What is a Doctor Mortgage Loan? Medical and legal professionals face unique financial challenges. From…

Understanding the True Cost of Homeownership in Suffolk County Beyond the Mortgage

Understanding the True Cost of Homeownership in Suffolk County Beyond the Mortgage

Buying a home is widely considered the ultimate American Dream. For many aspiring homeowners in Hauppauge, NY, and throughout Suffolk County, that dream involves a spacious yard, a safe neighborhood, and a place to build long-lasting memories. However, the path to homeownership involves more than just scraping together a down payment and locking in an interest rate.

At RCG Mortgage, we believe in radical transparency. As Andrew Russell, our founder and a multi-year NAMB Mortgage Broker of the Year, often says, we aim to provide a “Nordstrom” experience coupled with a “Ford” assembly line efficiency. Part of that premium service is ensuring our clients are fully educated on the financial realities of owning a home on Long Island.

While the monthly mortgage payment is the headline number, the “hidden” costs—property taxes, insurance, maintenance, and utilities—can significantly impact your monthly budget. In this comprehensive guide, we will break down the true cost of homeownership in Suffolk County so you can navigate the process with confidence and financial security.

The “Sticker Price” vs. The Real Monthly Payment

When you look at a listing on Zillow or Redfin for a beautiful colonial in Hauppauge or Smithtown, the estimated monthly payment usually calculates the Principal and Interest (P&I). While this is the bulk of your loan repayment, it is rarely the full amount you will write a check for every month.

In the mortgage industry, we use the acronym PITI to describe the total monthly obligation:

- Principal: The money that goes toward paying down the loan balance.

- Interest: The cost of borrowing the money.

- Taxes: Property taxes collected by your local municipality.

- Insurance: Homeowners insurance to protect the asset.

In Suffolk County, the “T” and “I” portions of that equation are substantial and can sometimes equal or exceed the principal portion of your payment. Ignoring these variables is the quickest way to find yourself “house poor.”

1. The Reality of Property Taxes on Long Island

It is no secret that Long Island has some of the highest property taxes in the nation. When budgeting for a home in Suffolk County, you must look closely at the specific tax bill for the property, not just a county average.

Why Are Taxes So High?

Your property taxes fund local school districts, police departments, fire departments, libraries, and general municipal services. In areas like Hauppauge, the school districts are top-tier, which is a major draw for families but comes with a higher tax levy.

The Variation by Hamlet and Village

Taxes can vary wildly depending on exactly where the home is located. A home in the Town of Islip might have a different tax rate than a similar home in the Town of Smithtown, even if they are only a few miles apart. Furthermore, if you buy within an incorporated village (like the Village of Islandia or Nissequogue), you may pay an additional village tax on top of your town and school taxes.

The STAR Exemption

When calculating costs, it is important to factor in the New York State School Tax Relief (STAR) program. Eligible homeowners can receive a reduction on their school tax bill. While this offers relief, you should budget based on the gross tax amount first to ensure you can comfortably afford the home before any potential rebates arrive.

2. Homeowners Insurance and Flood Zones

Protecting your investment is non-negotiable. Homeowners insurance prices in New York have been rising due to increased material costs and weather-related risks.

Coastal Considerations

Suffolk County is surrounded by water. Even if you aren’t buying a beachfront property in the Hamptons, windstorm deductibles and hurricane risks influence insurance premiums across the island. If you are purchasing a home south of Montauk Highway or near the Sound, lenders may require Flood Insurance, which is a separate policy from your standard homeowners insurance.

Standard homeowners insurance covers fire, theft, and liability. It generally costs between $1,200 and $2,500 annually for an average home in Suffolk, but this can double if specialized flood coverage is required. At RCG Mortgage, we recommend shopping local for insurance just like you do for your mortgage—local agents understand Long Island’s specific zoning maps better than national call centers.

3. Closing Costs: The Upfront Hurdle

Many first-time homebuyers in Hauppauge focus entirely on the down payment (e.g., 3.5% for an FHA loan or 20% for a conventional loan) and forget about closing costs. In New York, closing costs are among the highest in the country.

The New York Mortgage Recording Tax

The biggest surprise for many buyers is the Mortgage Recording Tax. In Suffolk County, this is generally 1.05% of the loan amount. For a $500,000 mortgage, that is an upfront cost of $5,250 just to record the loan with the county clerk. (Note: Lenders often pay a small portion of this, typically 0.25%, but the borrower bears the brunt).

Other Essential Closing Fees

- Title Insurance: Protects you and the lender against claims regarding the legal ownership of the home.

- Attorney Fees: New York is an “attorney state,” meaning both the buyer and seller must have legal representation.

- Pre-paid Items: You will likely have to pay a year of homeowners insurance upfront, plus roughly 3 to 6 months of property taxes to set up your escrow account.

When you request a quote from RCG Mortgage, we provide a detailed Loan Estimate that clearly outlines these cash-to-close requirements so there are no surprises at the closing table.

4. Utilities and Maintenance: The 1% Rule

Once you have the keys, the meter starts running. Moving from an apartment where heat might have been included to a 2,500-square-foot colonial means taking on full responsibility for utilities.

Energy Costs in Suffolk County

Long Island electricity rates (serviced by PSEG Long Island) are higher than the national average. Additionally, many older homes in Suffolk County still rely on oil heat. Filling an oil tank during a cold winter can cost several thousand dollars per season. Homes with natural gas (National Grid) tend to be more efficient, but converting from oil to gas is a significant capital expense.

The 1% Maintenance Rule

A smart rule of thumb for budgeting is to set aside 1% of your home’s purchase price annually for maintenance. If you buy a home for $600,000, you should budget $6,000 a year ($500/month) for repairs and upkeep.

Common Suffolk County maintenance costs include:

- Landscaping: Grass grows fast in the spring. Weekly cuts can range from $40 to $100.

- Snow Removal: While many shovel their own driveways, heavy Nor’easters may require professional plowing.

- Cesspool/Septic Service: Many areas in Suffolk are not on public sewers. Septic tanks need pumping and maintenance every few years.

- System Repairs: Boilers, hot water heaters, and roofs eventually need replacement.

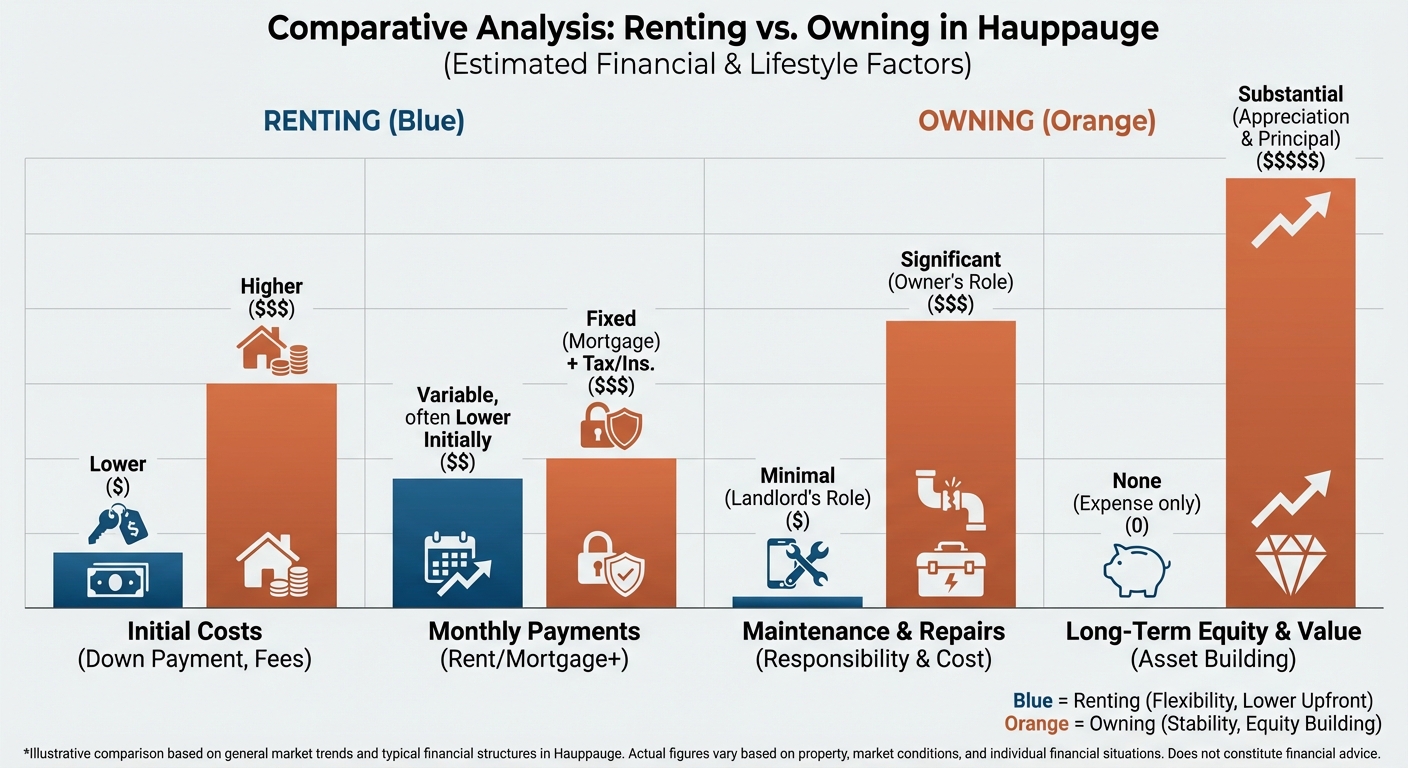

Comparative Analysis: Renting vs. Owning in Hauppauge

| Expense Category | Homeowner (Est. Monthly) | Renter (Est. Monthly) |

|---|---|---|

| Mortgage / Rent | $3,600 (P&I @ approx rates) | $4,200 |

| Property Taxes | $1,000 | $0 (Included in rent) |

| Homeowners Insurance | $150 | $25 (Renters Insurance) |

| Maintenance/Repairs | $500 (Budgeted) | $0 (Landlord responsibility) |

| Utilities (Water/Heat/Electric) | $400 | $200 (Often partially included) |

| Total Monthly Outflow | $5,650 | $4,425 |

| Wealth Creation (Equity) | High (Amortization + Appreciation) | None |

*Note: The figures above are estimates for educational purposes only. Interest rates and tax assessments vary.

While owning appears more expensive monthly, the Wealth Creation row is the differentiator. A renter pays $4,425 with 0% return on investment. A homeowner pays more, but a portion of that payment pays down their own debt (forced savings), and the asset typically appreciates over time.

Why Working with a Local Mortgage Broker Matters

Navigating these costs requires a partner who understands the local landscape. This is where RCG Mortgage distinguishes itself from big-box banks or online lenders.

Local Expertise vs. Call Centers

When you call a 1-800 number, the operator likely doesn’t know the difference between a tax bill in Islip vs. Brookhaven, or why you might need a specific wind deductible in Babylon. We do. Based right here in Hauppauge, NY, we live and work in the communities we serve.

Tailored Solutions for Your Budget

We don’t just hand you a pre-approval letter for the maximum amount you can borrow; we discuss what you should borrow based on your total budget, including those hidden costs mentioned above. Whether it’s an FHA loan with a lower down payment to save cash for renovations, or a conventional loan to eliminate mortgage insurance, we tailor the product to your life goals.

The “Broker Advantage”

Actionable Tips for Prospective Buyers

- Get a Full PITI Quote: When getting pre-qualified, ask us to estimate the full monthly payment including taxes and insurance, not just the loan payment.

- Check the Tax History: Don’t just look at the current year’s taxes. Check if the current owner has exemptions (like veterans or seniors) that you might not qualify for, which would cause the taxes to jump up after closing.

- Inspect the Utilities: During your home inspection, ask about the age of the boiler and the roof. These are big-ticket items that impact your “hidden cost” budget.

- Start an Emergency Fund: Before closing, ensure you have reserves left over. Do not drain every penny you have for the down payment. You need a cushion for that first unexpected repair.

Frequently Asked Questions (FAQs)

1. How much are closing costs typically in Suffolk County?

Closing costs in Suffolk County typically range between 3% and 5% of the purchase price. This includes the New York State Mortgage Recording Tax, attorney fees, title insurance, and pre-paid escrow items for taxes and insurance.

2. What is the difference between a Mortgage Broker and a Bank?

A bank can only offer you their specific loan products and rates. A mortgage broker, like RCG Mortgage, acts as an intermediary who can shop your application across dozens of wholesale lenders to find the best rate, term, and product for your specific situation. We work for you, not the bank.

3. Do I really need a 20% down payment to avoid hidden costs?

No. While 20% down eliminates Private Mortgage Insurance (PMI), many buyers in Suffolk County successfully purchase homes with 3% or 3.5% down using Conventional or FHA loans. We can help you calculate if the cost of PMI is worth the benefit of keeping more cash in your pocket for home repairs.

4. How do I know if the property taxes on a listing are accurate?

Listing sites often estimate taxes or show data that may be outdated. It is crucial to verify the taxes with the local town tax receiver or ask your real estate agent for the true tax bill. Remember to ask if the current figure includes STAR exemptions, which you will have to re-apply for.

5. Can I roll my closing costs into the mortgage?

Generally, for a home purchase, you cannot roll closing costs into the loan amount (with some exceptions like USDA loans or specific seller concessions). However, for a refinance, closing costs can often be included in the new loan balance.

Ready to Understand Your True Buying Power?

Buying a home in Suffolk County is a significant financial commitment, but it is also one of the most rewarding investments you can make. Don’t let the “hidden” costs surprise you. Partner with a team that prioritizes transparency and education.

At RCG Mortgage, our talented team is here to guide you through every step of the process, from pre-approval to the closing table. We have been recognized as the #1 Brokerage on Long Island because we put our clients’ financial health first.

Ready for a no-obligation quote? Let’s run the numbers together.

Get Started with RCG Mortgage Today

Or call us directly at (516) 246-6353

Related Posts