Understanding the Basics of a Conventional Mortgage When you are ready to buy a home…

The Complete Guide to Adjustable-Rate Mortgages (ARMs) in Hauppauge, NY

Understanding the Basics of an Adjustable-Rate Mortgage

When exploring home financing options in Hauppauge, NY, understanding the nuances of an adjustable rate mortgage is crucial. Also known as an ARM, this type of loan offers an initial interest rate that is typically lower than what you would find with a 30-year fixed-rate mortgage or a 15-year fixed-rate mortgage. After this introductory fixed period, the interest rate will adjust periodically based on market indexes.

For many Long Island homebuyers, an adjustable rate mortgage provides significant upfront savings. Whether you are considering a 3/1 ARM for a short-term stay or a 10/1 ARM for a longer horizon, RCG Mortgage is here to help you navigate your choices. Our team understands that every borrower has unique needs, and we pride ourselves on delivering tailored mortgage solutions.

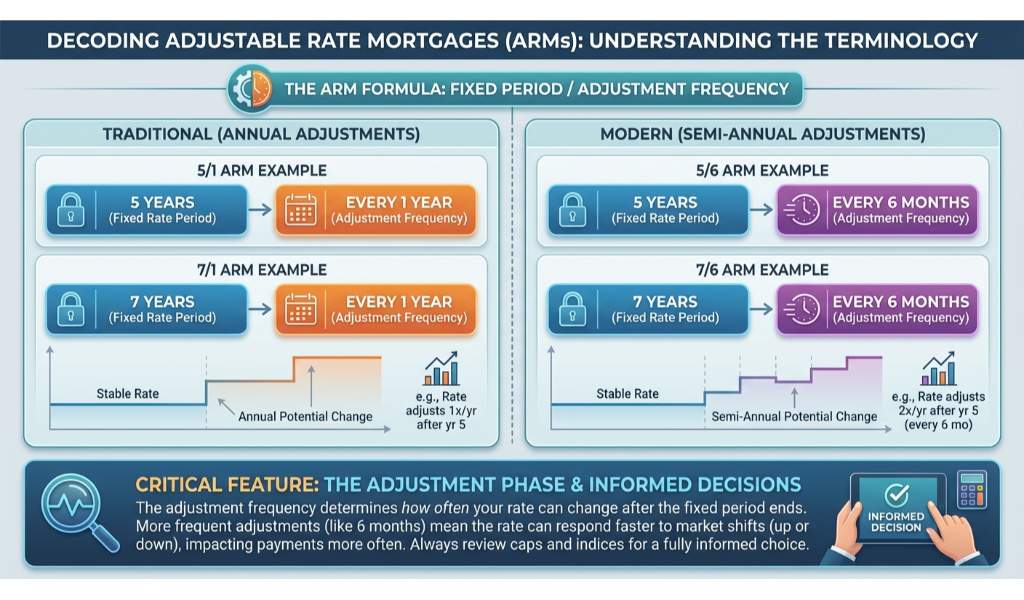

Breaking Down ARM Structures: 5/1, 7/1, 5/6, and 7/6 ARMs

To make an informed decision, it is essential to understand the terminology behind these loans. The numbers in an ARM (such as a 5/1 ARM or 7/1 ARM) represent the fixed period and the adjustment frequency. For example, in a 5/1 ARM, the rate remains fixed for five years and then adjusts once every year. Recently, lenders have also introduced options like the 5/6 ARM and 7/6 ARM, where the rate adjusts every six months after the initial fixed period.

One of the most critical features of an adjustable rate mortgage is its system of caps and floors. These protections limit how much your interest rate can change:

- Initial Cap: Limits the rate increase at the first adjustment.

- Periodic Cap: Limits how much the rate can increase during subsequent adjustment periods.

- Lifetime Cap: The absolute maximum interest rate you can be charged over the life of the loan.

- Floor: The minimum interest rate your loan can drop to.

These safeguards are especially important if you are financing a luxury property with a jumbo mortgage, where even small rate changes can significantly impact your monthly payment.

| ARM Type | Fixed Period | Adjustment Frequency |

|---|---|---|

| 3/1 ARM | 3 Years | Annually |

| 5/1 ARM | 5 Years | Annually |

| 5/6 ARM | 5 Years | Every 6 Months |

| 7/1 ARM | 7 Years | Annually |

| 7/6 ARM | 7 Years | Every 6 Months |

| 10/1 ARM | 10 Years | Annually |

Why Choose an ARM and How to Get a Second Opinion

Choosing an adjustable rate mortgage can be a strategic financial move if you plan to sell your home or refinance before the adjustable period begins. If market conditions change favorably, you might even consider a rate-and-term refinance to lock in a stable fixed rate down the road.

At RCG Mortgage, led by Andrew Russell, we are experts at providing second opinions on adjustable-rate mortgages. If you have received a quote from another lender and want to ensure you are getting the best possible terms for your Hauppauge home, our award-winning team is ready to review your options. As a multi-year NAMB Mortgage Broker of the Year, we operate with integrity and excellence to secure your financial future.

Q1: What is an adjustable rate mortgage?

An adjustable rate mortgage (ARM) is a home loan with an interest rate that changes periodically after an initial fixed-rate period.

Q2: How do caps and floors work on an ARM?

Caps limit how much your interest rate can increase initially, periodically, and over the life of the loan. Floors set a minimum limit on how low the rate can drop.

Q3: Is a 5/1 ARM better than a fixed-rate mortgage?

A 5/1 ARM can be advantageous if you plan to move or refinance within five years, as it typically offers a lower initial interest rate than a traditional fixed mortgage.

Q4: What is the difference between a 5/1 ARM and a 5/6 ARM?

Both options offer a five-year fixed rate. However, a 5/1 ARM adjusts annually after the fixed period, while a 5/6 ARM adjusts every six months.

Q5: Can I refinance my ARM before the rate adjusts?

Yes, many homeowners choose to use a rate-and-term refinance to switch to a stable fixed-rate loan before their ARM enters the adjustable phase.

Ready to explore your mortgage options or need a second opinion on an adjustable-rate mortgage?

Visit RCG Mortgage or call Andrew Russell directly at (516) 246-6353 to get started today.

Related Posts