VA Loans in Hauppauge: Exclusive Programs for Military Families in Suffolk County For veterans, active-duty…

Understanding Mortgage Closing Costs for a Refinance in New York

Understanding Mortgage Closing Costs for a Refinance in New York

If you are a homeowner in New York, you know that the Empire State does things a little differently—especially when it comes to real estate and mortgages. Whether you are looking to lower your monthly payment, shorten your loan term, or tap into your home’s equity for a renovation, refinancing can be a powerful financial tool. However, the hurdle that stops many homeowners in their tracks is the concept of closing costs.

New York is notorious for having some of the highest closing costs in the country. But here is the good news: understanding what these costs are, why they exist, and how to navigate them can save you thousands of dollars. At RCG Mortgage in Hauppauge, NY, we believe that an educated borrower is an empowered borrower.

In this comprehensive guide, we will break down exactly what goes into mortgage closing costs for a refinance in New York, explain the specific taxes that hit Long Island homeowners, and reveal strategies—like the CEMA loan—that can keep money in your pocket.

The Reality of Refinancing in New York

Refinancing is essentially replacing your current mortgage with a new one. While the goal is often to save money on interest, the process involves a transaction that incurs fees. In many states, closing costs might average around 2% to 3% of the loan amount. In New York, without proper planning, they can climb significantly higher due to state-specific taxes.

However, don’t let the sticker shock scare you away from a lower interest rate. With the right mortgage broker guiding you, the long-term savings of a refinance often far outweigh the upfront costs. Plus, there are specific structures available in New York to mitigate these expenses.

Breakdown: What Am I Paying For?

When you receive your Loan Estimate, it can look like a laundry list of fees. Let’s demystify the main categories of closing costs you will encounter when refinancing a home in Hauppauge, Suffolk County, or anywhere in New York.

1. Lender and Broker Fees

These are the fees paid directly to the financial institution arranging your loan. They cover the administrative cost of processing your application.

- Origination Fee: A fee charged by the lender for processing the loan.

- Underwriting Fee: The cost for the lender to assess your creditworthiness and risk.

- Discount Points: Optional fees you pay upfront to “buy down” your interest rate.

Pro Tip: At RCG Mortgage, we pride ourselves on transparency. As a broker, we shop multiple lenders to find you the most competitive fee structures, often beating big retail banks.

2. Third-Party Fees

These are fees paid to other professionals who perform necessary services to close the loan.

- Appraisal Fee: Lenders need to know the current market value of your home to ensure they aren’t lending more than the property is worth. In Long Island’s fluctuating market, this is a crucial step.

- Credit Report Fee: The cost to pull your credit scores from the three major bureaus.

- Flood Certification: A check to see if your property is in a flood zone (common in parts of Long Island).

3. Title and Legal Fees (The NY Difference)

New York is an “attorney state,” meaning you typically need an attorney to represent you during the closing process, and the bank will have their own attorney as well.

- Bank Attorney Fee: You generally pay for the lender’s legal representation.

- Title Search and Insurance: A title company will check for liens or claims against the property. You will be required to buy a new Lender’s Title Insurance Policy for the refinance. Unlike the owner’s policy you bought when you purchased the home, this protects the lender’s investment.

4. The Big One: New York Mortgage Recording Tax

This is the fee that catches most people off guard. In New York, every time you record a new mortgage, the state and county charge a tax. In Suffolk County and much of Long Island, this tax is substantial.

For a standard refinance, you are technically paying off the old loan and recording a brand new one. This triggers the Mortgage Recording Tax on the full amount of the new loan.

However, there is a solution.

The Secret Weapon: The CEMA Loan

If you are refinancing in New York, you need to know this acronym: CEMA. It stands for Consolidation, Extension, and Modification Agreement.

How CEMA Works

Instead of discharging your old mortgage and recording a completely new one, a CEMA allows you to merge your existing mortgage with a new loan for the difference (if you are taking cash out) or simply modify the terms of the existing balance.

Why It Matters

Because you aren’t technically recording a “new” mortgage for the full amount, you only pay the Mortgage Recording Tax on the “new money” (the difference between your old balance and new loan amount). If you aren’t taking cash out, your mortgage tax could be close to zero.

While CEMA loans come with higher processing fees to the lender and attorney, the savings on the tax usually far outweigh these costs for loans over $250,000.

Cost Comparison: Standard Refinance vs. CEMA

To illustrate the potential savings, let’s look at a hypothetical scenario for a homeowner in Hauppauge, NY looking to refinance a $500,000 mortgage balance.

| Fee Type | Standard Refinance (No CEMA) | CEMA Refinance |

|---|---|---|

| Mortgage Recording Tax (Approx. 1.05% in Suffolk) | $5,250 | $0 (on unpaid principal balance) |

| CEMA Processing/Attorney Fees | $0 | ~$1,500 (Estimated) |

| Net Cost for Tax/CEMA | $5,250 | $1,500 |

| Total Savings | $0 | ~$3,750 |

*Note: These figures are estimates for educational purposes. Actual costs vary by lender, loan amount, and specific location. Always consult with RCG Mortgage for a precise quote.

Why Choose a Local Broker in Hauppauge?

You might be tempted to click a button on a massive online lender’s website, but when dealing with the complexities of New York real estate laws and CEMA agreements, local expertise is non-negotiable.

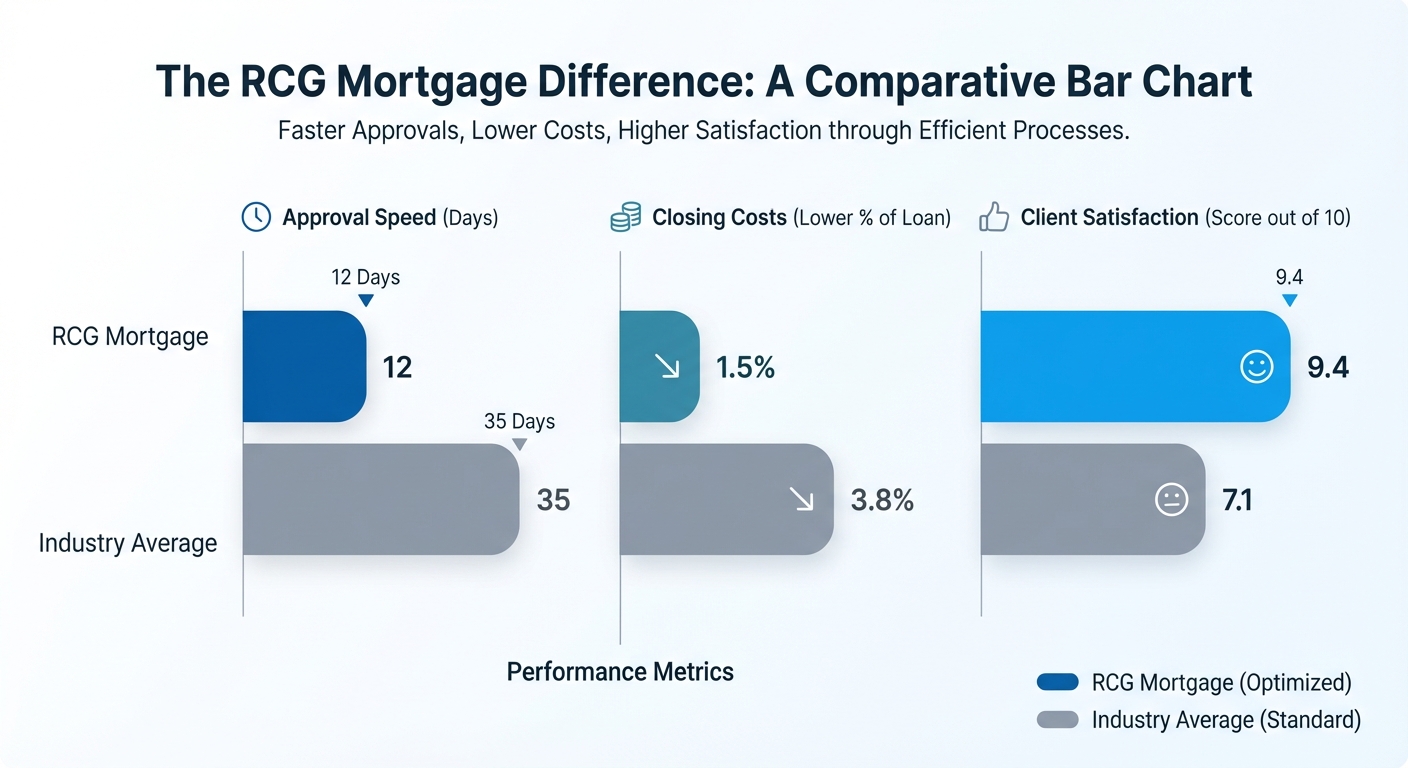

The RCG Mortgage Difference

Andrew Russell founded RCG Mortgage in 2017 with a specific vision: to combine the high-touch service of a luxury brand with the efficiency of a manufacturing line. We call it providing a “Nordstrom” experience coupled with a “Ford” assembly line.

- We Are Brokers, Not Bankers: When you walk into a bank, they can only sell you their specific products. As brokers, we work with dozens of wholesale lenders. We shop on your behalf to find the best rates and the lowest closing costs.

- Local Knowledge: We know the difference between closing in Suffolk County versus Nassau County. We have relationships with local attorneys and title companies who know how to expedite CEMA loans.

- Speed and Efficiency: We simplify the underwriting process. Our team is structured to move your loan from application to closing table efficiently, ensuring you don’t lose your rate lock.

Strategies to Reduce Closing Costs

Aside from utilizing a CEMA, there are other ways to manage the upfront costs of refinancing:

1. The “No-Closing-Cost” Refinance

2. Rolling Costs into the Loan

If you have enough equity, you can finance the closing costs. This increases your total loan amount, but it keeps cash in your bank account. This is very common for homeowners who want to maximize their liquidity.

3. Shop Around

Local Spotlight: Refinancing in Hauppauge and Long Island

Hauppauge is a unique market. With a mix of beautiful residential neighborhoods and a thriving industrial park, property values have remained robust. Refinancing here requires an appraisal team that understands the local nuances—why a home on one side of the street might appraise differently than one a block over.

Furthermore, dealing with local municipalities for permits or certificates of occupancy (CO) can sometimes delay closings. At RCG Mortgage, located right here on Wheeler Road, we help you anticipate these hurdles before they become problems.

Frequently Asked Questions (FAQs)

1. How long does it take to recoup my closing costs on a refinance?

This is called the “break-even point.” If your refinance saves you $200 a month and your closing costs were $4,000, it will take you 20 months (4,000 divided by 200) to break even. If you plan to stay in the home longer than 20 months, the refinance is a smart financial move. We can help you calculate this exact timeline.

2. Can I negotiate closing costs in New York?

Some third-party fees (like appraisal and taxes) are fixed. However, lender fees (like origination charges) are often negotiable. Because RCG Mortgage works with multiple wholesale lenders, we inherently negotiate on your behalf to find the lender with the most competitive fee structure.

3. Is a CEMA loan always the best option?

Not always. If your mortgage balance is small, the attorney fees required to process the CEMA might cost more than the tax savings. Generally, CEMA makes the most sense for loan amounts above $200,000 or $250,000. We will run the numbers both ways to see which yields the highest savings.

4. Do I need a new appraisal to refinance?

In many cases, yes. The lender needs to verify the current value of the home to determine your Loan-to-Value (LTV) ratio. However, some loan programs offer “appraisal waivers” if you have significant equity and a strong credit profile. We can check if your property is eligible for a waiver.

5. Can I refinance if I have less-than-perfect credit?

Absolutely. While the lowest advertised rates usually go to those with credit scores over 740, there are many programs (like FHA refinances or Non-QM loans) designed for borrowers with lower scores. As brokers, RCG Mortgage has access to a wider variety of loan products than traditional big banks.

Ready to Lower Your Monthly Payments?

Refinancing in New York involves moving parts, but it doesn’t have to be stressful. By understanding the costs and leveraging strategies like CEMA, you can unlock significant savings and improve your financial health.

Don’t navigate the complex world of New York mortgages alone. Work with a team that knows Hauppauge, knows Long Island, and knows how to treat you like a VIP while processing your loan with assembly-line efficiency.

Contact RCG Mortgage today for a no-obligation quote and a personalized closing cost analysis.

Call us: (516) 246-6353

Email: andrew@rcgmortgage.com

Visit us: 490 Wheeler Rd Suite 252, Hauppauge, NY 11788

Start Your Refinance Quote Now