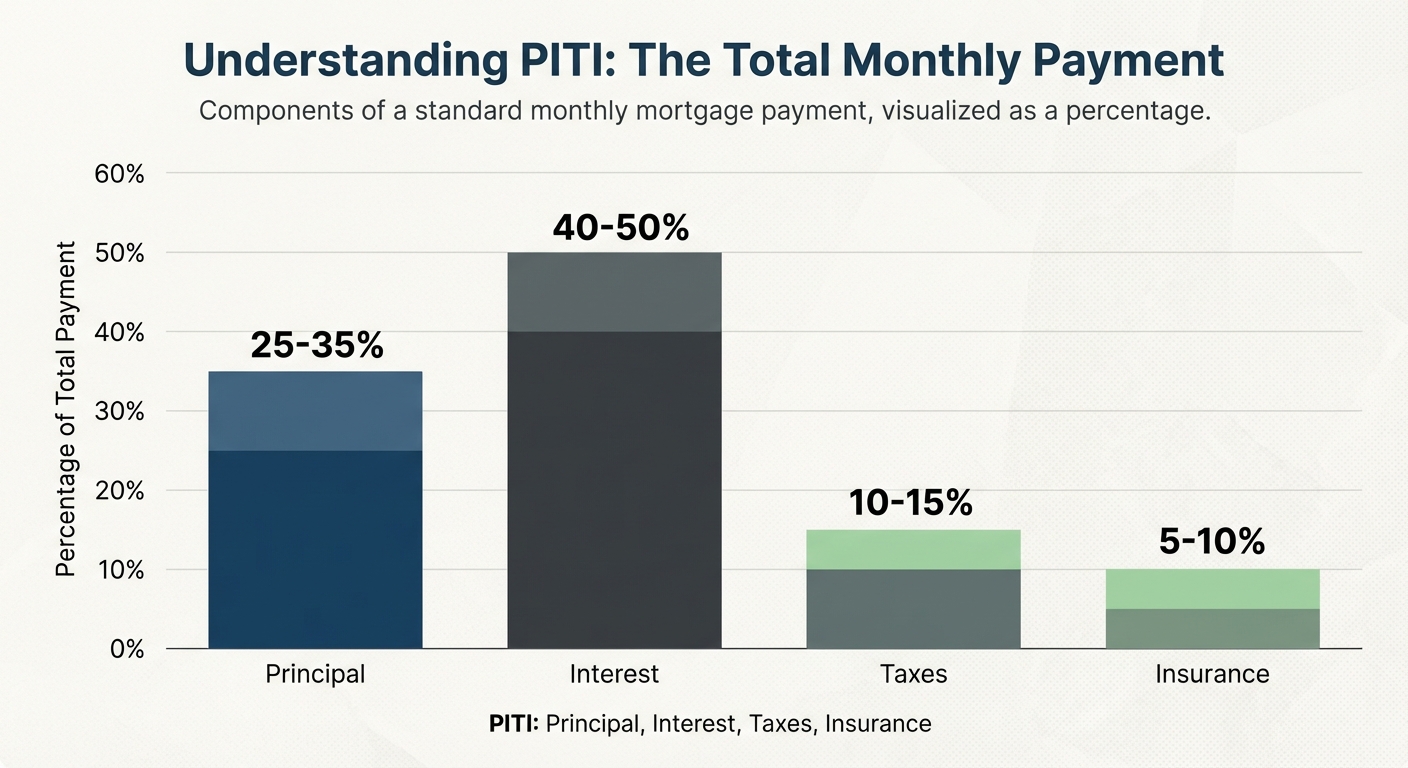

Understanding PITI: The Total Monthly Payment

To understand the impact of taxes, you need to understand the anatomy of a mortgage payment. In the industry, we call this PITI:

- Principal: The money that pays down the loan balance.

- Interest: The cost of borrowing the money.

- Taxes: Property taxes paid to the local government.

- Insurance: Homeowners insurance to protect the property.

In Hauppauge, the “T” in PITI can sometimes rival the “P” and “I” combined. This is why using a generic online calculator often leads to disappointment. If the calculator defaults to a national average tax rate (often around 1.1%), but the actual tax rate on a Long Island home is closer to 2.5% or 3%, your estimated payment could be off by hundreds, or even thousands, of dollars.

Comparison: How Taxes Change Your Payment

Let’s look at a hypothetical scenario for a home purchase in Hauppauge to see how tax variances affect your wallet.

| Scenario | Home Price | Annual Property Taxes | Monthly Tax Cost | Impact on Payment |

|---|---|---|---|---|

| Home A (Lower Tax) | $650,000 | $12,000 | $1,000 | Base Baseline |

| Home B (Average Tax) | $650,000 | $18,000 | $1,500 | +$500 / month |

| Home C (High Tax) | $650,000 | $24,000 | $2,000 | +$1,000 / month |

Note: This table is for illustrative purposes only and does not include principal, interest, or insurance.

As you can see, Home A and Home C cost the same to buy, but Home C costs $1,000 more per month just to live in. Over a 30-year term, that is a massive difference in financial obligation.

Why You Need a Local Mortgage Broker

This is where the distinction between a big-box bank and a local expert becomes vital. A large, national mortgage lender or an automated online system may not accurately estimate Hauppauge tax rates during your pre-approval process. They might qualify you for a loan amount based on incorrect tax data, leading to a denial later in the underwriting process or, worse, a monthly payment you struggle to afford.

By partnering with a trusted Mortgage Broker like Andrew Russell and the team at RCG Mortgage, you get local expertise. We know the Hauppauge market. We check the specific tax records for the properties you are interested in to ensure your pre-approval is rock solid.

A Mortgage Broker works for you, not the bank. We have the flexibility to shop multiple lenders to find interest rates that might help offset higher property tax costs, ensuring your total monthly payment stays within your budget.

Strategies to Manage and Lower Property Taxes

Just because taxes are high doesn’t mean you are powerless. Here are a few actionable tips for Hauppauge homeowners:

- File for the STAR Exemption: The New York State School Tax Relief (STAR) program offers property tax relief to eligible New York State homeowners. Ensure you register for this immediately upon closing.

- Grieve Your Taxes: In Suffolk County, you have the right to challenge your tax assessment if you believe it is higher than the market value of your home. Many homeowners successfully lower their bills by filing a grievance annually.

- Check for Village Taxes: Some areas in Hauppauge may fall within incorporated villages, which can have separate tax bills. We help you identify these hidden costs upfront.

The Role of Escrow Accounts

For most borrowers, you won’t be writing a separate check to the receiver of taxes twice a year. Instead, your mortgage lender will set up an escrow account. You pay 1/12th of your annual tax bill every month as part of your mortgage payment. The lender holds this money and pays the tax bill on your behalf when it is due.

At RCG Mortgage, we help you understand your closing disclosure so you know exactly how much is being collected for escrow reserves, ensuring you aren’t surprised by cash-to-close requirements.

Navigate the Market with Confidence

Don’t let property taxes scare you away from your dream home in Hauppauge. With the right planning and the right team, you can navigate the market with confidence. Whether you are a first-time buyer or looking to refinance, understanding the numbers is the key to success.

At RCG Mortgage, we pride ourselves on providing a “Nordstrom” experience with “Ford” efficiency. We are here to guide you through every line item of your mortgage.

Ready to Get Started?

Stop guessing your monthly payments and start planning your future. Contact Andrew Russell and the RCG Mortgage team today for a no-obligation quote and a true analysis of what you can afford in Hauppauge.

Contact RCG Mortgage Today or call us at (516) 246-6353.

Related Posts