If the last few years in real estate have taught us anything, it is that…

Your Guide to Physician and Professional-Program Mortgages in Hauppauge, NY

What is a Doctor Mortgage Loan?

Medical and legal professionals face unique financial challenges. From high student loan debt to delayed entry into the workforce, traditional lending criteria can sometimes hold you back from buying your dream home. This is where a doctor mortgage loan comes into play. Also known as Physician Professional-Program Mortgages, these specialized loans are designed to accommodate the financial realities of doctors, dentists, and lawyers.

At RCG Mortgage in Hauppauge, NY, we understand that your earning potential is high, even if your current debt-to-income ratio is skewed by educational loans. Unlike a standard conventional fixed-rate mortgage, a doctor loan often requires zero to very little down payment and does not mandate private mortgage insurance (PMI). Furthermore, student debt is frequently calculated differently, making it easier to qualify.

- Doctor Loans: Tailored for MDs, DOs, and sometimes residents or fellows looking to buy a home before their attending salary kicks in.

- Dentist Loans: Designed for DMDs and DDSs who might also be balancing practice acquisition costs alongside homeownership goals.

- Lawyer Loans: Specialized programs for attorneys that recognize the trajectory of a legal career and high earning potential.

If you have already been quoted a rate, we highly recommend getting a second opinion. We are experts at providing second opinions on physician and professional mortgage programs to ensure you are getting the most competitive terms available in Long Island.

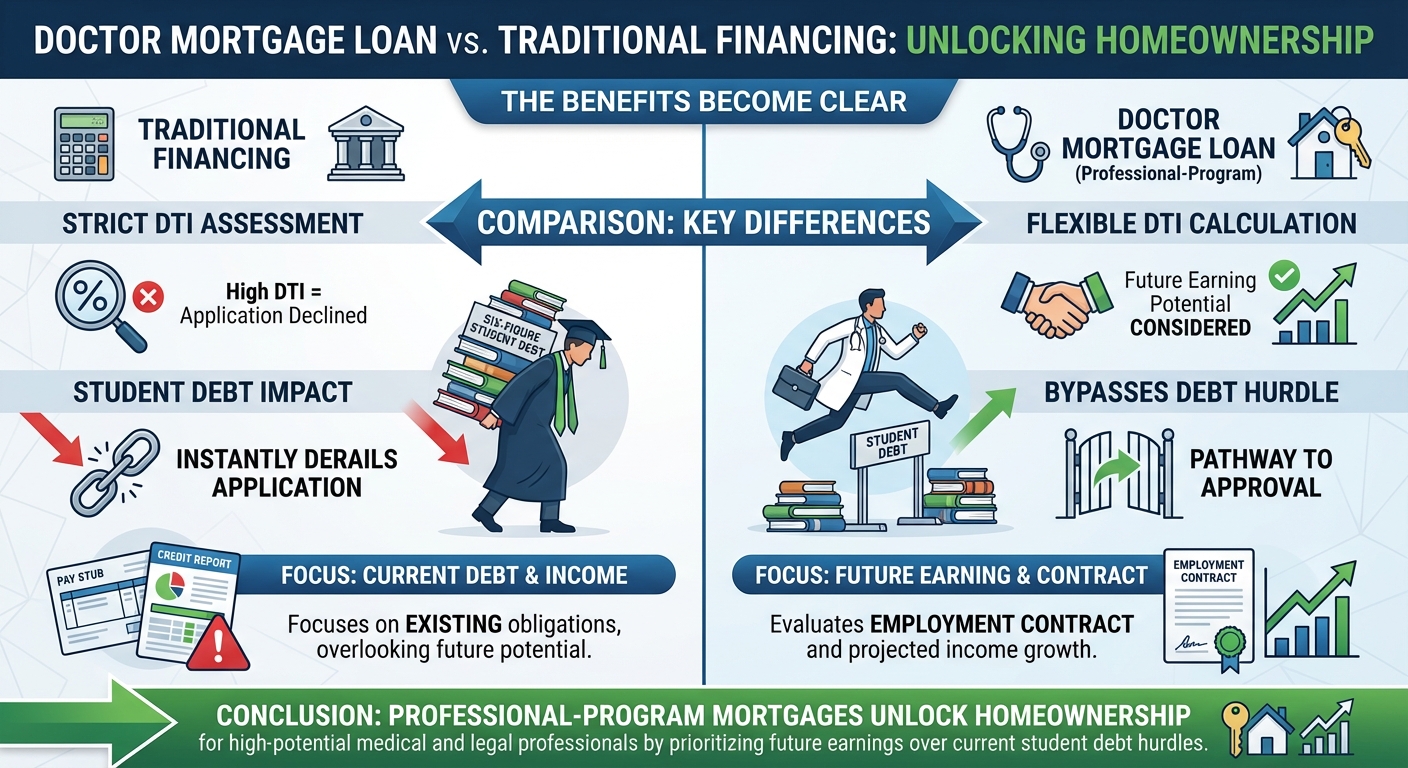

Comparing Professional Loans to Traditional Financing

When comparing a doctor mortgage loan to traditional financing options, the benefits quickly become clear. Standard loans typically require a strict assessment of your debt-to-income ratio. For a recent medical school graduate or a newly minted attorney in Hauppauge, NY, six-figure student debt can instantly derail a traditional mortgage application.

Professional-program mortgages bypass this hurdle. Lenders look at your future earning potential and your employment contract rather than just your past financial history. Additionally, many professionals seek luxury properties that exceed standard lending limits. In these cases, a physician loan can be a fantastic alternative to a traditional jumbo mortgage, offering high loan limits without the standard 20 percent down payment requirement.

Whether you are a dentist opening a new practice in Suffolk County or a resident transitioning to an attending role, securing the right financing is crucial. RCG Mortgage is dedicated to helping you navigate these specialized programs. Remember, not all lenders structure these loans the same way. Reaching out to us for a second opinion on your physician loan could save you thousands of dollars over the life of your mortgage.

| Feature | Traditional Mortgage | Doctor / Professional Loan |

|---|---|---|

| Down Payment | Typically 3% to 20% | 0% to 10% (often 0%) |

| Private Mortgage Insurance (PMI) | Required if under 20% down | Usually waived entirely |

| Student Loan Debt Calculation | Fully counted in DTI ratio | Often excluded or reduced if deferred |

| Proof of Income | Past pay stubs and tax returns | Employment contract often sufficient |

| Loan Limits | Conforming limits apply | High limits, similar to jumbo loans |

How to Qualify for a Doctor Mortgage Loan in Hauppauge

Qualifying for a professional or doctor mortgage loan in Hauppauge, NY, is a streamlined process when you work with an experienced mortgage broker. The first step is gathering your documentation. While you might not need years of tax returns, you will need to provide a copy of your employment contract, your medical or legal license, and details regarding your student loans.

Here are a few tips to ensure a smooth application process:

- Check your credit score: Even with flexible DTI requirements, a strong credit history is essential for securing the best interest rates.

- Have your contract ready: Lenders will want to see your start date and guaranteed base salary.

- Seek expert guidance: Mortgage guidelines vary wildly. Andrew Russell and the team at RCG Mortgage know exactly which lenders offer the most favorable terms for your specific profession.

We pride ourselves on offering comprehensive coverage of doctor, dentist, and lawyer loans. If you are actively shopping for a home in Long Island or simply planning for the future, let us review your scenario. We are experts at providing second opinions on physician and professional mortgage programs, ensuring you never leave money on the table.

Q1: Can I get a doctor mortgage loan before I start my new job?

Yes, many physician loan programs allow you to close on a home up to 90 days before your employment contract officially begins.

Q2: Are professional mortgage programs only for medical doctors?

No, these specialized loans are also available for dentists, veterinarians, and lawyers, depending on the specific lender guidelines.

Q3: Do doctor loans require private mortgage insurance (PMI)?

One of the biggest advantages of a physician professional-program mortgage is that PMI is typically not required, even with a zero percent down payment.

Q4: Can I use a doctor loan to refinance my current home?

Yes, many lenders offer refinancing options under their professional mortgage programs, which can be useful if you want to remove PMI from an existing loan.

Q5: Why should I get a second opinion on my professional mortgage quote?

Rates and terms for doctor loans vary significantly between lenders. RCG Mortgage specializes in providing second opinions to ensure you receive the most competitive offer available.

Ready to Secure Your Professional Mortgage?

Contact Andrew Russell at RCG Mortgage in Hauppauge, NY today for a free consultation or a second opinion on your loan estimate.

Call us at 1-516-246-6353 or email andrew@rcgmortgage.com.

Related Posts