VA Loans in Hauppauge: Exclusive Programs for Military Families in Suffolk County For veterans, active-duty…

Debunking 5 Common Mortgage Myths That Could Cost You Thousands

Debunking 5 Common Mortgage Myths That Could Cost You Thousands

Buying a home is arguably the most significant financial decision you will make in your lifetime. However, the path to homeownership is often cluttered with misinformation, outdated advice, and “rules of thumb” that simply don’t apply in today’s market. Whether you are looking to purchase your first home in Hauppauge, NY, or you are a seasoned investor looking to refinance on Long Island, falling for these common mortgage myths can prevent you from getting the best deal—or worse, keep you out of a home entirely.

At RCG Mortgage, we believe that an educated borrower is our best client. Led by Andrew Russell, a multi-year NAMB Mortgage Broker of the Year, our team is dedicated to providing transparency and clarity. We combine a “Nordstrom” level of customer service with a “Ford” assembly line efficiency to ensure your loan closes on time and on budget.

In this comprehensive guide, we are going to dismantle the top five mortgage myths that could be costing you thousands of dollars, and show you how a local mortgage broker in Hauppauge can help you navigate the real estate market with confidence.

Myth #1: You Need a 20% Down Payment to Buy a Home

The Reality: Most homebuyers put down significantly less than 20%, and there are many loan programs designed specifically for low down payments.

This is perhaps the most pervasive myth in the real estate industry. While putting 20% down was the standard decades ago—and it does help you avoid Private Mortgage Insurance (PMI)—it is absolutely not a requirement to purchase a home today. Believing this myth keeps many qualified renters on the sidelines, paying someone else’s mortgage while they struggle to save a massive lump sum.

Modern lending offers flexible options for borrowers in Hauppauge and across New York:

- FHA Loans: Backed by the Federal Housing Administration, these loans allow for down payments as low as 3.5%. This is a popular option for first-time homebuyers.

- VA Loans: For eligible veterans, active-duty service members, and surviving spouses, VA loans often require 0% down payment and do not require monthly mortgage insurance.

- USDA Loans: For properties in designated rural or suburban areas, USDA loans also offer 0% down financing.

- Conventional 97: Qualified borrowers can obtain a conventional loan with as little as 3% down.

Expert Tip: Don’t deplete your emergency savings just to reach a 20% down payment. It is often financially safer to put less down and keep cash reserves for home repairs, moving costs, and life’s unexpected events.

Myth #2: You Need “Perfect” Credit to Qualify

The Reality: You can qualify for a mortgage with a credit score well below 700.

Many potential buyers assume that if their credit score isn’t 780 or 800, they will be rejected by lenders. This is simply untrue. While a higher credit score can unlock lower interest rates, there are plenty of loan products available for borrowers with average or even “fair” credit.

At RCG Mortgage, we work with a wide variety of lenders, giving us access to products that big-box banks simply don’t offer. For example:

- FHA Loans: Generally allow for credit scores down to 580 (with 3.5% down) or even lower with a larger down payment.

- Non-QM Loans: “Non-Qualified Mortgage” loans are designed for borrowers with unique financial situations, such as self-employed individuals or those with credit events in their past.

If your credit score is below 640, don’t rule yourself out. Contact us to review your report. Sometimes, small adjustments—like paying down a specific credit card balance—can boost your score enough to qualify for a better tier of financing.

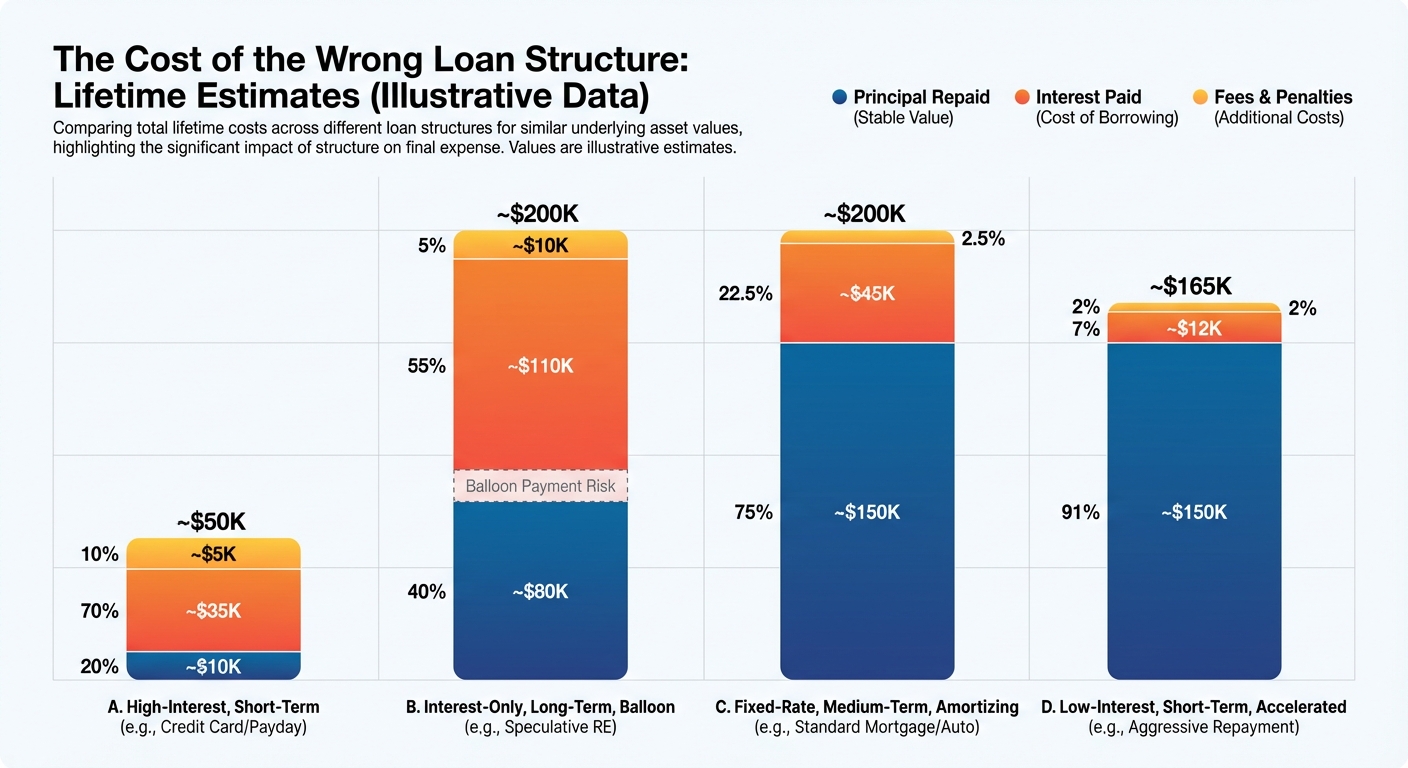

Myth #3: The Lowest Interest Rate is the Only Thing That Matters

The Reality: The Annual Percentage Rate (APR) and closing costs are just as important as the interest rate. A low rate with high fees is not a bargain.

It is easy to get fixated on the headline interest rate. However, some lenders (especially big online advertisers) may quote a rock-bottom rate but hide thousands of dollars in “discount points” or origination fees in the fine print. This is why you must look at the APR (Annual Percentage Rate), which represents the true cost of the loan including fees.

The Cost of the Wrong Loan Structure

Imagine Lender A offers you a 6.5% rate with $0 in points. Lender B offers you a 6.0% rate but charges you $8,000 upfront to “buy down” the rate. If you plan to move or refinance in 3 years, Lender B’s option might actually cost you more money overall, despite the lower monthly payment.

At RCG Mortgage, we focus on the Total Cost Analysis. We help you compare loan estimates side-by-side so you understand exactly what you are paying upfront versus what you are paying monthly. We tailor the loan structure to your long-term goals, whether that’s staying in your Hauppauge home forever or moving in five years.

At RCG Mortgage, we focus on the Total Cost Analysis. We help you compare loan estimates side-by-side so you understand exactly what you are paying upfront versus what you are paying monthly. We tailor the loan structure to your long-term goals, whether that’s staying in your Hauppauge home forever or moving in five years.

Myth #4: Pre-Qualification is the Same as Pre-Approval

The Reality: In the competitive Long Island housing market, a pre-qualification letter carries very little weight. You need a solid Pre-Approval.

Many buyers think they are ready to make an offer because they filled out a quick form online and received a “Pre-Qualification” letter. Here is the critical difference:

- Pre-Qualification: This is an estimate based on unverified information you provided verbally or online. The lender hasn’t pulled your credit or verified your income documents. It’s a “best guess.”

- Pre-Approval: This involves a thorough review of your financial life. The lender has pulled your credit, reviewed your W-2s, tax returns, and bank statements. A Pre-Approval letter tells the seller that you are a serious buyer and that financing is highly likely to be secured.

In areas like Hauppauge, Smithtown, and Commack, sellers often receive multiple offers. If you submit an offer with a flimsy pre-qualification, you will likely lose out to a buyer with a verified pre-approval from a reputable local broker like RCG Mortgage.

Myth #5: It’s Cheaper to Go Directly to a Big Bank

The Reality: Mortgage brokers often secure lower rates and lower fees than big retail banks because they have access to wholesale pricing.

There is a misconception that by “cutting out the middleman” and going to a big retail bank, you save money. The opposite is often true. Retail banks have massive overhead costs (branches, tellers, national advertising) and they only sell their own proprietary products. If their rate is high today, that is the only rate they can offer you.

Brokers Do It Better… RCG Does It Best.

As an independent mortgage broker, RCG Mortgage acts as a personal shopper for your loan. We are not tied to one lender. We shop dozens of wholesale lenders to find the specific product that fits your profile at the most competitive price. Because we bring lenders fully packaged, “ready-to-fund” loans, they offer us wholesale interest rates that are typically lower than what they offer to the general public.

Comparison: Mortgage Broker vs. Retail Bank

| Feature | RCG Mortgage (Broker) | Big Retail Bank |

|---|---|---|

| Loan Options | Access to dozens of lenders and hundreds of programs (FHA, VA, Non-QM, Jumbo). | Limited to the bank’s own specific products. |

| Interest Rates | Wholesale rates; we shop the market for you. | Retail rates; take it or leave it. |

| Speed & Efficiency | “Ford Assembly Line” process; faster closings. | Often bogged down by corporate bureaucracy; slower turn times. |

| Expertise | Specialized in mortgages only. Licensed experts. | Generalists who may also handle checking accounts and auto loans. |

| Local Knowledge | Deep understanding of Long Island/NY taxes and laws. | Call centers often located out of state or overseas. |

Why Local Expertise Matters in Hauppauge, NY

We are proud to be recognized as the NAMB Mortgage Broker of the Year for four consecutive years (2022-2025) and listed as the #1 Loan Originator in Long Island by Scotsman Guide. When you work with us, you are getting national recognition with a local handshake.

Frequently Asked Questions (FAQs)

1. Can I buy a home in Hauppauge if I have student loan debt?

Yes! Student loan debt does not automatically disqualify you from getting a mortgage. Lenders look at your Debt-to-Income (DTI) ratio. As long as your total monthly debt payments (including the new mortgage) are within the lender’s guidelines relative to your income, you can qualify. There are also specific calculations for student loans that a skilled broker can help you navigate.

2. Is it better to find a home first or get a mortgage pre-approval first?

Always get pre-approved first. A pre-approval defines your budget so you don’t fall in love with a house you can’t afford. Furthermore, most real estate agents in New York will not show you homes until you have a pre-approval letter, and sellers will certainly not accept an offer without one.

3. How much are closing costs in New York?

Closing costs in New York typically range between 3% and 6% of the loan amount. This includes taxes, title insurance, attorney fees, and lender fees. New York is known for having higher closing costs due to mortgage recording taxes, so it is vital to get a detailed Loan Estimate from RCG Mortgage early in the process so there are no surprises.

4. What if I am self-employed? Is it harder to get a mortgage?

It can be more complex, but not necessarily harder if you work with the right broker. Traditional banks often struggle to underwrite self-employed borrowers because tax write-offs can make income look lower than it is. RCG Mortgage offers “Bank Statement Loans” and other Non-QM products that allow us to use your business cash flow to qualify you, rather than just your tax returns.

5. Should I wait for interest rates to drop before buying?

Trying to time the market is risky. If you wait for rates to drop, home prices often rise due to increased demand, negating your savings. The saying goes: “Marry the house, date the rate.” You can always refinance your mortgage later if rates drop significantly, but you cannot go back and buy a home at today’s prices once values appreciate.

Ready to Navigate Your Mortgage Journey?

Don’t let myths and misconceptions cost you your dream home or thousands of dollars in unnecessary interest. Whether you are a first-time homebuyer, looking to move up, or interested in refinancing, RCG Mortgage is here to guide you with honesty, speed, and expertise.

Experience the difference of working with the #1 Mortgage Broker in Long Island. Let us provide you with a no-obligation quote and a customized plan to achieve your homeownership goals.

Contact RCG Mortgage Today

Phone: (516) 246-6353

Email: andrew@rcgmortgage.com

Address: 490 Wheeler Rd Suite 252, Hauppauge, NY 11788