VA Loans in Hauppauge: Exclusive Programs for Military Families in Suffolk County For veterans, active-duty…

Avoiding Common Mistakes First-Time Homebuyers Make: Advice from a Hauppauge Mortgage Expert

Avoiding Common Mistakes First-Time Homebuyers Make: Advice from a Hauppauge Mortgage Expert

Buying your first home is one of the most significant milestones in life. It represents the realization of the American Dream, a step toward financial stability, and a place to call your own. However, for many in Hauppauge, NY, and across Long Island, the path to homeownership can feel like navigating a maze without a map. The real estate market here is competitive, fast-paced, and financially complex.

At RCG Mortgage, we have guided thousands of aspiring homeowners through this process. As a top-rated local mortgage broker, we have seen it all—from the triumphs of closing day to the frustrations of avoidable errors. Andrew Russell, our founder and a multi-year NAMB Mortgage Broker of the Year, often says, “It is my greatest honor to help homebuyers achieve the American Dream of homeownership.” To help you achieve that dream without the nightmares, we have compiled a comprehensive guide on the most common mistakes first-time homebuyers make and how to avoid them.

Mistake #1: Confusing Pre-Qualification with Pre-Approval

One of the earliest stumbling blocks for first-time buyers is misunderstanding the difference between being “pre-qualified” and “pre-approved.” While they sound similar, they carry very different weights in the eyes of a seller, especially in the competitive Hauppauge real estate market.

- Pre-Qualification: This is generally a self-reported estimate of what you might be able to afford. You provide a lender with basic details about your income and debts, and they give you a ballpark figure. It is useful for budgeting, but it does not guarantee financing.

- Pre-Approval: This is a verified commitment from a lender. At RCG Mortgage, we review your credit report, pay stubs, W-2s, and bank statements to determine exactly how much we can lend you.

In a market like Long Island, where inventory is tight and bidding wars are common, a pre-qualification letter often isn’t enough. Sellers want assurance that the deal will close. A pre-approval letter from a reputable local expert like RCG Mortgage signals to real estate agents and sellers that you are a serious buyer with verified financing. As Andrew Russell notes in his advice to clients, getting pre-approved is the critical first step to “shopping with confidence.”

Mistake #2: Fixating Solely on the Interest Rate

We understand the urge to hunt for the absolute lowest number when looking at interest rates. However, fixating only on the rate is a classic rookie mistake. A mortgage is a complex financial product, and the interest rate is just one component of the total cost.

Many “big box” banks or online lenders may advertise rock-bottom rates, but those rates often come with hidden caveats, such as:

- High Discount Points: You might have to pay thousands of dollars upfront to “buy down” the rate.

- Higher Closing Costs: Excessive origination fees can offset the savings from a slightly lower rate.

- Inflexible Terms: The loan might have strict rules regarding refinancing or early payoff.

At RCG Mortgage, we believe in transparency. We look at the APR (Annual Percentage Rate), which gives you a broader picture of the loan’s cost, including fees. We also consider your long-term goals. Are you planning to stay in the home for 30 years, or is this a starter home for the next five? Sometimes, a slightly higher rate with lower upfront costs is the smarter financial move. Our “Nordstrom experience coupled with a Ford assembly line” approach means we tailor the product to your life, not just a number on a screen.

Mistake #3: Underestimating the “Hidden” Costs of Homeownership

Many first-time buyers in Hauppauge calculate their budget based solely on the principal and interest payment. This calculation is dangerous because it ignores the “TI” in “PITI” (Principal, Interest, Taxes, and Insurance).

Property Taxes and Insurance

Long Island is known for having higher property taxes compared to other regions. It is crucial to check the specific tax bill of the homes you are viewing. Additionally, homeowners insurance is a mandatory requirement for securing a mortgage. These costs are typically held in an escrow account and added to your monthly payment.

Closing Costs

Closing costs in New York can be substantial. These include title insurance, recording fees, attorney fees, and prepaid items. A general rule of thumb is to budget between 3% and 6% of the purchase price for closing costs. Failing to budget for this can leave you scrambling for cash days before the closing.

Private Mortgage Insurance (PMI)

If you are putting down less than 20%—which is very common for first-time buyers using FHA or conventional loans—you will likely have to pay PMI. This protects the lender in case of default. It’s an added monthly cost that must be factored into your budget.

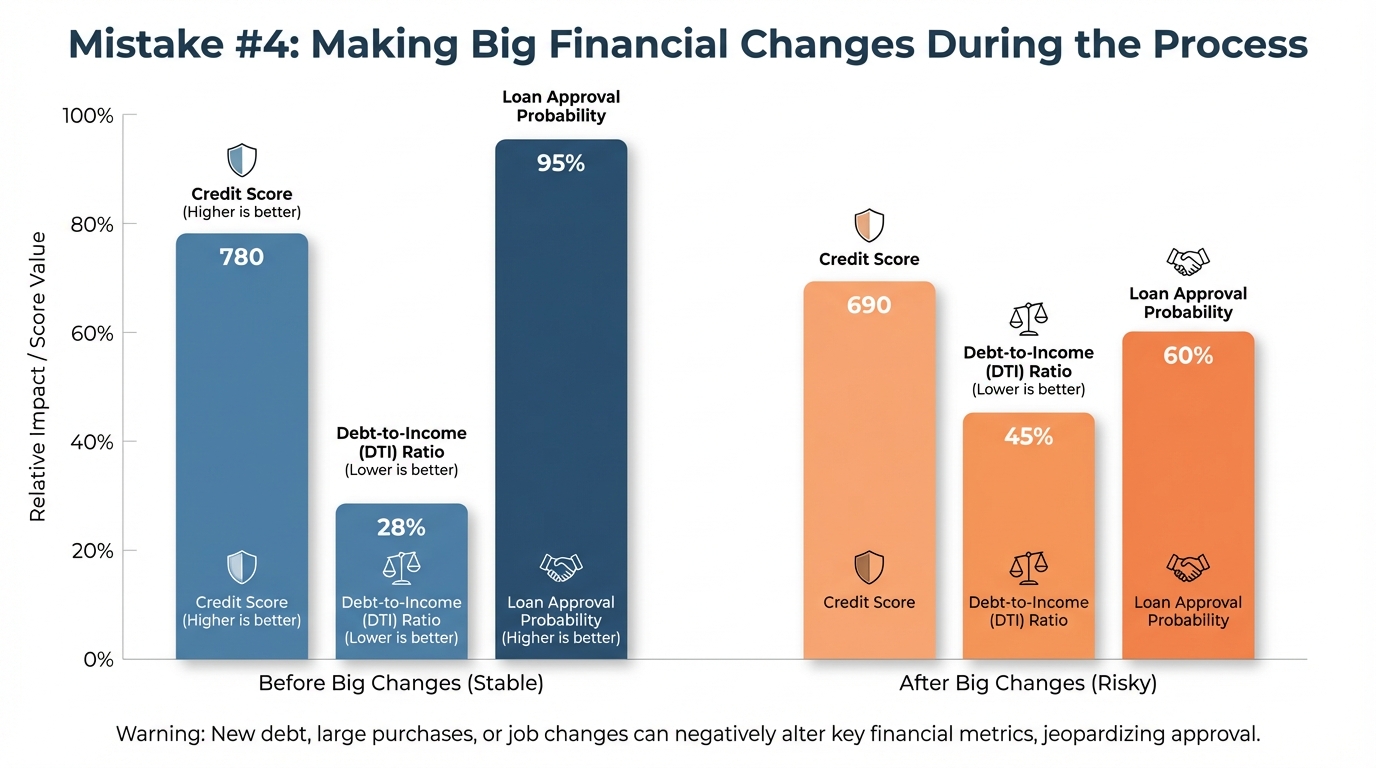

Mistake #4: Making Big Financial Changes During the Process

To ensure a smooth closing, follow these “Thou Shalt Nots” of the mortgage process:

To ensure a smooth closing, follow these “Thou Shalt Nots” of the mortgage process:

- Do NOT buy a new car: Even if you can afford the payment, the new debt changes your debt-to-income (DTI) ratio.

- Do NOT open new credit cards: Buying furniture for the new house on credit before you own the house is a major red flag.

- Do NOT quit or change jobs: Stability is key. If you must change jobs, consult your loan officer immediately.

- Do NOT move large sums of money: Large, unexplained deposits into your bank account can cause underwriting delays due to anti-money laundering regulations.

Mistake #5: Going Directly to a Big Bank Instead of a Broker

Many first-time buyers walk into the bank where they have their checking account, assuming that loyalty will get them the best deal. Unfortunately, big banks often suffer from what we call “Big-Bank Fatigue.” They have strict underwriting guidelines, slower processing times, and limited product offerings. If you don’t fit their specific “box,” you get denied.

Brokers Do It Better… RCG Does It Best.

As an independent mortgage broker in Hauppauge, RCG Mortgage works for you, not the bank. We have access to dozens of wholesale lenders, which allows us to:

- Shop the Market: We compare rates and terms from multiple lenders to find the best fit for your specific situation.

- Offer Diverse Products: Whether you need an FHA loan, a VA loan, a USDA loan, or a Non-QM loan for self-employed income, we have options big banks don’t.

- Speed and Service: We are a local business. You can call us, text us, or visit our office on Wheeler Rd. You are not just a file number to us.

Mistake #6: Draining Your Savings for the Down Payment

Homeownership comes with unexpected expenses. A water heater might break, or the roof might leak. As Andrew Russell advises, it is essential to maintain an emergency fund—often called “reserves” in the mortgage world. We can help you analyze whether it makes more sense to make a smaller down payment (keeping cash in your pocket) and pay a small amount of PMI, rather than becoming “house poor” with no liquidity.

Comparison: Local Mortgage Broker vs. Big Retail Bank

To visualize why partnering with a local expert like RCG Mortgage is beneficial for first-time buyers, consider this comparison:

| Feature | RCG Mortgage (Local Broker) | Big Retail Bank |

|---|---|---|

| Loan Options | Access to dozens of lenders and hundreds of programs (FHA, VA, USDA, Non-QM, Jumbo). | Limited to their own proprietary products only. |

| Interest Rates | Wholesale rates often lower than retail; we shop the market for you. | Set retail rates; no ability to shop around for you. |

| Speed of Process | Fast, streamlined “Ford assembly line” process. We close loans quickly. | Often slow, bureaucratic, and prone to delays. |

| Local Expertise | Deep knowledge of the Hauppauge and Long Island market, taxes, and attorneys. | Call centers often located out of state; unfamiliar with NY real estate laws. |

| Service Level | Personalized “Nordstrom” experience. You have a dedicated team. | Transactional. You are often passed between different departments. |

Actionable Advice: Your Checklist for Success

- Check Your Credit Early: Review your credit report months in advance. If your score is below 640, talk to us about strategies to improve it.

- Get a Real Pre-Approval: Contact RCG Mortgage to get a verified pre-approval letter before you view homes.

- Define Your Budget (Monthly): Don’t just ask “How much can I borrow?” Ask “How much am I comfortable paying every month?”

- Assemble Your Team: You need a great loan officer, a knowledgeable real estate agent, and a real estate attorney. We can recommend trusted local partners.

- Ask Questions: There are no stupid questions. Whether it’s about FHA Streamline Refinances for the future or understanding escrow, we are here to educate you.

Frequently Asked Questions (FAQs)

1. How much down payment do I really need for a house in Hauppauge?

Many buyers believe the myth that you need 20% down. This is false. FHA loans require as little as 3.5% down, and conventional loans for first-time buyers can be as low as 3%. If you are a veteran or active military, VA loans offer 0% down payment options. RCG Mortgage can help you determine which program fits your savings.

2. What is a “Non-QM” loan, and is it right for me?

Non-QM (Non-Qualified Mortgage) loans are designed for borrowers who don’t fit the traditional mold, such as self-employed individuals or those with complex income streams. Instead of using tax returns, we might use bank statements to qualify you. It’s an excellent option for business owners in Long Island who write off expenses but have strong cash flow.

3. Should I lock my interest rate immediately?

Interest rates change daily based on the bond market. “Rate FOMO” is real! Once you have a contract on a home, we generally recommend locking your rate to protect against market volatility. We monitor the market closely and will advise you on the optimal time to lock.

4. Can I use gift funds for my down payment?

Yes! Most loan programs allow you to use gift funds from a family member for your down payment and closing costs. However, there is a specific way to document this to satisfy anti-money laundering rules. Do not just deposit cash; speak to us first so we can provide a gift letter template and instructions.

5. Why should I choose a mortgage broker in Hauppauge over an online lender?

Real estate is local. An online lender in a different time zone won’t understand Long Island’s unique tax structure, flood zones, or the speed required to win a bid here. Furthermore, RCG Mortgage is invested in this community. Our reputation depends on your satisfaction, which is why we have been named NAMB Mortgage Broker of the Year multiple times.

Start Your Homebuying Journey the Right Way

Buying your first home should be exciting, not terrifying. By avoiding these common mistakes and partnering with a team that values transparency and accountability, you can secure a mortgage that fits your life and your budget.

At RCG Mortgage, we combine the personalized service of a local business with the power and technology of a top-tier financial institution. We are located right here at 490 Wheeler Rd, Suite 252 in Hauppauge, NY. Whether you are looking for a standard fixed-rate mortgage, an FHA loan, or just need advice on where to start, Andrew Russell and the team are ready to guide you.

Don’t navigate this market alone. Let’s get you into your dream home.

Ready to Get Pre-Approved?

Contact RCG Mortgage today for a no-obligation quote and experience the difference a dedicated broker makes.

Call us: (516) 246-6353

Email: andrew@rcgmortgage.com

Visit us: www.rcgmortgage.com