What is a Doctor Mortgage Loan? Medical and legal professionals face unique financial challenges. From…

Comparing Conventional vs. FHA Loans for a Starter Home in Hauppauge, NY

Comparing Conventional vs. FHA Loans for a Starter Home in Hauppauge, NY

Buying your first home is one of the most significant milestones in life, especially in a competitive real estate market like Long Island. For prospective buyers eyeing a starter home in Hauppauge, NY, the journey often begins not at an open house, but with a look at finances. Two of the most common pathways to homeownership are Conventional loans and FHA loans. But how do you know which one is right for you?

As a leading Mortgage Broker based right here in Hauppauge, RCG Mortgage understands the unique nuances of the Suffolk County market. While both loan types can get you the keys to your new home, they are designed for different borrower profiles. Let’s break down the differences to help you make an informed decision.

The Conventional Loan: The Standard for Strong Credit

A Conventional loan is a mortgage that is not insured or guaranteed by the federal government. Instead, these loans are backed by private lenders and usually sold to government-sponsored enterprises like Fannie Mae or Freddie Mac. For many years, this has been the “gold standard” for borrowers with established credit histories.

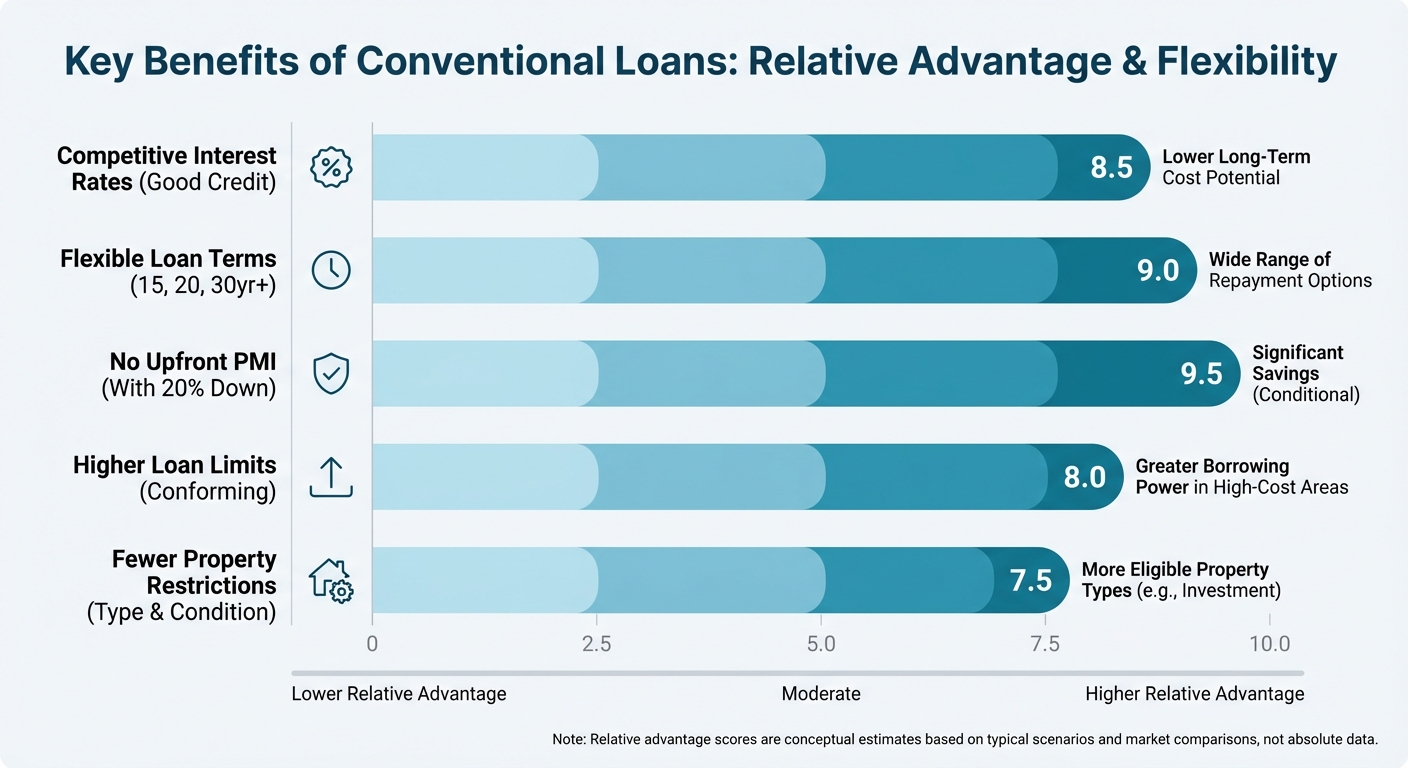

Key Benefits of Conventional Loans

- PMI Removal: If you put down less than 20%, you will have to pay Private Mortgage Insurance (PMI). However, unlike FHA loans, this PMI falls off automatically once you reach 22% equity in your home.

- Flexible Down Payments: Contrary to the popular “20% down” myth, first-time homebuyers can often qualify for a Conventional loan with as little as 3% down.

- Property Flexibility: These loans can be used for primary residences, second homes, or investment properties.

The FHA Loan: The Flexible Path to Homeownership

An FHA loan is a government-backed mortgage insured by the Federal Housing Administration. These loans were created to make homeownership more accessible, particularly for first-time buyers who might not have a perfect credit score or a massive down payment saved up.

Key Benefits of FHA Loans

- Lower Credit Score Requirements: You can generally qualify for an FHA loan with a credit score as low as 580.

- Forgiving Debt Ratios: FHA loans often allow for a higher Debt-to-Income (DTI) ratio, which is helpful for buyers carrying student loans or auto loans.

- Low Down Payment: The minimum down payment is fixed at 3.5%, making the barrier to entry lower for many Hauppauge residents.

Head-to-Head Comparison: Conventional vs. FHA

To help you visualize the differences, here is a comparison based on typical standards for a starter home in the Hauppauge area.

| Feature | Conventional Loan | FHA Loan |

|---|---|---|

| Minimum Down Payment | 3% (for first-time buyers) | 3.5% |

| Minimum Credit Score | Typically 620+ | Typically 580+ |

| Mortgage Insurance | PMI (Can be removed at 20% equity) | MIP (Usually for the life of the loan) |

| Debt-to-Income Ratio | Stricter (usually up to 45-50%) | More Flexible (can go higher) |

| Appraisal Standards | Standard safety/value check | Strict safety/habitability check |

Why Choose a Local Mortgage Broker in Hauppauge?

When shopping for a home in Long Island, many buyers instinctively walk into a big bank. However, this can lead to “Big-Bank Fatigue”—endless paperwork, impersonal service, and limited options. This is where partnering with a local Mortgage Broker like RCG Mortgage changes the game.

A mortgage lender at a bank can only offer you their specific products. If their rates are high or their guidelines are strict, you are out of luck. As brokers, we work differently:

- We Shop for You: We have access to multiple wholesale lenders. We compare rates and terms from various sources to find the loan that fits your life, not the bank’s quota.

- Local Expertise: We know the Hauppauge market. We understand local property taxes and how they impact your monthly payment and purchasing power.

- Speed and Efficiency: We pride ourselves on a “Nordstrom” experience with “Ford” assembly line efficiency. We simplify the underwriting process to get you to the closing table faster.

Which Loan is Right for You?

There is no single “best” loan—only the loan that is best for your financial situation. If you have excellent credit and want to avoid long-term mortgage insurance, Conventional might be the winner. If you are rebuilding credit or need flexibility on your debt ratios, FHA is a powerful tool to get you into a home sooner.

At RCG Mortgage, we believe transparency and education are key. We don’t just quote a rate; we explain your options so you can move forward with confidence.

Ready to Explore Your Options?

Don’t navigate the complex world of mortgages alone. Whether you are looking for a Conventional, FHA, or even a VA loan, our team is here to guide you every step of the way.

Request a Quote Today or call us at (516) 246-6353 to speak with a local expert about your homeownership goals.

Related Posts